.jpg)

Summary

- The banking sector has fared better under COVID restrictions as compared to the Global Financial Crisis of 2008.

- Reforms carried out post the GFC have worked in favour of the banking sector.

- Banks have been able to defer loan payments and offer more lending with dedicated RBA support and robust liquid asset holdings at their disposal

- Increase in Non-Performing Assets, lending to new and risky borrowers and impact of loans forbearance on capital positions are critical challenges faced by banking players.

- Issues like operational capacity, technological failures and cyber-attacks are additional challenges to the new norms under COVID.

Recovering from the after-effects of a pandemic requires robust measures in all sectors. With international borders shut for months now, Australia has seen a demand shock coupled with an unparalleled unemployment rate. The economic contraction observed in some economies post the pandemic is heightened to a level seen only during World War II.

Amidst this chaos, the financial sector seems to have adjusted to these shocks quite smoothly, as per the recently released report by RBA, namely ‘Financial Stability Review – October 2020’. Although, there are some ramifications brought along by the low interest rates policy of the RBA, the financial sector seems to have been relatively less affected than the other sectors.

ALSO READ: Australian Economy: RBA toes the line, keep the rates unchanged at an all-time low

This may come as a surprise as the banking sector was the eye of the storm during the Global Financial Crisis (GFC), another Black Swan Event like COVID-19.

According to RBA, banks have fared adequately well, if not exceedingly well, during the pandemic. This has been made possible because of larger assets with bank this time than in 2008. Moreover, the faith in banks has remained intact even in the face of a global economic crisis. This is immensely important as during GFC, consumer confidence in the banks was lost and the financial sector came crashing down as a consequence.

GOOD READ: Australian Banking Space Amidst Virus-Induced Volatility; Digitalisation Turning Over a New Leaf

Health Is Wealth: Holds True for Banking Space

The health of the financial sector is of prime importance for key economic operations to function smoothly. With liquid asset holdings at their disposal and RBA’s liquidity operations in place, the banking sector absorbed the blow of the pandemic. Things have moved in positive direction for banks as the risks attached to financial sector has been shifted to the risks attached to an uncertain economic recovery.

RBA stated that the financial markets did, however, face the consequences of a slowed economy earlier in March. Early periods of the lockdown saw a sharp re-pricing of assets and a greater demand for liquidity. While stabilisation was achieved due to the unexpected policies by the Government. Without the knowledge of an upcoming Government policy, people’s expectations do not adjust in order to accommodate the forthcoming changes. Thus, the intended outcome of the policy was achieved.

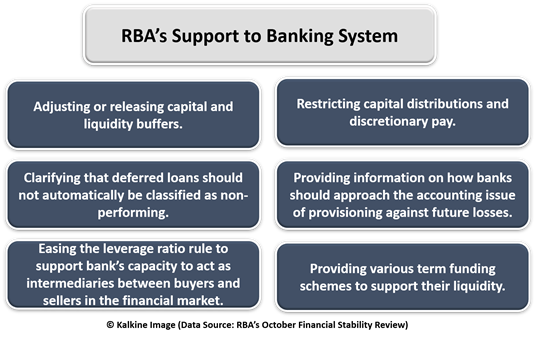

The reforms carried out post the GFC seem to have worked in favour of the banking sector in 2020. With greater resilience to shocks, RBA believes that the banks were able to continue lending.

According to RBA, the median Tier 1 capital ratio, which is the ratio of its equity capital and disclosed reserves to its total risk weighted assets, was 15% in large banks. Adding to this, effective policies post 2008 enabled the banks to function normally and stay stable. Credit extended by banks has promoted expansion of the economy by increasing consumer spending.

These benefits to banks have seeped down to the consumer level as well. Due to the above regulations banks are able to defer loan payments and offer more lending to people and businesses in need. Moratoriums have been offered on residential loans as housing property also struggles with excess supply.

Risks Faced by the Banking Sector

Economic recession fuelled by serious job losses and salary cuts comes attached with a risk of an increase in Non-Performing Assets. It is expected that there will be a rise in NPAs during the pandemic. As people are unable to repay loans and they delay on their mortgage payments, there is a lurking fear that these would become non-performing.

Another issue of concern is lending to new borrowers. Banks are likely to avoid lending to new and risky borrowers.

The forbearance offered on mortgage loans might be the need of the hour. However, RBA projects that it might harm the banks’ capital positions if the current situation persists for too long.

Though fairly protected in the fiscal aspect, banks still face operational risks. A new string of unforeseen challenges has risen because of the pandemic. Issues like operational capacity, technological failures and cyber-attacks are additional challenges to the new norms under COVID.

RELATED READ: Growing Role of Cybersecurity Firms as Work from Home becomes the New Normal-TNT, NET

Banking Sector Tailwinds

The banking sector has cushioned what otherwise would have been a rough landing for the financial sector that took off on a downward journey after the pandemic.

Many policies that encourage better lending practices under the scenario of contracted demand have been the harbingers of financial sector stability.

RBA estimates that because of increased provisions, bank profits have fallen by 50% compared with the previous half year and return on equity has gone well below its average.

Regardless of these challenges, the banking sector has fared well and has seen a lesser number of faulty borrowers and maintains stable profits.

When put under stress tests, banks have performed well thus adding to their credibility even in these uncertain times. It is important to note that these stress tests may not always adapt to all situations as they have been based on models.

All of these factors have contributed to a strong and stable financial sector in Australia which has further cushioned the rest of the economy.