.jpg)

Summary

- Governor Phillip Lowe hinted at the possibility of lower interest rates in a recent speech.

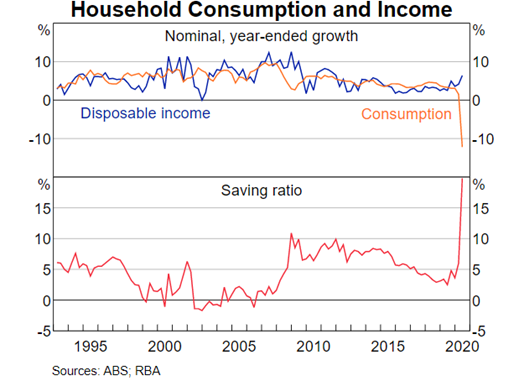

- Consumption levels have not received the boost that was expected from the current policy aids.

- In order to stock up on their deposits, consumers have continued to save even after the provision of fiscal aids.

- The upward revision of cash rates is unlikely until inflation reaches 2-3%.

- Recovery has been uneven across regions and through different phases of time.

- The decision to move the interest rates down to 0.1% requires heavy deliberation before it is implemented.

RBA Governor Phillip Lowe hinted at the possibility of future rate cuts in his latest speech at Citi’s 12th Annual Australia and New Zealand Investment Conference in Sydney. Governor Lowe said that further aid is needed in order to promote more spending.

As consumption levels have not received the expected boost from the existing policies, further course of action may be required. This is where the possibility of interest rate cut to 0.1% comes to the light.

Governor Lowe stated that the Open Market operations and the Term Funding Facility have both been of great help in supplying credit to households and businesses. This supply of credit is important in the recovery phase.

In his speech, Mr Lowe added that there is no possibility of cash rates bouncing back any time soon. Stringent monetary policy decisions favouring investment and consumption have been adopted by the RBA in the recent past. However, over time the policy response has been shifted towards the fiscal side.

The Need for Lower Rates

The efforts to increase consumption levels have resulted in counter-intuitive results. A pattern of further increase in savings has been observed. The economic crisis caused by the pandemic has seen people saving more and more in order to protect themselves from any future uncertainties.

With no concrete timeline till complete recovery from the pandemic, many people continue to remain cautious. In order to stock up on their deposits, consumers continue to save even after the provision of fiscal aids.

Falling interest rates also come with a possibility of increased savings, as people expect lesser returns on their bank deposits. Their current consumption patterns are evolved out of their expectations about the future as well.

As people expect the situation to get better, their spending patterns are bound to improve. However, without a proper recovery path and no solid timeline currently, most people would be wary of the unpredictable circumstances and thus would save more.

In the light of these circumstances, it is possible that interest rates will be tipping down in the near future. However, they may not become negative as Mr Lowe has expressed his dissent with regards to a negative interest rate set-up in the economy.

There still remains a lot to be discussed on the table before rates are pulled down to 0.1%.

ALSO READ: How is the negative interest rate prospect panning out for Australia?

Current Recovery Measures

According to Mr Lowe, the income support offered by the RBA through policies like Term Funding Facility and JobSeeker payments have helped households through this tough phase. However, with interest rates at a record low level of 0.25%, consumption levels have still not seen the recovery that was expected.

Australia has seen low budget deficits and low levels of public debt, thus making the current situation an unprecedented case. Mr. Lowe suggests that the deficits are at a manageable level and can be financed once the economy stabilises and consumer spending grows.

Partial and Uneven Recovery

A striking feature of the current economic situation is the unevenness in recovery. All COVID-related constraints as well as relief measures have been implemented with equal intensity and frequency throughout Australia. However, recovery has been uneven across regions and through different phases of time.

The inconsistency in recovery has been observed across age groups, industry, firm size and regions.

It was also observed that during the initial phase of the lockdown, consumer spending initially recorded a boost when people invested their money in electronics and exercise equipment. However, these were not enough to increase spending overall.

The second phase in Victoria has also contributed to these irregularities as the earlier recovery was subdued due to re-imposed restrictions.

Unemployment and Savings

Another important aspect touched by Mr Lowe in his speech is the probable increase in unemployment in December. Unemployment rates are at an all-time high in Australia currently and this figure is expected to increase by December 2020.

As unemployment increases, all measures adopted as a remedy to contracted consumption, might go in vain as people would again start to save. Thus, policy measures have to be adopted in a way so as to combat this future expectation of consumption contracting further.

The pandemic has made people more risk averse. Their appetite for handling tumultuous times has decreased due to a long period of uncertainty. Thus, most people would not want to be at the riskier side of things and would save more to protect themselves from any impending economic downturn.

Future Policy Prospects

The next monetary policy meet is scheduled to be in November where further policy aids would be discussed. Mr. Lowe said that “monetary policy easing” would be on RBA’s agenda for now.

In his speech, Governor Lowe stressed on creating positive expectation of the future path of the pandemic. As the spread of the virus comes under control, job market is expected to strengthen, and salary cuts may diminish. Consequently, people would get more secure and would save less.

The anticipation of a future income stream allows consumers to have a relatively loose hand on their spending habits. Thus, the prospect of a vaccine may encourage more spending for now.

Cash rates are not expected to rise till the inflation rate is brought down between the target range of 2-3%. RBA understands that current policy measure might affect the long-term financial stability. But for now, the focus is on private sector job creation as well as easing loan payments.

It is still unclear how much of a boost any more monetary policy actions might bring about. The effectiveness of a policy might be hampered by the long-term risks associated with it, which may start to reflect in some time.

Thus, there are a lot of considerations before a new monetary policy is rolled out. The real course of action would only become clear once the RBA holds the next policy meet.