The financial sector of Australia is the largest contributor in the GDP of the country and is also a significant contributor to the economic growth of the nation. In FY 19 period, the Australian companies have faced the impact of Royal Commission, and interest rates cut by the various banks.

Navigator Global Investments Ltd

Strong Performance in FY 19:

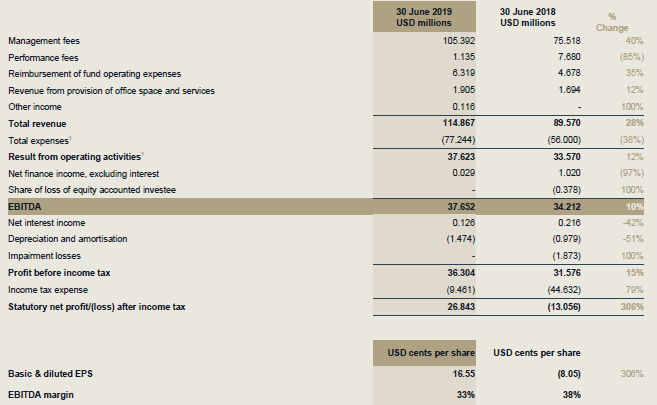

On 8 August 2019, Navigator Global Investments Ltd (ASX: NGI), that offers investment management services, released its full year results, for the period ending 30 June 2019 and has reported whopping rise of 306% in net profit to US$26.84 million, a 28% growth in revenue to ~US$114.9 million and a 10% increase in EBITDA to US$37.65 million.

Also, during FY 19 period, the Management fee revenue grew by 40% to US$105.4 million due to 51% increase in the average total AUM. The company has posted US$6.5 million decline in the Performance fee revenue for the 2019 to US$1.1 million on the previous financial year. This is driven by the lower investment performance of the company across the portfolios. During FY19, the company from operating activities has generated US$22.6 million. The company in full year 2019 has paid $27.5 million to shareholders as dividends, had net paid for investments in unquoted securities of entities managed by Lighthouse of US$1.6 million, had paid for leasehold improvements and acquisition of equipment of US$1.5 million and has paid for transaction costs associated with the MAS transaction of US$1.1 million. Additionally, during FY 19 period, the companyâs investments in Lighthouse funds has risen by US$1.8 million to US$12.7 million. The companyâs investment in external entities during the period is of US$5.3 million versus US$5.6 million in FY 18. At the end of FY 19, the company had cash & cash equivalents of US$29 million.

FY 19 Financial Performance (Source: Companyâs Report)

On 12 August 2019, NGIâs stock last traded at A$3.560, down by 2.198 percent from the prior close. Meanwhile NGIâs stock has provided with a negative return of 8.77% in the last three months duration and traded at a P/E ratio of 15.76x.

Eclipx Group Limited

Divestments & Subdued Performance in 1H 2019:

Eclipx Group Limited (ASX: ECX) has recently on 31 July 2019, notified the market that it had sold GraysOnline and AreYouSelling to Quadrant Private Equity for the total consideration of A$60 million. The net proceeds from these divestments will be used to pay debt.

The company intends to concentrate on its core fleet leasing and novated businesses. The company has planned the divestment of two of its businesses, and a strategic review of another 2 sub-scale businesses. This is apart from AreYouSelling & GraysOnline.

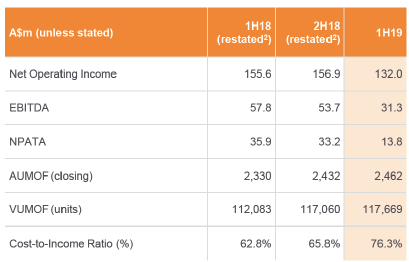

On the other hand, for the first half of 2019, the company has reported 62% decline in the net profit after tax and amortisation (NPATA) to $13.8 million on the back of underperformance in the non-core businesses, like GraysOnline, Right2Drive and Commercial Equipment. Further, the company had posted (statutory loss after tax) standing at $120.3 million compared to (profit after tax) which stood at $25.0 million during the 1H18 period. This comprised of the $118.4 million (after- tax non-cash impairment of goodwill) pertaining to its businesses namely - GraysOnline and Right2Drive.

ECX during 1H 2019 had not declared the interim dividend for the period. Further, during the first half of 2019, the companyâs core fleet and novated businesses had posted 3% fall in the EBITDA to $40.7 million. Net Operating Income (before end of lease and impairment) of the companyâs core business has risen 3 percent, at $73.3 million, whereas its operating expenses had witnessed a marginal decline. Total assets under management or financed (AUMOF) during the period increased 7% to $2.1 billion and Total vehicles under management or financed (VUMOF) increased by 6% to 103,414.

1H FY 19 Financial Performance (Source: Companyâs Report)

On 12 August 2019, ECXâs stock last traded flat at A$1.465, up by 2.198. The stock has provided with a negative return of 45.77% in the last three months period.

Clearview Wealth Ltd

Preliminary FY 19 Performance:

Clearview Wealth Ltd (ASX:CVW) in its preliminary report for FY 19 period released on 18 July 2019 was anticipating for the FY 19 results - the Underlying NPAT of $25.1m, including $1.8m of adverse impact on FY19 performance on the back of the change in income protection claims assumptions. For the year 2019, the company has reported NPAT of $4.0m, including the positive outcome driven by lower discount rate in policy liabilities (net of a change in CPI assumptions), which is however, offset by impairment write-off of Goodwill, Intangibles and other costs that is not directly related to ordinary activities. The company during the second half of 2019 has completed the significant cost transformation program and IT strategy review.

The company in 2H FY19 period has ended some poor performing life insurance distribution relationships. CVW had further repriced and enhanced the life insurance and wealth management products. In the second-half the company had reviewed its financial advice business strategy, dealer group pricing model and had also launched LaVista Licensee Solutions. The company had positioned its life insurance business to grab the opportunities that will arise from the breakdown of vertical integration and the opening up of APLs. Further, the Embedded Value for 2019 is expected to be approximately $671.5m as on 30 June 2019.

Moreover, the company has been considering a share buyback program, which would depend upon the market conditions and ClearViewâs overall capital management strategy.

On 12 August 2019, CVWâs stock last traded at A$0.690, up by 6.154 percent from the previous closing price. The companyâs stock has provided with a negative return of 18.75 percent during the last three months and traded at a P/E ratio of 15.550x.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.