Summary

- The US Federal Reserve, on last Wednesday, told that restrictions on share repurchases and dividend payments to shareholders will continue in the last quarter of the year.

- The agency highlighted that US banks remained strong from a capital standpoint in the third quarter, which ended in September.

- The Federal Reserve will conduct a stress test, and results would be announced at the end of this year.

Dividend stocks have been one of the favourite picks for many investors across time. Companies formulate dividend pay-out policies to cater to the expected needs of investors post taking the capital allocation decision into consideration. There has been a lot of focus on dividend and buy back decisions undertaken by companies in the US, especially financial players.

Last week, the US Federal Reserve extended measures to maintain a high level of capital resilience among banks in the US. It expects US large banks to remain highly liquid from a capital perspective since bad loans will deplete capital.

In Q4 2020, large banks with total assets of over $100 billion are now refrained from making share repurchases, while dividend payment would be capped based on the measures, which take recent income as a consideration.

During the third quarter ended in September, large US banks remained resilient in terms of capital position, highlighted the Fed. Earlier this year, the banking regulator released stress test results for the US banking system, underlining that large banks have been sufficiently capitalised amid the COVID-19 crisis.

Given the economic uncertainty considering COVID-19, the Federal Reserve believes restrictions on dividend and share buybacks will help to preserve capital for banks, while providing a floor for loan losses and support lending.

The Board will undertake another stress test at the end of this year to test the resilience of large banks. The market participants would closely monitor this since the upcoming stress test will undertake new scenarios where variables will be different.

June stress test outcomes

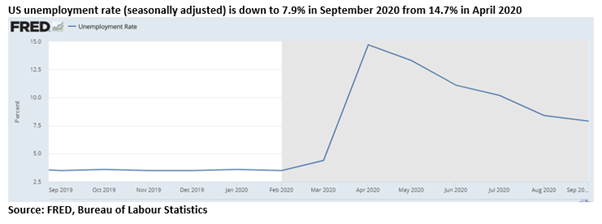

The test results had highlighted that loan losses for the US banks would be in the range of $560 billion to $700 billion for 34 banks. This scenario was possible when the unemployment rate would be between 15.6% and 19.5%. Likewise, under these circumstances, the aggregate capital ratios for the banks would be in between 9.5% and 7.7%.

These stress test results were forecast under three scenarios, which undertook V-shaped recovery, U-shaped recovery, and W-shaped recovery. Further, the Government stimulus packages unveiled in the wake of COVID-19 were not accounted under the analysis.

Good read: The US Fed Bats for Further Stimulus, Market Losing Hope?

Governor Brainard did not buy the idea of lower capital requirements. He had stated that higher capital buffers with the banks had provided resilience during the pandemic, while also allowing banks to initiate recovery.

He was of a view that lower capital requirements would halt the credit flow in the economy. The stress test undertaken by the Federal Reserve tested the ability of the banks to extend credit in the wake of economic crisis.

After the sensitivity analysis, they pitched for additional loss-absorbing capacity for several banks to limit the downside to capital buffers. Under some scenarios, the result depicted that many banks would be left operating in their stress capital buffers.

Past observations from the Federal Reserve have witnessed that credit conditions tighten when banks operate close to their mandatory capital requirements. In the absence of smooth credit flow in the economy, the recovery would be impacted.

Buybacks and dividends

In the US, trend in buybacks has shown that most of the US corporates prefer using share repurchases as a return to shareholders.

In the wake of ongoing economic crisis, which is expected to shoot bad loans for the banks, cash spending on shareholder returns would ultimately hurt the banks’ ability to meet capital requirements and extend credit.

Dividend restrictions formulated by the Federal Reserve direct banks to distribute income based on recent earnings. Under these restrictions, the banks cannot pay dividends or increase dividends unless sufficient income is earned.

The Board also told banks to re-evaluate the long-term capital plans of banks. They might have stressed the long-term capital plans because of the Basel III norms, which would in place over the next few years.

With interest rates at record low levels, banks with large lending business will likely suffer from lower-income and profitability. This will be added with the potential influx of bad loans, which would require provisions and even write-offs in many cases.

Must Read: Is the US set for low-interest rates for the next 3 years? The Fed believes so

(All currencies in USD unless or otherwise stated)