US Markets: American equities traded lower to moderately higher on Thursday, 4 November, with the tech leader Nasdaq Composite and the broader share index S&P 500 registering fresh record highs, while Dow Industrials traded in the negative territory as shares of Dow, Goldman Sachs, JPMorgan Chase, Cisco Systems, UnitedHealth Group, Intel, Apple and Travelers Companies hovered in red.

After hitting record highs in the opening trades, US shares dropped slightly as market participants continued to contemplate the latest action by the Federal Open Market Committee (FOMC). With the US Federal Reserve announcing the anticipated tapering in the bond buying programme, the equities have seemingly welcomed the move. All the three major stock indices ended on a fresh record high on Wednesday.

The persistently falling number of US citizens seeking the unemployment benefits have constructively boosted the equity markets as it dropped to 269,000 for the week ending 30 October. This has been the lowest number of claims filed by Americans since the widespread emergence of Covid-19 pandemic in March of 2020. The continuous improvement in the employment landscape exhibits the pace of recovery, at a time when the corporations are resuming their respective operations at the biggest scale for the first time in the pandemic era.

Nonetheless, the acute limitedness of staff due to elongated inactivity in the job market in the recent past continue to hurt the businesses as they are not able to fill the positions with adequately skilled workers.

The Dow Jones Industrial Average shed 75.07 points, or 0.21% to 36,082.51, while the wider share indicator S&P 500 rose 15.38 points, or 0.33% to 4,675.95 and tech heavy barometer Nasdaq Composite advanced 100.44 points, or 0.64% to 15,912.03. During the day so far, S&P 500 has registered a fresh lifetime peak of 4,683 and Nasdaq has recorded a new all-time high of 15,961.25.

US Market News: Shares of Qualcomm rallied more than 12% after the wireless technology major reported better-than-expected earnings for the July-September quarter. Among the Dow constituents, shares of Merck & Co, Salesforce.com, McDonald’s, Home Depot, Walmart, and Nike emerged as the lead gainers, providing the biggest positive points to the market index.

Qualcomm and Nvidia were the biggest gainers among the Nasdaq Composite shares, the rally was supported by considerable rise in the stocks of Advanced Micro Devices, Xilinx, Costco Wholesale, Microchip Technology, Adobe Systems, Electronic Arts, Amazon, Tesla, and Alphabet.

UK Market News: London equities bounced back slightly after the Bank of England decided to hold the rates in the second-last Monetary Policy Committee meeting in the present calendar year. The weaker value of Great Britain pound (GBP) vs the United States dollar (USD) supported the equities as the central bank surprised investors by maintaining the rates at record low.

The domestic benchmark FTSE 100 gained 32.47 points, or 0.45% to 7,281.36, after hitting an intraday high of 7,292.96. The mid-cap indicator FTSE 250 vastly outperformed the headline index on Thursday. FTSE 250 rose as much as 377.99 points, or 1.64% to 23,494.96, after making an intraday peak of 23,565.07.

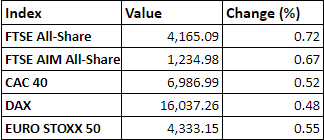

FTSE 100 (4 November)

Source: EODHD/Others

Market Snapshot

Top 3 volume leaders: Lloyds Banking Group, Vodafone Group, BP

Top 3 sectoral indices: Telecommunications, Electronic & Electrical Equipment and Engineering Products

Bottom 3 sectoral indices: Banking, Life Insurance and Consumer Services

Crude oil prices: Brent crude up 0.29% at $82.23/barrel; US WTI crude down 0.02% at $80.84/barrel

Gold prices: An ounce of gold traded at $1,793.85, up 1.70%

Exchange rate: GBP vs USD - 1.3506, down 1.30% | GBP vs EUR - 1.1694, down 0.74%

Bond yields: US 10-Year Treasury yield - 1.533% | UK 10-Year Government Bond yield - 0.9405%

Markets @ 16:25 GMT