Summary

- The global LNG trades are moving at rabbit’s pace, with total trades reaching 348 million tonnes in 2019, leading to a supply rush, which is now dependable on China and Taiwan imports and energy policies.

- Both China and Taiwan are poised to lead the LNG growth curve while incorporating more LNG tranche into the total energy mix.

- Also, the global LNG trades have witnessed a plunge in the beginning of the year, in the wake of falling industrial energy demand, it is anticipated to improve over the long run.

- Demand of LNG to surge in China and Taiwan while remaining flat across Europe, despite high energy demand, over limited storage capacity.

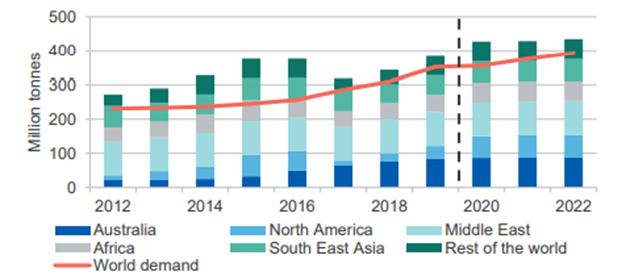

LNG trade across the globe has grown rapidly over the last few years, totalling around 348 million tonnes in 2019, presenting an increase of 12 per cent or 38 million tonnes against the previous year.

The surge in LNG trade has prompted a surge in the supply chain, with global LNG supply capacity growing by ~40 million tonnes per annum in 2019, outpacing demand and leading to a supply glut. The present supply glut, along with low oil-linked reference prices, is now posing a multitude of challenges for the oil & gas sector.

Additionally, while the supply chain has been growing rapidly with the domestic market supplying 77 million tonnes of LNG in 2019, surpassing Qatar, and the United States domestic LNG production booming, the demand has remained relatively stagnant.

However, the global LNG demand is now estimated by industry experts to pick some pace ahead with China and Taiwan, leading the growth curve front.

Demand and Supply Forecast (Source: DIIS)

To Know More, Do Read: Australia To Jostle Qatar for the LNG Crown; How Long Would the Reign Last?

Just like gold and iron ore, the rein of LNG is falling in the hands of China, which yet remains the second-largest consumer of the global supply chain.

Also Read: China- The Catalyst to Gold and Iron Ore Rally

China- A Prominent Catalyst for LNG Demand Growth

During the onset of the year 2020, COVID-19 outbreak took a toll on LNG demand in China, with LNG largely concentrated in February and March 2020, falling by an estimated 7.1 per cent against the previous corresponding period (pcp).

- However, LNG imports rebounded during April and May, with an ease in travel restrictions, and a slight recovery in the Chinese economy, continuing on red dragons’ commitment to purchase USD 52 billion of energy products from the United States in 2020 and 2021, under the umbrella of Phase One trade deal.

- Despite several cancelled contracts witnessed since the beginning of the year, the Department of Industry, Science, Energy and Resources (DIIS) anticipates that Chinese LNG imports would climb to 68 million tonnes in 2020 to represent an increase of 12 against the previous year.

- Furthermore, as China is ahead of the recovery curve, with an early lockdown and an early unlock, it presents opportunities to LNG exporters to absorb some excess supply in 2020.

Ahead of 2020, LNG demand in China would be primarily driven by the industrial sector, and a policy-driven expansion of gas-fired power generation to address climate change and remain committed to the Accord de Paris.

Moreover, many industry experts estimate that China would be the key source of global LNG demand growth, with the LNG imports of 83 million tonnes by 2022, making the red dragons the largest importer of the global supply chain, mainly from the United States and Australia.

Risk Factors

China is estimated to become the largest LNG importer over the long run; however, the estimation of industry experts is not without risk.

- The impact of slowing global economic growth on China’s export-oriented sectors, and the risk of further COVID-19 containment measures presents a downside risk.

- Additionally, the global LNG exports to China could face severe competition from domestic gas and pipeline imports, with the commencing of the Power of Siberia pipeline in December 2019, which would ramp-up over the next five years.

- Also, the LNG demand in China is sensitive to future energy and environmental policies, which are subject to considerable uncertainty as government priorities alter because of the effects of COVID-19.

The Global Demand Scenario

On the global counter, Japan demonstrated a minimal impact of the COVID-19 outbreak on the LNG demand during the first quarter, with imports surging by 15 per cent in March 2020 against pcp.

- However, several buyers sought deferrals of cargoes for April-June 2020 delivery in anticipation of weaker demand, which coupled with a state of emergency from 7 April 2020 to 25 May 2020, took a toll on the LNG demand in the wake of declining power consumption.

- The LNG imports of Japan declined by 5.4 per cent in April, whilst declining 25 per cent in May 2020 against pcp.

- Whilst a fall in demand during the second quarter was evident; many industry experts believe that the overall LNG demand in 2020 across Japan would only decline marginally by 3 per cent to stand at 74 million tonnes.

- However, beyond 2020, the resurfacing nuclear power would keep the LNG demand stagnant and near 74 to 75 million tonnes.

Taiwan has emerged as one of the top performers in terms of managing the COVID-19 outbreak, with early containment of the infection and no lockdown, keeping the energy demand robust. Also, LNG demand captures a significant chunk in Taiwan’s energy mix.

- However, despite a robust energy demand, the LNG imports have declined 2.0 per cent during the first five months of the year against pcp but are estimated to surge over the next two and a half years.

- Taiwan energy plans envisage the share of gas in the total energy mix from 34 per cent to 50.0 per cent by 2025.

Furthermore, LNG demand across South Korea, and India took a toll due to extended lockdowns and reduced energy demand.

- Europe, which imported a record 87 million tonnes of LNG in 2019, set to witness an increase of 71 per cent against the previous year, is another emerging catalyst to the global LNG demand with strong imports growth.

- In early 2020, LNG imports increased by 37 per cent year-on-year in the first five months of the year; however, limited storage capacity across Europe is anticipated to keep the LNG demand stagnant ahead.