Highlights

- FY25 network sales of GYG reached AUD 1.18 billion, up 23% YoY, with EBITDA up 138.8% YoY and NPAT of AUD 14.5 million.

- GYG announced a maiden dividend of 12.6 cents per share following a turnaround from prior-year losses.

- FY26 plans include opening 32 new restaurants, with 72% in drive-thru format, while targeting 40 new Australian outlets annually over the next five years.

Guzman y Gomez Limited (ASX:GYG), the Australian quick-service restaurant (QSR) chain specialising in fresh, made-to-order Mexican-inspired meals, had announced encouraging financial results for the year ended 30 June 2025 (FY25). Since its inception in Sydney in 2006, the company has grown to more than 250 locations across Australia, Singapore, Japan, and the United States.

FY25 Results

For FY25, GYG recorded network sales of AUD 1.18 billion, representing a 23% YoY increase from AUD 959.7 million in FY24. Earnings before interest, taxes, depreciation, and amortization (EBITDA) surged to AUD 65.1 million in FY25, marking a 138.8% rise compared to AUD 27.3 million in the previous year. The company also achieved a net profit after tax (NPAT) of AUD 14.5 million, reversing a loss of AUD 13.7 million in FY24.

The sales performance was attributed to sustained comparable sales growth and network expansion. The Australia segment, including operations in Singapore and Japan, posted 9.6% comparable sales growth. The company declared a maiden dividend of 12.6 cents per share.

Business Updates

On 28 August 2025, GYG announced that Director Thomas Cowan reduced his indirect holding in the company by 2.6 million shares following clients assuming direct management. He continues to hold more than 21 million shares through TDM entities.

Outlook

In FY26, GYG plans to open 32 new restaurants, of which 20 will be franchised and 12 corporate-owned, with about 72% adopting the drive-thru format. EBITDA margins are projected to rise to 5.9%–6.3%, supported by comparable sales momentum and strategic initiatives.

Looking ahead, the company aims to expand aggressively in Australia, targeting 40 new restaurants annually over the next five years, with around 85% in drive-thru format. The expansion will leverage a mix of franchised (60%) and corporate (40%) stores.

GYG also expects margin improvements over the medium term through corporate operating leverage, increased contributions from higher-margin drive-thru outlets, tiered royalty benefits, and efficiency gains in general and administrative costs. The company is targeting an EBITDA margin of about 10% of network sales.

Share performance of GYG

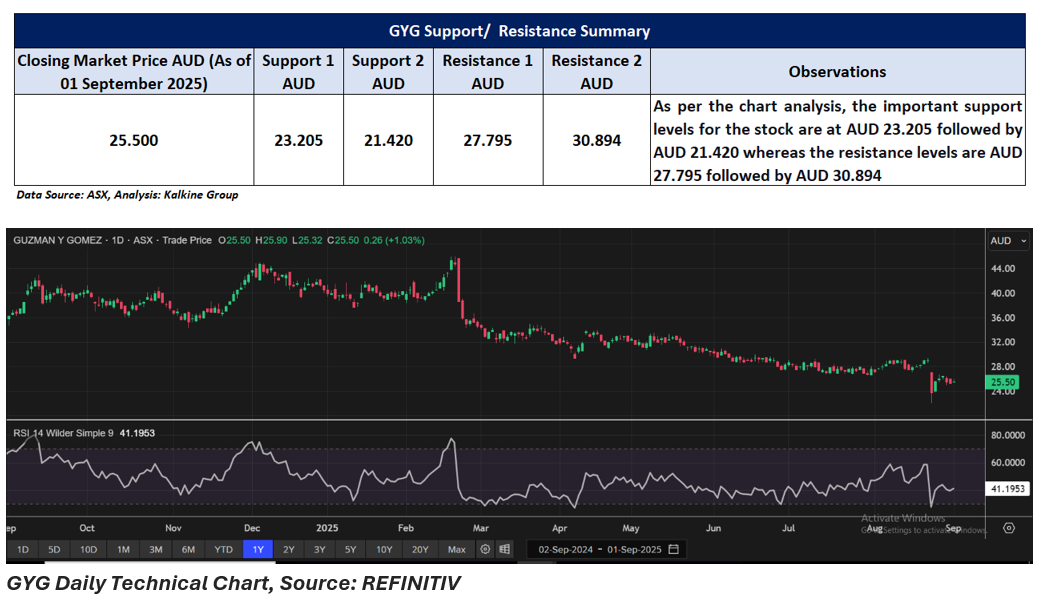

GYG shares gained 1.03% to close at AUD 25.500 per share on 01 September 2025. In a year, GYG’s share price has declined 28.17%. It is down 25.89% over six months, 7.37% over one month, and 0.16% in the past week. Over the past three months, share price dropped 15.70%, while year-to-date it has fallen 37.15%. The 52-week high is AUD 45.990, recorded on 19 February 2025, and the 52-week low is AUD 22.000, reached on 22 August 2025.

Support and Resistance Summary

Note 1: Past performance is neither an Indicator nor a guarantee of future performance.

Note 2: The reference date for all price data, and currency, is 01 September 2025. The reference data in this report has been partly sourced from EODHD/Others.

Technical Indicators Defined:

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Disclaimer

This article has been prepared by Kalkine Media, echoed on the website kalkinemedia.com/au and associated pages, based on the information obtained and collated from the subscription reports prepared by Kalkine Pty. Ltd. [ABN 34 154 808 312; AFSL no. 425376] on Kalkine.com.au (and associated pages). The principal purpose of the content is to provide factual information only for educational purposes. None of the content in this article, including any news, quotes, information, data, text, reports, ratings, opinions, images, photos, graphics, graphs, charts, animations, and video is or is intended to be, advisory in nature. The content does not contain or imply any recommendation or opinion intended to influence your financial decisions, including but not limited to, in respect of any particular security, transaction, or investment strategy, and must not be relied upon by you as such. The content is provided without any express or implied warranties of any kind. Kalkine Media, and its related bodies corporate, agents, and employees (Kalkine Group) cannot and do not warrant the accuracy, completeness, timeliness, merchantability, or fitness for a particular purpose of the content or the website, and to the extent permitted by law, Kalkine Group hereby disclaims any and all such express or implied warranties. Kalkine Group shall NOT be held liable for any investment or trading losses you may incur by using the information shared on our website.