Highlights

- ANTO's revenue for FY23 increased by 7.9% to USD 6,324.5 million compared to USD 5,862.0 million in FY22

- Gold production in FY23 also saw a significant rise of 18% to 209,100 ounces, attributed to higher gold grades at Centinela

- Total copper sales volumes rose by 3.8%, while gold sales witnessed a notable uptick of 17.3% in FY23

Antofagasta PLC (LSE: ANTO) is an FTSE 100 index listed company. It specializes in copper mining and operates four copper mines in Chile. Besides, the company has a transport division as well in Northern Chile, to serve mining customers. It has a market capitalization of GBP 21,836.73 million.

ANTO's revenue for FY23 increased by 7.9% to USD 6,324.5 million compared to USD 5,862.0 million in the previous corresponding period (pcp). The surge in revenue was driven by both a rise in the quantity of metals produced and an uptick in realized sales prices. Additionally, EBITDA saw a 5.4% surge to USD 3,087.2 million, up from USD 2,929.7 million in FY22.

The group also noted a slight uptick in copper production by 2%, reaching 660,600 tonnes primarily due to increased output from Los Pelambres. Gold production for FY23 saw a significant rise of 18% to 209,100 ounces, attributed to higher gold grades at Centinela. Moreover, total copper sales volumes rose by 3.8%, while gold sales witnessed a notable uptick of 17.3% in FY23.

Further, the company had a higher EBITDA margin of 32.5% and a higher current ratio of 2.37x in FY23, surpassing the industry median of 13.4% and 1.83x, respectively.

Recent business update

According to the company's Q1 FY24 production update, copper production totalled 129,400 tonnes, marking an 11% decline from Q1 FY23. This decrease can be primarily attributed to lower grades and increased ore hardness at Centinela. Gold production also experienced a downturn, falling by 21% to 33,300 tonnes, attributed to anticipated lower grades at Centinela in Q1 FY24. On the other hand, molybdenum production saw an 8% increase, reaching 2,700 tonnes, propelled by higher output at Los Pelambres in Q1 FY24.

Company outlook

ANTO anticipates copper production to range between 670,000 tonnes and 710,000 tonnes in FY24, with quarterly production progressively rising throughout the year. The company maintains its cash cost guidance at USD 2.25 per pound before by-product credits and USD 1.60 per pound after credits.

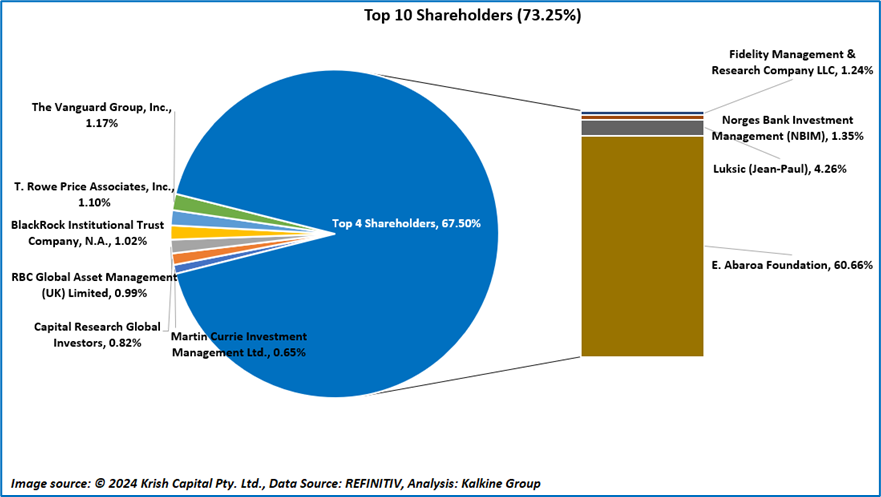

Top 10 Shareholders

The top 10 shareholders of ANTO together account for approximately 73.25% of the total shareholdings in the company. E. Abaroa Foundation holds the largest shareholding at approximately 60.66%, followed by Luksic (Jean-Paul) at around 4.26%, as shown in the chart below:

Stock performance

The share price of ANTO has increased by about 20.11% in the last three months and over the last six months, it has surged by around 50.61%. The stock has a 52-week high and 52-week low of GBX 2,425.00 & 1,280.00, respectively. At present, it is trading above the average of its 52-week high-low.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference data for all price data, currency, technical indicators, support, and resistance levels is 04 June 2024. The reference data in this report has been partly sourced from EODHD/Others.