Summary

- Retail, labour and property markets have noted significant improvements over October.

- Government and central bank’s encouraging economic policies, along with other factors, are driving a recovery in the Australian economy.

- While ease of restrictions is improving business conditions and consumer confidence levels, the risk of a surge in COVID-19 infections still persists.

With COVID-19 pandemic under control, the Australian economy is actively proceeding on the path of economic recovery. While the economy is not out of the woods yet, several green shoots are sprouting in the nation’s economy, stimulating hopes of a sooner return to the pre-pandemic state.

Australia’s consumer sentiment levels recently climbed to seven-year high during the first week of November, with Aussies looking forward to a normal Christmas. Westpac-Melbourne Institute index of consumer sentiment rose by 2.5 per cent during the period, following a surge of 11.9 per cent in October.

Amidst a boost in consumer confidence levels, a significant improvement has been noted in the performance of different sectors across the economy, including labour, retail and property. Let us quickly shed some light on bright spots dazzling in each of these sectors below:

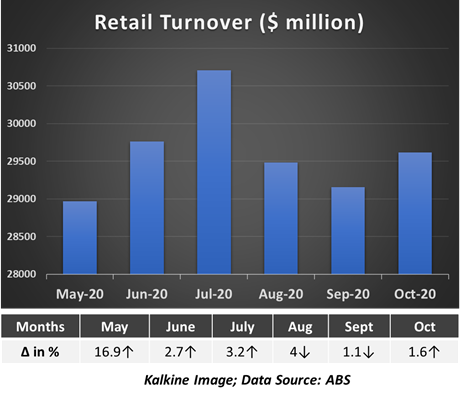

Retail Sector Growth

The latest preliminary estimates from the Australian Bureau of Statistics (ABS) suggest that the retail sector recorded strong growth in October 2020 amidst ease of COVID-19 restrictions. The seasonally adjusted retail turnover rose by 1.6 % from September to October 2020, beating estimates of a 0.3% rise. An improvement in consumer spending and consumer confidence levels seem to have stimulated this recovery in retail sales.

Below chart demonstrates a change in the level of retail turnover over the last six months:

In October 2020, Victoria led the retail growth in all industries except food retailing by recording a growth of 5.2%. Most of the improvement in the retail sector came amidst increased demand for food from cafes and restaurants. As lockdown restrictions eased and shops reopened, higher demand for takeaway food coupled with dining services led to retail sector expansion.

Related Read: Victoria Emerges as the Warrior Against Corona War

Household goods retailing remained unaltered, maintaining recent strength. However, there was an increase in the demand for other retail goods like clothing, footwear, and personal accessories. These improvements came after reopening of businesses, with consumers becoming less apprehensive about their spending habits.

It is worth understanding a chunk of the population was going through job losses during the initial stages of lockdown restrictions. Thus, it made sense for them to curb their retail spending. However, liquidity inflow has led to improved expectations, and thus, expenditure has increased.

Labour Force Participation

According to the ABS estimates, Australia’s employment and monthly hours worked in all jobs increased by 1.4% and 1.2%, respectively from September to October 2020. The rise in employment was only 1.7% below March, signifying that a large chunk of people outside of labour force is now back into employment.

During the period, Victoria recorded a strong increase in the number of hours worked, which surged by 5.6%. Besides, the state’s employment also rose by 2.5% to 81,600 people.

However, seasonally adjusted unemployment also grew in October 2020, with the participation rate surging by 0.9%. Importantly, a strong uptick in the participation rate led to the jobless rate rising by only 0.1%. Below chart demonstrates a change in the level of Australia’s unemployment rate over the last six months:

It is imperative to note that a larger number of people are now actively looking for jobs and are available to work. This appears to be a much-needed shove for businesses and corporates as the continuing recovery might mark the beginning of their overall revival from virus crisis.

ALSO READ: How COVID-19 has Impacted Australian Labour & Property Markets?

Property Sector Upturn

Housing demand is expected to improve as people regain jobs. Low interest rate environment is also anticipated to drive the process of demand creation in the property market, besides fostering consumer confidence, business confidence and stock market rally.

Prices have varied across Australian cities since the pandemic struck. Regional cities recorded an increased demand due to people shifting away from capital cities. However, this demand was unmet with an insufficient supply of property. Consequently, prices surged in regional areas, while they remained subdued in other business hubs.

A prime example of such a contrast was NSW region, which recorded an increased demand in the regional areas but saw a lack of supply in the capital Sydney. The far west side of NSW recorded housing prices going as low as $150.

However, this is expected to change given the progress in the employment forecasts. GDP is also expected to grow sharply in 2021 while it may take a few years’ time before returning to pre-pandemic levels.

It is imperative to note that the Australian property market returned to positive growth in October following five months of consistent fall in house prices. CoreLogic’s recent estimates suggest that residential property values improved by 0.4% in October, with every capital city except Melbourne recording a rise. During October, dwelling values improved by over 1% in all four smallest capital cities, with Hobart, Brisbane, Canberra and Adelaide noting record-high housing values.

Moreover, one cannot neglect an ongoing recovery in Australia’s dwelling approval levels, which seem to be bolstering house price surge across the nation. The chart below shows the performance of dwelling approvals since May 2020:

Housing prices are set to show an increase as the property market sets on a recovery trail. With employment levels increasing along with an uptick in consumer confidence and business sentiment, the housing market is projected to see an increased demand in the near future.

Factors Behind the Revival

The changes in unemployment and retail have been the strongest for the month of October 2020. This is clearly a positive sign for the economy and has improved forecasts for future periods as well.

Undeniably, the favourable policies implemented by the government and the RBA have helped the economy pick up speed. Besides, banks have also enabled borrowers to invest in real estate and other assets by allowing deferment in loan payments and announcing other relaxations. It is hard to overlook separate stimulus packages introduced by state governments that have further given a leg up to economic recovery.

On top of these factors, an increase in consumer spending, as recorded by major banks via credit card spending and consumer activity, has also lent a helping hand to this revival.

For now, these factors have given the kickstart needed by the economy to recover. However, it is important to note that as restrictions are eased, there is a risk of infections soaring across Australia. This might affect how economic recovery takes shape.

One cannot neglect that majority of areas across the globe are recording a second wave of the virus. Therefore, easing of restrictions comes with a huge responsibility on the shoulders of the government as well as the people. The effectiveness of the job creation efforts taken by the government might subside if the cases rise, and people may be compelled to stay indoors once again.

The current advantage to the government is the previous experience of dealing with the pandemic. With this knowledge, the government can reshape its policies, focusing on areas that can add more value to the economic recovery. While improvement is evident, it may take some more time before the economy is entirely recouped.