Summary

- Australia has officially entered a financial recession after almost 30 years of uninterrupted growth.

- Australian GDP has fallen by 7% in the last financial quarter, marking the biggest fall since 1959.

- The last recession that Australia experienced was in the early 1990s, with a 1.7% drop in GDP. The impact on unemployment lasted until 1994.

- The two recessions have a lot in common – the Victorian state suffered the most.

- It is believed that the recovery will be long and hard, but the situation could have been a lot worse if not for wage subsidies that helped the Australians in need.

Australia has officially entered a financial recession due to the impact of the coronavirus pandemic. The prosperity had lasted for almost 30 years, one of the longest prosperous periods for any nation.

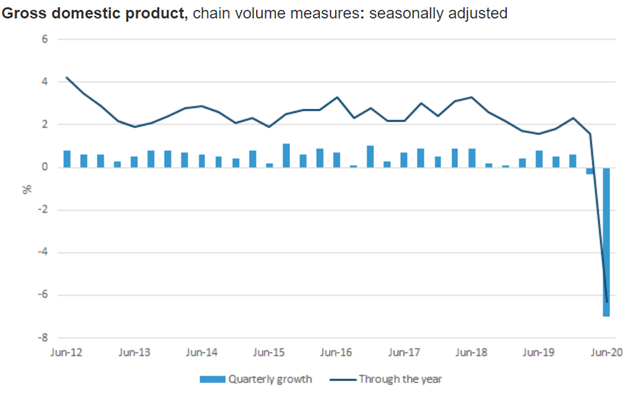

Australian Bureau of Statistics (ABS) reported today that Australia experienced the biggest GDP fall in the April to June period. A 7% drop has been recorded, which is the biggest since 1959 when Australia started tracking its figures.

Source: Australian Bureau of Statistics

By introducing two stimulus packages, JobKeeper and JobSeeker, Australia ensured that the situation did not get worse. The outcome could have been devastating if not for the government support. It is believed that JobKeeper and JobSeeker helped in stimulating the economy when Australian citizens were forced to save every penny they had.

Australian Treasurer John Frydenberg stated that without the wage subsidies, many more Australians would have lost their jobs, which would have resulted in a great economic catastrophe. It is estimated that around 700,000 jobs were saved due to the existence of JobKeeper. The Treasurer also expressed his concerns about the Australian future, stating that the economy’s recovery will be long and hard.

DO READ: Transiting from JobKeeper to JobSeeker: Morrison’s Government plan to boost employment

Historical timeline: 1990 Recession

Australia has been one of the most formidable economies in the world and can be proud of experiencing just one recession in nearly 30 years before declaring the 2020 recession.

The last recession was noted in the September quarter in 1990, due to the inflation of necessary goods in the 1980s. Because of that, Treasurer Paul Keating from that period became famous for the statement that Australia needed to have that recession.

Comparing to the coronavirus slump, the last drastic GDP drop was 1.7%, which makes the current distress almost four times bigger than the one in the 1990s.

The state of Victoria faced the worst financial consequences back in the 1990s, which does not look too different from a current situation, due to the declared emergency state in Victoria.

The unemployment rates were increasing in the early 1990s and had been rising until late 1992.

In 1994, the unemployment fell (being less than 10%), as well as the inflation, due to the economic recovery called Working Nation.

Global Virus Crisis Induced Recession

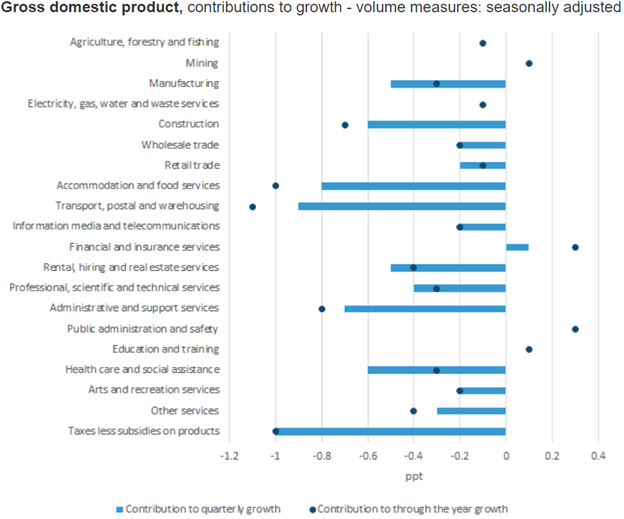

Strict movement and lockdown restrictions have impacted the life that Australians were typically used to. The tourism and hospitality crashes were the main contributors to the 7% GDP drop. After the Government decided to shut down international borders, other states within Australia followed, closing borders for personal travel.

Prime Minister Scott Morrison urged all the states to open state borders by Christmas, but his message was not very welcomed by the people, as the COVID-19 situation still appears to be harmful.

Apart from tourism and hospitality, other industries that were hit the most were education, arts, and event industry. Due to the international borders being shut, many international students got stranded abroad, not being able to travel to Australia, or simply being afraid of the coronavirus uncertainties.

Source: ABS

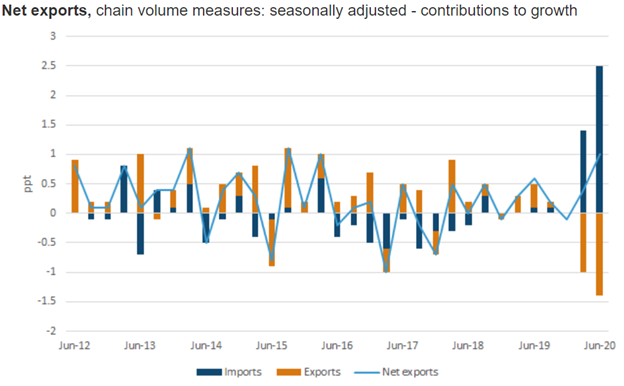

The trade war with China made the coronavirus situation even worse, resulting in a 6.7% drop in exports.

As Australia’s biggest trade partner, China’s boycott on importing seafood, beef and barley did not bring any good news for the Australian economy.

ALSO READ: The milieu between China and Australia when it comes to trade talks

Compared to exports, imports have seen a much bigger fall (12.9%), due to travel restrictions. That change was mostly felt within chains (e.g. Kmart), which suffered a major supply shortage.

Source: ABS

Outlook: Any Emerging Positive Signs?

It is estimated that the quarantine cost would be ~A$12 billion, and the estimate has not considered the most recent lockdown in Victoria (Victoria accounts for ~¼ of the Australian GDP).

More than 400,000 Aussies are expected to lose their jobs, or at least have fewer working hours than they had before.

Some businesses have seen increased sales (e.g. food delivery services, furniture, and technology retail stores), but those that were hit experienced a significant downfall.

Australians are urged to feel more confident about the future and are encouraged to stimulate the economy by supporting small local businesses. That seems to be the first and most logical step to get back on track.

Right now, Australia has a debt worth more than A$80 billion, and it is expected to grow even more.

However, this week marked some promising updates on the economic front. The ABS data announced this morning indicated a 3.2% seasonally adjusted growth in retail turnover for July 2020, driven by impressive sales in household goods.

Further, ABS reported a 12% increase in the number of dwellings in July, indicating an improvement in consumer sentiment. Coupled with a record current account surplus in the quarter ended June 2020, the recent economic updates indicate that there are some bright spots in the current situation.

With the RBA Governor Mr Philip Lowe highlighting that the monetary policy limits have been exhausted, all eyes would be on the Federal Budget 2020/2021, to be announced in October, with a focus on corporate tax rate cuts.

MUST READ: RBA retains cash rate at 0.25% yet again; Majority of ASX indices ended in red