Definition

Related Definitions

Variable Life Insurance

Variable Life Insurance

What is variable life insurance?

Variable life insurance is a type of life insurance that incorporates investing and life insurance elements.

This is a permanent life insurance policy with distinct accounts, including investment funds and instruments, like equity funds, stocks, bond funds, bonds, and money market funds. Investment opportunities and policy loans are unique aspects of variable life insurance policies.

Summary

- Variable life insurance is a type of life insurance that combines the concepts of investing and life insurance.

- Because of the investment risks, variable policies are classified as securities contracts.

- Variable life insurance is sometimes more pricey than other types of life insurance, such as term life.

Frequently Asked Questions (FAQs)

How does a variable life insurance policy function?

Variable life insurance not only contains investing and life insurance components, but it may also be used in a variety of ways.

Variable life insurance is sometimes referred to as a type of security. Due to the investment risks, variable policies are deemed as securities contracts. Accordingly, they are regulated by federal securities laws, and sales professionals are expected to offer a prospectus of available investment products to prospective customers under federal regulations.

Here's how to understand variable life insurance coverage in the simplest way possible. It is an agreement between a customer and an insurance company. It's designed to fulfil specific tax planning, investment, and insurance purposes.

Variable life insurance is a form of coverage that pays a set sum to the customer's family or other beneficiaries in the event of death. The financial worth of this type of policy is determined by the number of premiums clients pay, the policy's expenses and fees, and the performance of the policy's investment alternatives, which are typically mutual funds.

Source: © Dizain777 | Megapixl.com

Furthermore, if a person chooses to use a variable life insurance policy, they will enjoy tax benefits, like tax-deferred earnings accumulation.

The investment opportunities offered on the policy and the favourable tax treatment of the policy's cash value growth make variable life insurance appealing. Moreover, policyholders can access their policy's cash value through a tax-free loan as long as the policy is in place. Unpaid loans containing interest and principal may, nevertheless, limit the death benefit.

Moreover, profits or interest incorporated in full and partial insurance surrenders is taxable at the moment of distribution.

Like mutual funds and other types of investments, a variable life insurance policy should be accompanied by a prospectus that details all policy charges, sub-account expenses, and fees.

New York Life and Prudential are two of the most significant firms globally when it comes to providing variable life insurance products.

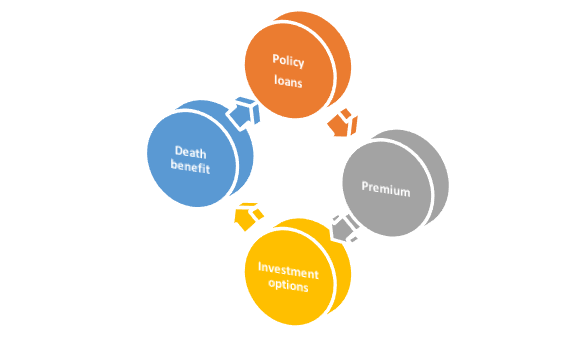

To summarise, the functioning of a variable life insurance policy is dependent on four factors.

Policy loans

The advantage is that holders are not obligated to pay federal taxes on loan withdrawals and do not have to pay surrender fees. However, as a disadvantage, the policy's effective cash value will be lowered, reducing the death benefit payable to the holder's beneficiaries.

Premium

Under a variable life insurance policy, the recipients should pay premiums in an account. This payment includes a fee for advising services, which lowers the effective premium deposited into the account. Individuals can then put their premium into one or more investment alternatives, which are usually mutual funds.

Source: Copyright © 2021 Kalkine Media

Investment options

A fixed account and a cash value account are included in the policy. The cash value account allows for investments in various sub-accounts, with a maximum of 50 sub-accounts per policy.

Death benefit

The monetary sum collected by the declared beneficiaries and dependents in the policyholder's death is known as a death benefit.

Variable life insurance pays out a death benefit that includes the face amount plus either the policy's net contribution in the form of premium payments or the account's existing cash value.

Who requires variable life insurance?

Because of its high cost, variable life insurance is not an investment opportunity or suitable life insurance for many people.

A traditional term life insurance policy would be beneficial if a person only desires to assure a death benefit payout for family members because it gives more coverage for a lower price.

In the meantime, individuals will benefit more from traditional investing. The cash value of a variable life insurance policy, on the other hand, can only be effective for people who have exhausted all other investing options.

What are the benefits of a variable life insurance policy?

- It shields family members against debts like student loans and mortgages in the case of premature death.

- It provides recipients with a tax-free inheritance, which is helpful for high-net-worth individuals whose inheritance would otherwise be subject to estate tax.

- It pays final expenses such as funerals and other end-of-life expenses.

- It generates long-term savings with the option to invest in funds supplied by insurers.

Source: © Orson | Megapixl.com

What are some of the drawbacks of variable life insurance?

- It is not a suitable short savings option as it is meant to fulfil long-term financial goals or offer a death benefit.

- It is necessary to keep enough cash in the account to pay policy premiums, and if this is not done, the recipient will not be entitled to any death benefits.

- The overall policy costs and fees add up to significant liability. The costs of owning a policy usually include several fees deducted from premium payments and surrender charges.

- It is substantially pricier than term life insurance for a comparable level of protection for recipients, and the cash value investing options are restricted.

- It comes with the risk of losing initial premium payments, which is compounded by the risks involved with investing decisions.

- Another inherent risk is the bankruptcy of the insurance business itself. Recipients get guarantees, including death benefits, based on the issuing firm's financial strength, but the firm may be unable to fulfil its obligations in the event of financial hardship.