Highlights

- An informed decision can change the quantum of profit one earns from any investment option

- APY and APR may sound identical, confusing, but both are poles apart, and simple to understand

- Fund managers and lenders may play with terms and words, hence it is best to know the basics

Money should make more money by itself – that’s the inspiration behind investing.

The next question is – how fast is your investment growing? There can be different ways to calculate the returns, and two of the most popular ones are annual percentage yield (APY) and annual percentage rate (APR).

Though both of these will help know the exact rise in the value that a person has invested, the calculations are not identical, which is why one may look attractive than the other despite the fact that real returns are the same.

APY vs. APR

A simple way to understand APY and APR is by knowing which industry player uses which of the two when advertising products.

APY

APY is quoted by investment companies and portfolio managers to draw the attention of investors to their products. This is because compounding the interest is an inseparable part of APY. Compound interest would always appear more than simple interest since it factors in interest on previous interest, not on the principal amount alone.

Also read: The trick to save extra 20 dollars every week

APR

Lenders tend to use APR to advertise, say a mortgage loan or a credit card. This is because here the interest is a penalty on the customer, not reward. Here, since simple interest goes into calculating APR, the figure arrived at appears less harsh to the customer, a borrower.

The only difference hence is how the interest goes into arriving at the figure – in APY, it is compounded, and in APR, it's simple.

Always seek more info on APR and APY

More than industry players, who are specialists in finance, it is the customer that needs to distinguish between APR and APY before arriving at any conclusion. For example, one investment product can appear better than the other just because the former is quoting APY and the latter APR. The customer can seek the service provider’s support to know the exact figures as it may be complex to compute by oneself.

Is the stock market worth investing?

As stated earlier, money should make more money. But is investing in stocks a good idea?

Yes, there is no certainty that the stock/s you pick will appreciate in the future. But at the same time, we cannot ignore ace investors including Warren Buffet who made fortune by investing in stocks. In a recent speech, Buffett said that he has instructed his estate manager to invest his money in S&P 500 index after his death. That’s a huge statement.

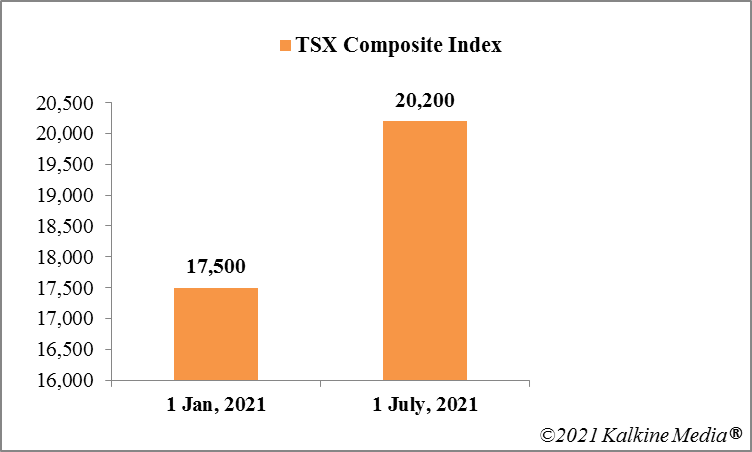

Even at a time when the economy is not doing that well, the benchmark index of Canada, TSX Composite Index, has returned in double-digits in 2021. These returns outshine those of conventional investment options like retirement plans or certificates of deposit.

Also read: How to invest in cryptocurrencies?

The index peaked to 20,000 in June 2021, at a time when the Canadian economy had yet to achieve pre-pandemic levels with respect to employment and GDP growth rate.

Bottom line

Investing or taking out a loan is not bad, but taking any uninformed decision can be expensive. That’s why one must know whether the fund manager or the lender is quoting APY or APR. The difference is explained above, and it is just the compound interest in APY that makes the big difference. Once we know the right calculation, investing in stocks or any investment option becomes a lot easier and rewarding.