Summary

- Incitec Pivot has a strong technology pipeline and is focused on delivering new technological advances on the ground.

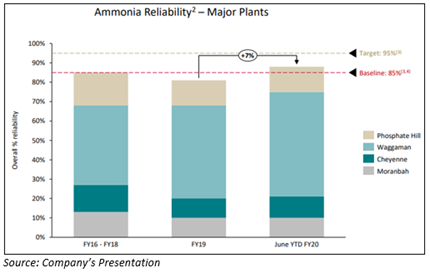

- Manufacturing performance continued its solid momentum from 1H 2020 across all main plants, with overall plant reliability up almost 7% at the end of June 2020.

- The developing Australian agriculture industry and improved rainfall conditions have been driving robust volume recovery in the financial year 2020.

A bear market leads to a sense of fear among investors. The situation only gets worse when the bearish levels persist for a long duration. However, experts suggest that such a scenario gives rise to several opportunities for market participants to grab. In such a scenario, an investor must remain calm and look for prospects in the market.

A bearish market eventually gets replaced by a bullish market, and an investor needs to bank upon the opportunity provided by the market to invest with a long-term outlook. Despite the negative sentiments around the bull markets, the good news is that they have always opened the way for long-term investors to choose high-potential companies at a low price.

DO READ: Guide to Invest in 2020 Bear Market

With this backdrop, we will discuss the ASX-listed Company Incitec Pivot, which seems to be on its path to recovery.

About Incitec Pivot Limited

Incitec Pivot Limited (ASX:IPL) is a manufacturer & distributor of fertilisers, explosives and industrial explosives. The Company is a leader in the agriculture and resources industries and is a member of ASX 100.

Incitec Pivot plays a crucial role in releasing the worlds natural resources through Dyno Nobel, to build infrastructure and generate the energy required to live in a modern world.

On 4 August 2020, Incitec Pivot updated the market with its investor’s presentation on the ASX.

Performance Update for Nine Months Ended June 2020-

The Company has strong technology pipeline and is focused on delivering new technology advances on the ground. Notably, CyberDet 2 wireless platform moving as per the plan of 2021 rollout on universal Gen 4 platform for mainstream requirements.

- Mining volumes in Australia for the nine months to June 2020 continue to be strong as the mining sector is operating well in a COVID-19 environment.

- Base & Precious Metals volumes YTD June 2020 remained strong, up 12% on pcp, with Metallurgical Coal volumes down by 4% compared to pcp due to lower contracted volumes and first half 2020 weather impacts.

- International volumes were down 12% compared to pcp, with lower demand from Thermal Coal customers in Indonesia, impacted by weather, changed mine plans and COVID-19

- Year to date June 2020 Quarry & Construction volumes were increased by 1% as compared to pcp, Base & Precious Metals volumes dwindled by 6% compared to pcp and Coal volumes fell by 21% compared to pcp.

- Fertiliser distribution volumes based on year to date June 2020 climbed by 16% on pcp, bolstered by above-average rainfall during January-June 2020 for much of southeastern Australia.

- Manufacturing performance continued its solid momentum from the H1 2020 across all main plants. The overall plant reliability at the end of June 2020 stood at 88%, up almost 7% from FY 2019.

HAVE YOU READ: 5 Reasons To Invest In A Tough Market Situation

Progress in manufacturing performance

- The Company is on track to deliver manufacturing excellence target by FY 2022.

- With almost 7% improvement on year to date, Incitec Pivot is on track to provide A$40 million to A$50 million earning uplift by FY 2022.

Incitec Pivot’s business remained resilient; Well set up for growth

- Key supplier to essential industries that have persisted robust through COVID-19 pandemic.

- Approximately A$60 million EBIT uplift per annum from anticipated cost savings by the financial year 2022, driving margin expansion.

- Growth projected from the fiscal year 2021, supported by premium technology offering.

- The Company to deliver A$40-A$50 million earnings uplift by FY 2022, driven by superior plant reliability.

- Advanced fertilisers products and services expansion, underpinning potential future growth.

- Substantial earnings leverage to current low commodity prices.

Fertilisers APAC- Incitec Pivot Limited is a prominent and the only integrated East Coast supplier of premium fertiliser solutions across Australia.

Incitec has robust long term fundamentals-

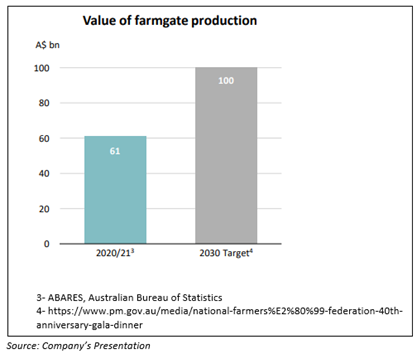

- Fertilisers are essential for enhancing agricultural productivity, with an estimated 5 million tonnes applied in 2019, approximately 70% in Eastern Australia.

- The Australian agriculture industry is developing, driving long-term demand for fertilisers.

Improving conditions-

- Wetter than normal conditions through large parts of 2020, supporting strong demand for fertilisers.

- Improved rainfall driving robust volume recovery in the financial year 2020, June YTD 2020 distribution volumes up 16% compared to pcp.

- Incitec disclosed that there is still a requirement to follow up rain to replenish water storage levels for irrigation requirements.

- Further development potential from the recovery of the irrigated Cotton industry with normalisation of rainfall.

Incitec also raised capital via an SPP and a Placement offer with the intent of using the proceeds for repayment of syndicated loans and hold a part of it as cash on deposit.

RELATED: Incitec Pivot Successfully Raises A$57.5 Million via Share Purchase Plan

Stock Performance: On 18 August 2020, IPL share price closed at A$2.140, a decline of 1.382% from its previous close. The market capitalisation of Incitec stands at A$4.21 billion, with nearly 1.94 billion outstanding shares. In the last three months, IPL has delivered a positive return of 11.57%.

Bottomline

Incitec Pivot is on the verge of transforming into a leading Australian soil health company and delivering new technology innovations on the ground. Incitec’s strong technology pipeline, and upcoming plans to roll out the technology in the future, demonstrate that it is moving progressively on its path of recovery.

GODD READ: Bear Market Brain Game-Do Markets Affect Your Brain While Jolting Your Pockets?