Summary

- COVID-19 induced sensitivity analysis showed that loan losses could be in the order of $560 billion to $700 billion for 34 banks.

- Governor Brainard has pitched for additional loss-absorbing capacity for the banks in light of uncertainty due to the pandemic.

- Banks are required to submit their capital plans, which should account for current stress.

The Federal Reserve has released results of stress tests of banks. In light of COVID-19, the central bank also conducted a sensitivity analysis on banks, which have gathered more attention than stress test results. The Board believes that the banking system has been rock solid in this crisis, and results from sensitivity analysis show the ability of banks to manage ‘harshest shocks’.

This time stress test of the US banking system was different than the previous stress tests. And, the Federal Reserve conducted the sensitivity analysis to ascertain resilience in the banking sector. For the COVID-19 sensitivity analysis, the central bank applied three scenarios- V-shaped recovery, U-shaped recovery, and W-shaped recovery.

In these three scenarios, the unemployment rate range was taken between 15.6% and 19.5%. Sensitivity analysis guided for loan losses between $560 billion and $700 billion collectively for 34 banks. It also showed that aggregate capital ratios could range within 9.5% and 7.7% from 12% in the fourth quarter of 2019.

This analysis did not consider the Government welfare payments and additional unemployment insurance. They found that most of the banks remain well capitalised, and several could test mandatory capital levels, under a U-shaped and W-shaped scenario.

Brainard Says No to Lower Capital Requirements, Pitches for Additional Loss-Absorbing Capacity

Governor Brainard stated that Dodd-Frank reforms had played an enormous role in enabling banks to respond to the crisis. He didn’t buy the idea of reducing capital buffers of the banks, which have proved their mettle during the COVID-19 pandemic, enabling banks to instigate a recovery.

Lowering the capital buffer requirements of banks will likely result in tightened credit flow to the economy, as banks would seek to maintain capital buffer at the heart of an economic crisis.

Stress testing continues to ascertain the resilience of banks during a crisis, and banks’ ability to maintain a smooth flow of credit. He noted that forward-looking sensitivity analysis indicates that several large banks will need additional loss-absorbing capacity to prevent downside to the capital buffers.

Due to looming uncertainty, the sensitivity analysis has wide range of loss rates and capital ratio results. Excluding authorised distributions and partially imposing increased risk in banks’ balance sheets, the testing showed that many banks could be operating in their stress capital buffer with one quarter close to mandatory capital requirements.

Related: COVID-19 Aftermath: US Real GDP expected to shrink by 5.6% in 2020

The sensitivity analysis did not account for the capital outgo as a result of distribution to common equity holders. In the past, the Fed had observed that when banks operate closer to their mandatory capital requirements, it results in tighter credit conditions, which could adversely impact the recovery.

Vice-Chair for Supervision, Quarles Says Capital Preservation is the Key

Vice-Chair for Supervision, Randal K. Quarles noted that the banking system entered the crisis with a position of strength, unlike the last crisis in 2007-09. United States’ largest banks had $1.2 trillion in common equity and $3.3 trillion in high quality liquid assets.

Federal Reserve also gave the nod to utilise these capital buffer to promote safe lending. Mr Quarles stated that over 70% of capital distribution by the largest and most systematic banks arrived through share repurchases in recent years, which have been voluntarily suspended by many banks in Q2 in an effort to preserve capital.

He also stated that there remains uncertainty on the recovery and its impact on banking organisations. And, the Federal Reserve would take necessary actions to ensure that banks maintain large capital reserves to prevent downside risks.

Related: Is the worlds’ beloved currency off for a downhill?

Suspended Share Buybacks and Dividend Tests

In the third quarter of this year, the Federal Reserve would need banks to suspend share repurchases; this would ensure that banks remain committed to preserving capital. The Board also requires banks to re-evaluate their long-term capital plans.

They have directed large banks to update current stresses in their capital plans, enabling banks to ascertain renewed capital needs. The Federal Reserve would review the capital plans of banks, and decide on the required adjustments.

Under the current system, the regulations allow banks to pay third quarter dividends based on the average income earned over the past four quarters. As a backward-looking measure, it conflicts with the essence of stress testing, which is to maintain forward-looking resilience in banks. Therefore, dividend payments based on previous income would deteriorate loss-absorbing capacity.

In 3Q, the Board has decided to limit dividend payment to the amount paid in the second quarter and based on recent earnings. Moreover, banks would not be able to increase dividend payments, and dividends could be paid when banks have earned sufficient income.

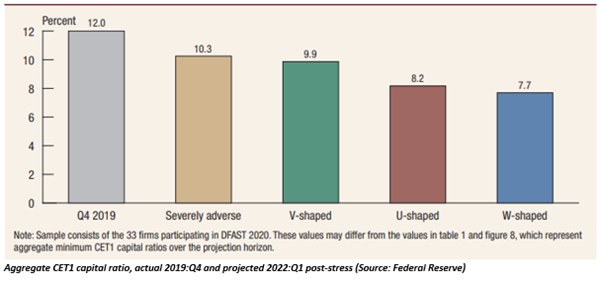

COVID-19 Sensitivity Testing Results of 33 firms

Under a severely adverse scenario, the aggregate CET1 capital ratio of the firms would be around 10.3% in Q1 2022. A V-shaped recovery is expected to take the aggregate capital ratio to 9.9%, while the ratio would be 8.2% in a U-shaped recovery. Aggregate CET1 capital ratio would be at 7.7% under a W-shaped recovery.

(All currencies are in USD)