_07_03_2026_03_50_21_133108.jpg)

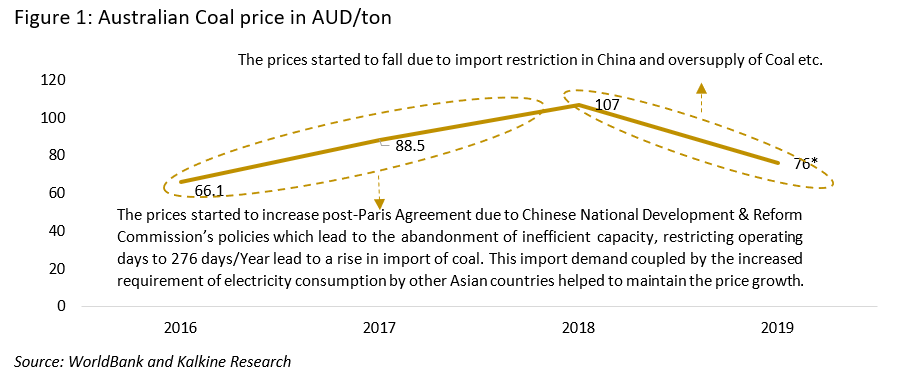

Come 2019, Australian Coal price started to tumble once again after peaking up in 2018 courtesy to low demand from China and oversupply of commodity due to the move toward a reduction in CO2 emission. As of November 2019, coal price plummeted by 37.38% from 2018 average price of AUD 107/ton, as shown in figure 1.

The Chinese import restriction has put the cap on seaborne coal due to which buyers are cancelling the deals or seeking to defer the delivery time to January next year. This has led to the loss of ~AUD 2.56- 2.92/ton to International traders. The demand of coking coal too expected to plunge in China due to shift toward electric arc furnace using scrap iron. However, this impact on coking coal is expected to get compensated by the increased import of the remaining Asian countries such as India, Brazil, South Korea, Japan and Turkey due to the Steel demand.

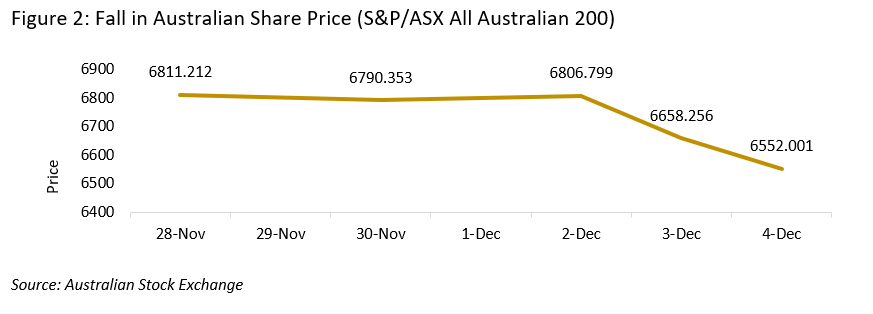

The market was still dealing with the hurdles then the blow came from United States (US) restoring tariff import on steel and aluminum from Brazil and Argentina citing devaluation of US currencies. This led to the biggest fall in Australian share for being part of US section 232 imposes quotas on steel product export to the US.

The Coal price is expected to remain constant in short term while appear to increase in future due to the strong demand from Asian countries electricity consumption and rise in Electric Vehicle (EV) fleet etc. Similarly, the same trend is observed in Coal producing companies in Australia, such as Whitehaven, New Hope, Yancoal.

- Whitehaven (ASX:WHC): Share price hit low at AUD 2.630 on 6th December from AUD 3.17 traded on 2nd December 2019. The stock traded volume increased from 2,142,048 to 11,431,650 during the same period which signifies the wave in the sentiments of people. The company had increased dividend distribution in FY19 by 42% i.e. AUD 464.854 Million from FY18 and improved group gearing ratio of 8% in FY19 from 12% the previous year. Also, EBITDA margin on produced coal improved from preceding year i.e. AUD 63/t to AUD66/t in FY19 due to the improved realized price of coal and high calorific value.

The price of the share is further affected by the recent announcement of concerning to cut in FY20 guidance due to the shortage of skilled operator in Maules Creek mine and impact of draught creating more smoke interrupting the production schedule. The production cut is in the range of 12% for Maules Creek and 6% for Narrabri Mine.

The revenue generated from shipping is mainly coming from Japan followed by Taiwan, South Korea, India and China. China will not have much impact on the company since it accounts for only 2.7% of total revenue generation of AUD 24.77 Billion. Which seems to be easily getting compensated by the increased demand from other Asian countries.

- New Hope (ASX:NHC): Following the same trend price of share trembled to AUD 2.00 on 6th December from AUD 2.17 traded on 2nd December 2019. In this case dividend distribution increased by 33% in FY19 i.e. AUD 133 million in FY19 distribution of AUD 99.738 million in FY18 which makes 13% surge in the dividend paid per share in FY19 at 9 cents/share. Also, EBITDA margin from continuing operations decreased from preceding year i.e. ~43% to ~39.57% in FY19 due to the high operational expenses as well as sales cost in comparison to previous years. Though EBITDA from continuing operations increased by 11% to AUD 517.061 Million in FY19.

Here, revenue generated from shipping is mainly coming from Japan followed by China, Taiwan, Chile and Korea/Indonesia. China will have very less impact on revenues generation as it accounts for 9% whereas remaining five countries alone contributes 76.35%.

- Yancoal (ASX:YAL): Here unlike S&P/ASX All Australian 200 Index trend, share price moved in roller-coaster fashion. The share price decreased from AUD 2.94 on 2nd December 2019 to AUD 2.93 on 6th December 2019. Not much impact is seen in the traded price of stock courtesy to Yanzhou, a Chinese company being major shareholder of Yancoal. In this case dividend payment in FY18 was around AUD 507 Million having a payout ratio of 60% and in FY17&16 no dividend payment was made. Gearing ratio has improved significantly from 47% in FY17 to 35% FY18. Also, operating EBITDA margin increased from 36% in FY17 to 45% FY18

There is no change in production guidance of FY19 reaching ~35Mt up by 6.38%. Most of the volume is expected to come from Mount Thorley Warkworth, Moolarben, Tier 1 Asserts, and Hunter Valley Operations. Also, ~1% of a slight improvement in operating cash cost is noticed in FY19 at 62.5 AUD/t FOB.

Here, revenue generated from shipping mainly coming from Japan followed by Singapore, China, South Korea and Taiwan. Companyâs 25% revenues came from China in FY17 which has been reduced to 16% in FY18. Export in future is expected to come from Japan, Singapore, Taiwan and Thailand.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.