A global media and entertainment company, Crowd Media Holdings Limited (ASX: CM8) recently implemented some cost-saving measures to move back to profitability. The companyâs Crowd Media division is on a pathway of strong growth trajectory with the recently executed agreement with Moneyfarm as well as the new 3rd party agreements for its digital marketing services. Besides the ongoing strategic review, the company is exploring additional ways to improve shareholder value. Around one year back, the company had disclosed some of its growth strategies for the financial year 2019.

The four growth strategies that the company followed in FY19 are as follows (Source: 2018 Annual Report):

- Accelerate Crowd agency growth by leveraging the global social media platform of Q&A

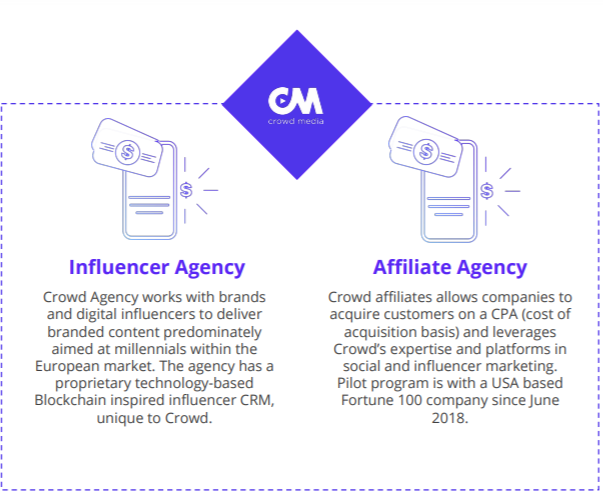

Crowd Agency works hand in hand with brands as well as digital influencers to deliver branded content, which is focused on millennials. By executing advertising campaigns for global brands and leveraging the social media and influencer distribution network, the company is achieving growth in its agency division. The network that the companyâs Q&A division has built up in over 30 countries is coming in handy for the Agency division, which is leveraging it to accelerate more growth.

- Diversify Crowd Media revenues with minimal investment by selling third party (affiliate) products through the existing platform:

As discussed above, the companyâs Media division is on a pathway of a strong growth trajectory. In FY19, the company was focused on diversifying its Crowd Media revenues with minimal investment by selling third party (affiliate) products through the existing platform, with an intention to flourish this division.

In line with strategy, the company had executed 3rd party agreements for digital marketing including digital influencer marketing for multiple international brands which include a famous kid TV Series -PJ Masks, a leading travel website- Expedia, a leading Fintech challenger bank in Europe- N26 and Italyâs leading pasta brand - Pasta Garofalo, as announced on 15 May 2019.

In FY2019 the company was focussed on selling its digital subscriptions to millennials using social media marketing expertise. Although the FY19 results are not yet disclosed, the companyâs media division expects to witness revenue growth of 240% in the year, taking revenues to around $1.7 million as compared to $0.5 million in FY18.

For FY2020, the company will keep its focus on bringing globally competitive social media and digital influencer campaigns to clients and expects to generate substantial revenues with strong YoY growth, taking the Media Division to new heights of achievements.

- Continue to grow Q&A business through product pivots:

The company is already a world-leading Q&A entertainment & technology service provider, and in FY2019, the company efforts were focussed on further growing this division through product pivots. During the year, the company was focussed on opening new growth channels beyond millennials through product pivots targeted at other demographics and expanding social media platforms while maintaining profitability in Subscription business by expanding content and payment options.

Crowd Media Divisionâs Products (Source: Company reports)

Crowd Media Divisionâs Products (Source: Company reports)

For FY19, the company expects to earn revenues of around $23 million. And in FY2020, the company is intensifying its efforts to stabilise and grow the revenues and profits of its Q&A and Subscription mobile businesses via new products and new geographic markets.

- Leverage technology to optimise margins to further invest in growth:

In FY19, the company was focussed on leveraging Artificial Intelligence (AI) and Business Intelligence (BI) technology to reduce its down costs and further optimise its Return on Investment (ROI). Along with that, the company was focussed on neutralizing its Q&A operator costs through third-party revenue streams.

Overview of Strategic Review: In order to move back to profitability and to restore shareholder value, the company had commenced a strategic review which was first announced to the market in mid-April 2019. Following the review, the company identified several areas where it can save some money.

As a result, CM8 executed numerous cost-cutting measures in FY19, which may translate to an annualised cost savings of ~ $3.5 million. The company had already reduced $1.4 million in annualised costs with the latest redundancy round, which included changing the CEO and Boardâs remuneration to help conserve cash.

To fund the various redundancies, the Company secured a Convertible Note to raise $0.75 million which will be used to fund the employee exits as well as for providing working capital to fund future initiatives.

The companyâs CEO has agreed to accept 50% of his salary in Crowd Media shares in lieu of cash for FY2020 and likewise, the Chairman and Board have also agreed to accept 25% of their fees in Crowd Media shares in lieu of cash.

Under the guidance and management of a highly experienced and skilled Board of Directors, the company is very well placed to bring value to its shareholders. The companyâs Board includes:

Theodore Hnarakis (Non-Executive Chairman)- a well-seasoned industry veteran who has plenty of experience in the media industry and scaling up ASX-listed technology businesses;

Domenic Carosa (CEO & Executive Director)- a popular Internet leader who had played an important role in creating and establishing various other big firms;

Sophie Karzis (Company Secretary and Non-Executive Director)- A member of Law Institute of Victoria and the Institute of Chartered Secretaries with over a decade of experience as a commercial lawyer.

To know more Click here - A Quick Look at Crowd Mediaâs Think Tank- Board of Directors

At market close on 30 July 2019, CM8âs stock was trading at a price of $ 0.020 with a market capitalisation of circa $4.98 million.

Disclaimer This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. The above article is sponsored but NOT a solicitation or recommendation to buy, sell or hold the stock of the company (or companies) under discussion. We are neither licensed nor qualified to provide investment advice through this platform.