Summary

- Gold and iron ore are taking the stage as stars of the commodity world with both posting strong gains in the wake of gush in prices, leading them to test multi-period highs.

- While gold is trading near its seven-year high, iron ore is continuously inking new 52-week highs.

- But what’s next for them, where the demand is coming from, which factors are driving their prices, and were these commodities could head ahead.

- The answer to every question is leading back to China, where the COVID-19 first emerged.

Gold and iron ore have been the best-performing commodities so far with prices of gold spot trading near its seven-year high at USD 1,818.13 per ounce and prices of Iron Ore Futures on the Dalian Commodity Exchange (or DCE) trading near its new 52-week high of RMB 845.00 per dry metric tonne.

The surge in both commodities has provided an impetus to ASX-listed gold and ASX-listed iron ore stocks, which are now emerging as the top performers in the metal and mining space.

To Know More, Do Read: Commodity Stocks Making Their Way To The Top

Amidst the market turmoil, the gold market has witnessed a lot of cash inflow through gold-backed ETFs and aggressive purchasing of many central banks across the globe, to hedge their position against the market beta and dollar rush, respectively.

To Know More, Do Read: Gold Vaults to Highest Levels Since October 2012; Trade Trends and Data Divergence

- On the other counter, iron ore prices have been gushing over the supply shortage which emerged due to operational challenges faced by Australian and Brazilian iron ore miners in the face of Tropical Cyclone Damien and heavy rainfalls, respectively.

- Apart from that, operational challenges faced by some miners across the globe concerning the workforce over travel and free movement restrictions imposed by several countries to contain the spread of COVID-19 also contributed to the supply squeeze.

To Know More, Do Read: Iron Ore- The Rally From 15-Week High to a 52-Week High

One thing which is now common behind the rush in prices of both commodities is the demand from China.

While gold had witnessed a rally over the market fear, until now, many industry experts now believe that the further rally would gather steam from the retail sector, especially from China, thanks to its early lockdown and an early lifting of lockdown.

- Retail demand for gold has taken a considerable hit in the recent past over the shifting consumption pattern around the globe with many deferring consumption and parking most of the saving into the financial market.

- The evidence of which could be gathered from the reports generated by various exchanges across the globe over recent trading activities.

- Even across the continent, trading activities have witnessed a boom with many new trading accounts now entering trades in the financial market, leading to a surge in volumes.

To Know More, Do Read: Australia is Day Trading and How! Market Activity Jumps Multifold: Time to Grease your wheels

Furthermore, the surge in gold prices has taken a toll on the retail demand as well, which, however, now seems to be a new normal, and many large investment banks such as Goldman Sachs anticipates that gold prices could average as high as USD 2,000 per ounce by next year, and the retail demand from China and India could act as a major factor to aid price surge.

- As per the data from the World Gold Council (or WGC), the retail demand for gold, i.e., the jewellery demand fell by 39 per cent against the previous corresponding period (or pcp) during the first quarter of the year 2020 to stand at 325.8 tonnes, representing a record low in the data series of WGC.

- Furthermore, China, which is the largest retail market, was the hardest hit with a decline of 65 per cent in jewellery demand at just 64.0 tonnes during the same period.

However, the retail demand is now expected by various investment banks to surge in China, which could further boost the gold rally over the coming years.

Likewise, iron ore prices are now depending upon the demand from China.

China is charging its steel output- first to capture a large tranche of the global steel industry, and secondly to provide an impetus to its post-COVID-19 economy.

To Know More, Do Read: China Poised to Grab the Global Steel Trade as Economies Open up for Trade

Economic activities across China has now taken a leap with industrial production, manufacturing activities, non-manufacturing activities, and especially construction activities gaining momentum, leading to high demand for steel domestically.

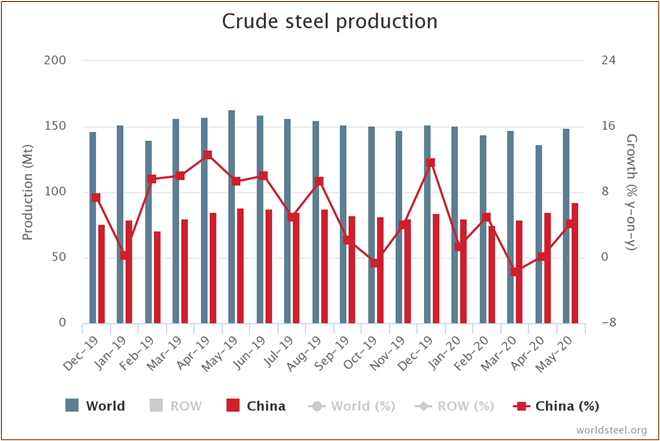

- China alone produced over 62.0 per cent of the global steel production of 148.8 million tonnes in May 2020 at 92.3 million tonnes, which also remained 4.2 per cent up against pcp and ~ 8.58 per cent up against the previous month.

- After witnessing a slight fall in steel production during the first quarter of the year 2020, the steel output is now running at a rabbit-pace with three months of a consecutive surge.

Source: World Steel Association

The higher steel production in China is now calling for iron ore; thus, despite witnessing a slight recovery in the supply chain, the commodity is gushing forward on the international front.

Furthermore, the World Steel Association anticipates that the steel demand across China would be more visible in the second half of 2020, driven by construction, especially infrastructure investment, as the government has put forward several new infrastructure initiatives, which could further support the demand for iron ore.

In a nutshell, both the top-performing commodities on the international front are somehow tracing back to China, and the revival of the nation could further propel these commodities. However, it is not without risk as the red dragons are currently dealing with the issue of the second wave of COVID-19 infection, leading to the slowing down of daily activities across many provinces, which if fuelled further, could put a lid on gains of both the commodities.