Summary

- Since March, RBA has developed various coping strategies for different stages of the recovery process.

- Monetary policy measures have continuously been altered to suit the targeted areas better.

- Along with the 3-year bond targets, the monetary policy committee also decided to introduce a quantity bond purchase program in November.

- Future expectations of monetary policy changes brought about remarkablerecoveries earlier than expected.

The Australian economy is surfacing from the worst recession ever recorded since the 1930s. This recovery has been made possible through stringent monetary policy action by the RBA. The immediate decisions taken by the monetary policy committee have helped shape this recovery.

The current unprecedented times have left behind a huge impact not only on the economy but also on how the economic recovery should pan out for various economies. Many new initiatives by the RBA and the Australian government have been progressive decisions for the Australian economy.

Pandemic related recovery has highlighted the importance of taking quick action and adopting targeted policies.

ALSO READ: Economic Charter: Australia's Current Account and House Approvals Data Out

Policy Measures Adopted in Times Of Distress

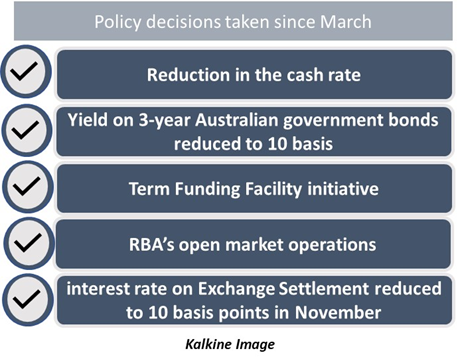

RBA’s first step in its plan of action was to reduce the cash rate. This was accompanied by measures like the introduction of a target on the yield on 3-year Australian government bonds of around 10 basis points, a Term Funding Facility initiative, RBA’s open market operations to inject liquidity into the markets, and further strengthening measures by the RBA.

These changes happened gradually, the beginning of which started in March this year. The interest rate on Exchange Settlement was reduced from 25 basis points to 10 basis points in November, and the RBA set a target of buying $100 billion worth of government bonds over 6 months as well as $5 billion worth of Australian securities.

Source: ShutterStock

Effectiveness of Policy Measures Adopted

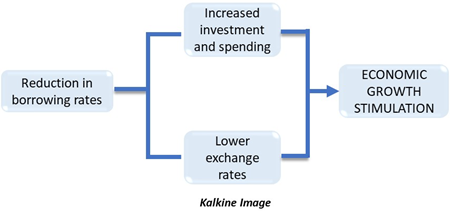

Reducing the borrowing rates stimulates spending in the economy as it becomes cheaper to borrow now than in the future. Low borrowing costs would enhance borrowing in the economy and would give rise to investment and spending. The liquidity in the market was also enhanced by RBA’s open market operations.

Lower interest rates are also expected to keep the exchange rates subdued. When the RBA buys bonds, it increases the Exchange Settlement balances as the bank credits the counterparty.

The 3-year government bonds influence many borrowing rates across the county. In other countries, the yield on 10-year government bonds is considered more important, for instance, in US longer term bonds are used as a benchmark. However, in Australia, the 3-year bonds are considered as a more important benchmark, against which other rates are measured. The timeline of three years represents the estimated time it would take for the cash rate to bounce back.

The benefits of these policy measures have seeped into households as well. The mortgage rates have been on a decline since March. This has further led to more disposable cash being made available in the portfolio of mortgage holders.

Early superannuation withdrawals were offered to individuals who have also revived demand in the economy. Various other policy measures aimed at job creation like JobSeeker and JobKeeper have provided a boost to employment.

Employment generation has helped increase household savings apart from creating demand. These savings would ensure future cash stimulus is maintained.

RELATED READ: Main economic boost from vaccines to follow later: BoE

Bond Purchases by the RBA

The RBA has focused bond purchases on maintaining 3 main criteria, these are:

- Maintaining the 3-year target

- Addressing market function

- Purchasing bonds worth $100 billion after November

Adding to the 3-year bond targets, the monetary policy committee also decided to introduce a quantity bond purchase program in November. The yield on longer term bonds was observed to be higher than in other countries. Therefore, it was concluded that the government bond purchases were affecting the yields of longer-term bonds more than they affected the targeted 3-year bonds.

The 3-year period is the preferable period, as the economy is expected to take 3 years’ time to show strength. Thus, even though long-term bonds are showing greater yields, the RBA continues to focus on 3-year bonds. Another reason that long term bonds are not targeted is that over a longer period, various other factors also start affecting the yield of the bonds. Many global factors affect the returns on these bonds. Therefore, the RBA should focus on the 3-year bonds only.

ALSO READ: RBA Monetary Policy Decision: No Changes to Policy Setup

Source: ShutterStock

Changes in Expectations Post Announcement

The cash rate cut to a near zero level did not come as a surprise. The reduction of cash rate to 10 basis points on the November 3rd monetary policy meeting was a move that had been long due. These expectations started to appear in September itself, thus, changes were observed early on, even before the announcement was made.

The quantity targets for bond purchases was also an expected move. Thus, the yields started to decline at the front end of the cycle. This decline was observed in the yields of both longer-term bonds as well as 3-year bonds. However, the decline for the former was greater than the decrease in the latter.

The policy changes had subsequent impacts on the exchange rate as well. The exchange rate in trade-weighted terms depreciated by 5%, against the USD between mid-September and November. This came even before the November package was announced, thus, a majority of this seems to have resulted out of expectations being developed early on.

The Monetary Policy Path

RBA has developed stringent policy action and a diverse set of targeted policies for various stages of recovery since March 2020. The reduction of borrowing rates has been the centric point of these policies. This decision has also led to lowering of exchange rates and depreciation of the Australian Dollar.

The impact of lower interest rates has more than offset the impact of lower deposit rates that have been passed onto the consumers by the commercial banks.

The monetary and fiscal policy, coupled with various employment generation initiatives, would move the economy for now. The news of the possibility of a vaccine in the future would also stir economic growth. Regardless of these developments, monetary policy continues to remain at the heart of the Australian recovery.