_06_15_2026_08_31_29_563066.jpg)

Summary

- Housing prices started a recovery path albeit on a slippery slope.

- Few capital cities recorded an increase in housing price index in September, according to latest CoreLogic monthly data.

- However, property prices declined by 0.9% in Melbourne, 0.3% in Sydney and by 0.1% nationally in September.

- Lack of demand for property stands at the epicentre of this price decline.

- Increased unemployment levels in the post pandemic scenario and halted immigration are the causal factors behind this lack of demand.

- Lower interest rates might create the window to invest in housing as borrowing becomes less costly.

- According to RBA, complete and total recovery might take a longer time.

With the economy locked in a crisis mode, Australia’s struggle to stabilise its property market continues as housing prices show a downward streak at the national level for the month of September. Housing prices declined by 0.1% nationally in September 2020.

However, notably, the 0.1% dip is the smallest since home prices started to decline since May.

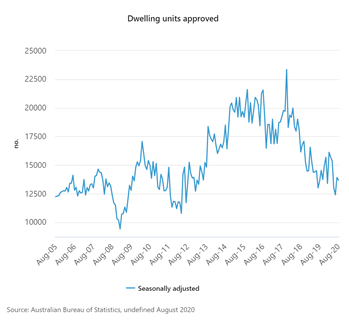

Besides, as per the latest ABS data, the total number of dwelling approvals fell by 1.6% in August. Private sector dwellings other than houses fell by 11%, while private sector housing rose by 4.8% in August.

Recent data by CoreLogic suggests that prices have increased in some parts, contrary to the expectations. This recovery, however, is limited to regional markets as major markets in Sydney and Melbourne, which comprise a total of 40% market share, struggle to recoup.

Sydney experienced a housing price index increase in August 2020. However, this did not carry over to September when prices fell down by 0.3% in Sydney. This temporary momentum can be credited to easing of lockdown restrictions, but a long term solution seems imperative.

Capital cities such as Canberra, Adelaide, Hobart, Perth, Brisbane and Darwin recorded a surge in property prices duringSeptember 2020. While, Melbourne and Sydney were at the root of the national decline. Prices decreased by 0.9% and 0.3% in Melbourne and Sydney respectively. Notably, a 2% decline in capital cities and a 4% rise in the combined regional index were observed.

The property space seems to be getting out of the woods, with some sort of optimistic trends seen in capital cities (except Melbourne and Sydney). However, demand driven factors need to be closely monitored in near term in view of overall labour market scenario and gradual withdrawal of government support.

ALSO READ: Is the Australian real estate sector likely to get out of the woods in 2021?

Demand Scenario for Property Space

Rental housing seems to have taken the biggest blow due to the curbed activity in the property market. This can stem from a varied number of reasons. To begin with, unemployment rates in Australia have reached an unprecedented state post the pandemic.

With job losses on the rise and the lack of immigrants into the country, a demand deficit has manifested in the housing market, particularly for renting market. In a scenario where supply remains more or less the same but demand cuts down abruptly, a rise in prices is inevitable.

The need for creating remote employment under lockdown restrictions has led to people shifting away from the capital housing hubs and move back to regional cities. This could explain the positive figures seen in the regional cities while the same is not observed for Melbourne and Sydney.

Another possible explanation for the increase in demand for property in the regional area can be a change in lifestyle. Containment measures have mandated the prohibition of public gatherings and people have become wary of densely populated areas. Thus, moving back to less populated cities serves this purpose.

To look at August property scenario, CLICK HERE!

A Brief History of the Australian Property Sector

Australian property rates are considered one of the highest in the world. The surge in Australian housing prices began around 2014-2015. Some theories suggest that an infrastructural boom set in after the year 2000 when Australia hosted the Olympic Games. This set in motion the high property rates.

However, prices apparently peaked around June 2017. The subsequent plunge taken by property rates can be the outcome of a housing market bubble much like the one observed in 2008. It was speculated that the Australian housing market was highly overvalued and was headed for a crash.

Sydney rates had already fallen by 5-10% over the course of one year from 2018-2019. Though slight and gradual recovery was observed in the property market since late 2019, excess supply of property was a pre-pandemic issue which led up to the softening of the housing market under current pandemic-induced restrictions.

Speculators expected the prices to drop further and by June 2020 the observed drop in prices exceeded these expectations.

RELATED READ: How did the economy get affected by the pandemic?

What Does the Future Hold for the Australian Housing Market?

The decline in the property prices is further expected to exaggerate in the coming months. Although, a staggered but steady growth in the regional markets paints an optimistic picture, it may not compensate for the decline in capital markets.

The soaring unemployment figures, lack of immigration and hence an overall demand deficit continues to inflate the problem.

The Government has introduced policies aimed at healing the economy. Moratoriums have been offered to tenants who have been affected by the job losses and payment cuts. Landowners were offered land tax relief under the condition that they offer some cuts on the rental payments. Certain states even offered cash payments to tenants to ease the burden of payments on them.

RBA states that the deferments and moratoriums offered to tenants have been effective. RBA also claims that prices have adjusted in the housing market; however, it is evident that capital cities Melbourne and Sydney continually showed a decline in housing price index, till the last day of September 2020.

These two cities are especially important as they hold a major stake in the housing market. Their negative numbers have overcompensated for the increased prices in other capital cities as well as regional markets. This might continue till lockdown restrictions are brought to a complete halt.

Low housing demand, primarily amidst a decline in overseas students due to international travel restrictions, may create pressure on rent and vacancy rates in areas of inner-city suburb.

The Path to Total Recovery

According to RBA, complete and total recovery might take a longer time. The pace of growth is quite slow and is partial. RBA is hopeful that once international borders are opened and immigration resumes, the demand will pick up and economy will stabilise. It may also give rise to rental housing agreements.

Till then, RBA’s strategy lies in lowering interest rates to encourage borrowings, providing moratoriums on housing payments and deferring rental payments.

These seem to work for now, however the positive aspects associated with these policies might dissolve in the long run. A different course of action would then be necessary.

DO NOT MISS: All that you need to know about RBA's toolkit