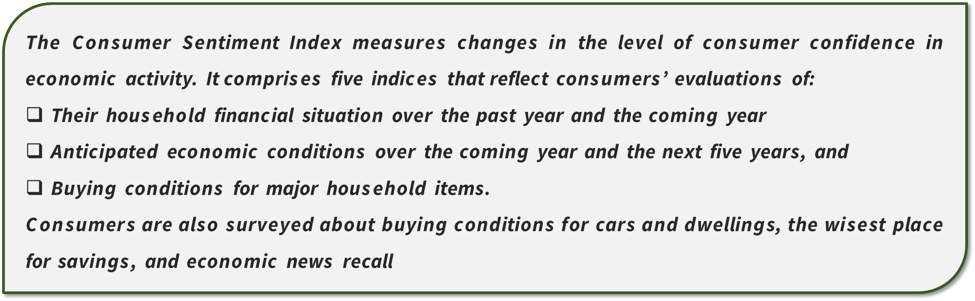

A decline of 1.8% in the Consumer Sentiment Index was declared on 22 January 2020 to 93.4 from 95.1 in December by the Westpac-Melbourne Institute Index of Consumer Sentiment. This came as an effect of the devastating bushfires that is threatening Australia’s livelihood. However, the decline is not as intensive as the one at the time of Queensland floods in 2011. The Index, during the Queensland floods in 2011 had witnessed a fall of 5.8%.

The overall confidence levels during the Queensland floods period in 2011 were much higher than the current confidence levels, and the fall in the Index during the floods was from 111.0 to 104.6.

Notably, the Index has printed below 93.4 in only seven monthly readings since the lows of the Global Financial Crisis (where the Index averaged only 89 over a 15-month period from March 2008 to May 2009).

According to Westpac Banking Corporation (ASX:WBC)-

- The ‘economy, next five years’ sub-index fell 3.7% in January and the ‘economy, next 12 months’ sub-index fell 5.4%, sharply down on a year ago (–8.9% and –11.9% respectively);

- The ‘time to buy a major household item’ sub-index fell 1.8% in January,

- Currently, the sub-index stands at 113.4 which is well below its long-run average of 127 and 4.1% down on last year,

- This suggests that the consumers are likely to be extra cautious, particularly in December and January;

- The ‘finances vs a year ago’ sub-index rose 0.7% in January and the ‘finances, next 12 months’ sub-index increased by 0.9%, both down by 3.1% and 3.2% respectively on a year ago.

On the side of factors promoting optimism, the Australian share market has gained 6% since the start of the year, maintaining positivity in financial markets and lifting the global economy. In addition to this, the fair housing market conditions further pointed to ongoing confidence in the housing market.

Westpac-Melbourne Institute Unemployment Expectations Index

Firstly, it should be noted that higher readings in the Westpac-Melbourne Institute Unemployment Expectations Index indicates the expectation of more consumers’ unemployment to rise in the year ahead. The Index fell 2.9% to 134 in January, representing an increase of 8.4% as compared to the same time in the previous year. Westpac sees this to be in uniformity with the slowdown in jobs expansion and the expected stable rises in the underemployment and unemployment rates over the upcoming year.

Moreover, Westpac expects an increase of 5.6% in the rate of unemployment from 5.2% during the journey in the first half of the current year.

The Black Friday Effect

Westpac believes that the unexpected jump in retail sales reported for November could be largely influenced by the Black Friday effect. Additionally, the current levels of the increment in the spending do not form convincing arguments for debating the negative indicators linked with the regularly occurring low levels of the Index.

The Australian Bureau of Statistics (ABS) provides the following facts about the Australian Retail Trade for November 2019:

- The trend estimate rose 0.3% in November 2019 following a rise of 0.3% in October 2019 and a rise of 0.3% in September 2019;

- In trend terms, Australian turnover rose 2.9% in November 2019 compared with November 2018;

- The seasonally adjusted estimate rose 0.9% in November 2019 following a rise of 0.1% in October 2019 and a rise of 0.2% in September 2019;

Housing-related Sentiment

With views on time to buy lifting while price expectations continued to surge in January, Housing-related sentiment was solid, wherein:

- The ‘time to buy a dwelling’ index rose 5.7% in January to 118.8, nearing the long-run average of 120;

- The index is down by 6.4% from its peak in August, shortly after the low point for prices which occurred in June;

- On the basis that the current level of 118.8 compared to a low point of 90.0 in the previous cycle, it is likely that the price gains have further to run;

- The speed of house price appreciation may slow if this Index loses ground through 2020;

- Sydney and Melbourne now sit at 117.4 and 105.8, off the recent peaks of 130 and 133 respectively;

There was a rise of 8.1% in the Westpac-Melbourne Institute Index of House Price Expectations Index in January to 151.48, representing a stunning 58% increase over the year.

The boost in optimism has not been as dramatic as witnessed in this cycle; however, the Index has reached higher levels in previous price cycles. Moreover, it is possible that valuable lead indicators shaping the current house price cycle may be offered by the Time to Buy Index and the House Price Expectations Index, while they also look like indicating continuity in the positive price action of the current period to last in the near term.

On the other side, The Reserve Bank Board is scheduled to meet on 4 February 2020, in which Westpac expects a cut in the cash rate by 0.25% to 0.5%. If there are rate cuts, it is likely to be influenced by the downgrade in the growth forecasts for 2020.

In terms of the global trade trends, an increasing breathing space is sensed in international trade after signing of the phase one trade deal between the US and China. However, the terms of trade look like hurting other countries in the play, but the bigger picture of the tensions look like demystifying gradually.

For more details about the Phase one of the trade deal, follow: What does Phase one Trade deal mean?

Another defiance to the damaged consumer confidence is the record performance of S&P/ASX 200. Since the beginning of 2020, the ASX index has been increasing to a record high, and we witnessed the market closing at higher notes, notwithstanding the downgrades in the earnings forecasts by some of the companies, especially in the consumer discretionary.

Good Read: Surging ASX Defies Downgrade Warnings

Bottomline

The survey was undertaken by Westpac in the week of widespread rain after the bushfire where the negative impact of the bushfires had somewhat reduced. However, the fall in the Index would have been much intense if Westpac would have conducted the survey a few weeks earlier during the time of bushfire, notwithstanding the very low starting point. Although consumer confidence seems crippling, we have seen rising positivity in the global economy as well as the stock market along with rising prices in the housing market.