Highlights

- Batteries are predicted to account for 22% of the total nickel demand by 2027.

- The world demand for lithium is estimated to be 724,000 tonnes of Lithium Carbon Equivalent in 2022.

- Nickel Industries Ltd. (ASX:NIC) reported grades of 6.36% nickel in Hengjaya mine project infill drill assay results.

- Rio Tinto shares outperformed ASX 200 by over 3% in September 2022 following production of spodumene concentrate in Rio Tinto Iron and Titanium project.

Battery plays a very important role in key applications like consumer electronics, electric vehicles (EVs) and off-grid battery storage. Battery metals are those metals which can be used to manufacture rechargeable batteries (secondary batteries). These include lithium, nickel, cobalt, manganese, aluminum, tin, etc. Out of these, lithium and nickel are of particular significance, while cobalt is obtained as a by-product from copper and nickel mining.

Performance of nickel and lithium in first quarter of 2022

Nickel

The global demand for nickel rebounded in 2021 as the impact of the COVID-19 pandemic died down and the world economy recovered. The main use of nickel is in the production of stainless steel, followed by the production of alloys, plating, casting and rechargeable batteries. The total demand for nickel was forecasted to reach 2.9 million tonnes in 2022 and almost 3.1 million tonnes in 2023.

The demand for EVS was very high in 2021 and is expected to continue this trend. There will be a growing need for bigger battery packs, which will be a major driving force of the nickel demand. Batteries are predicted to account for 22% of the total nickel demand by 2027.

The positivity regarding the EV demand, low exchange inventories and the Russian Invasion over Ukraine led to the price growth of nickel in the March quarter 2022. Between April 2021 and February 2022, nickel price at the London Metals Exchange surged by 54% from US$16,151 to US$24,887. The nickel spot price averaged US$26,000 per tonne in March 2022.

Lithium

The battery usage for portable electronic devices in electric vehicles continued to drive the lithium demand. The batteries accounted for 75% usage of lithium in 2021. The prices of EVs were declining, the choices of models were increasing, and governments across the world were also taking favourable measures.

The global lithium demand is projected to reach 636,000 tonnes in 2022, but a cut of 30% in China’s passenger vehicles EV subsidy program may have an impact.

The strong demand in the EV sector resulted in shortages of spodumene, lithium hydroxide and lithium carbonate. Spot prices for three commodities surged to record levels. Spodumene prices averaged US$2700 per tonne in Feb-Mar 2022. Spot prices for lithium hydroxide averaged US$57,000 per tonne in February 2022 and reached over US$70,000 by mid-March 2022.

Performance of nickel and lithium in second quarter of 2022

Nickel

Manufacturing declined in China in April 2022 because of the strict COVID-19 containment measures. It was a significant hit to the world’s nickel demand. The demand was expected to grow 20% annually, but global inflation and geopolitical situations added uncertainty.

The price of nickel averaged US$33,000 in April 2022 but dropped sharply due to the reasons mentioned above. By the end of June 2022, the price was US$23,994 per tonne.

Lithium

Macroeconomic challenges, production cut in China, and delays in vehicle delivery, reduced global EV production in April 2022. By May 2022, global supply chains recovered to improve the demand.

The increase in lithium production in Australia, and several expansion projects undertaken in Chile and Argentina, are expected to meet the predicted increase in the world lithium output. The Benchmark Mineral Intelligence indicated that a US$42-billion investment will be needed to meet lithium demand by 2030.

As a result of the demand surge and low inventories, spot prices of spodumene were at a record high in June 2022, reaching US$7,000 per tonne. Spot prices of lithium hydroxide were near US$68,900 per tonne in May 2022.

There is considerable uncertainty because of long lead times for lithium mines, the potential for delays in production, and rapid price movements. Refiners and battery producers were interested in building up stocks, leading to high spot prices this quarter.

Performance of nickel and lithium in third quarter of 2022

Nickel

Despite a fall in the production of stainless steel in China, the US, and Europe, Indonesia continued to surge their steel production. The production of primary nickel in Indonesia increased by 32% in the first half of 2022.

Sales of EVS accelerated in 2021 and were forecasted to reach 11 million units in 2022. This means the use of nickel in batteries is expected to rise by 33% in 2022.

The liquidity of LME increased after the fall in LME Open Interest. Global energy prices remained at high levels, and a possible sanction on nickel exports from Russia was the factor supporting nickel prices to fall further.

Lithium

Sales of EVs were at a record high in 2022. In China alone, EV sales averaged nearly half a million a month in 2022. Key global auto manufacturers planned to accelerate the transition to EVs by developing new production lines. The global demand for lithium was estimated to be 724,000 tonnes of lithium carbonate equivalent in 2022. It is expected to surge by 40% in the next two years.

Canada is expecting three new lithium projects to start production in 2023. Mexico has nationalised its lithium resources and created a state-run company to mine lithium. Europe and North America were planning to reduce dependency on China’s imports.

The demand for EVs could not be met by spodumene, lithium hydroxide, and lithium carbonate. Their spot prices were pushed to new record levels.

Spot spodumene concentrate averaged US$4,720 per tonne in August 2022, and spot lithium hydroxide prices averaged US$70,300 per tonne in August 2022.

A look at some ASX battery metals stocks

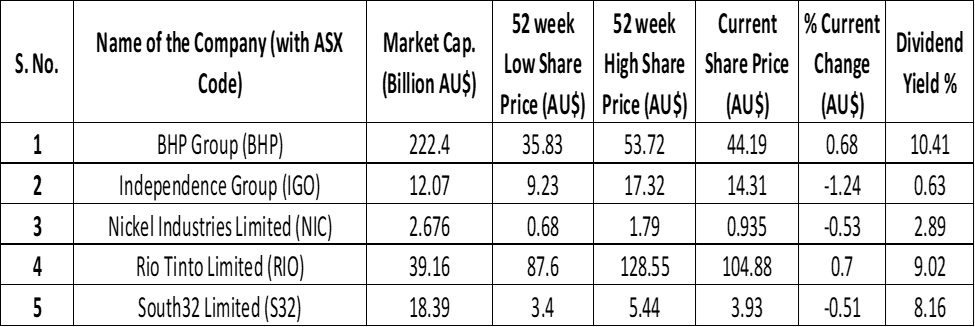

Nickel stocks

BHP Group Limited (ASX:BHP)

- In 2022, BHP announced to invest US$40 million in the Kabanga Nickel Project, West Tanzania, to produce Class I battery-grade nickel.

- BHP signed a Memorandum of Understanding (MOU) with the Ford Motor Company for nickel supply from its Nickel West Asset in July 2022. They also wished to collaborate to make battery supply chains sustainable and improve technological and commercial innovation. BHP was also advancing its nickel exploration targets internationally in August 2022.

Independence Group (ASX:IGO)

- IGO announced in June 2022 to utilise synergies across combined nickel deposits of Nova, Forrestania, and Cosmos mines in Western Australia.

- In its annual general meeting in November 2022, IGO mentioned that new nickel supply will be needed from 2026 as the demand for EVs will exceed the supply.

Nickel Industries Limited (ASX:NIC)

- In September 2022, Nickel Industries announced that grades of 6.36% nickel were reported in the infill drill assay results of the Hengjaya mine project. The average grade was found to be 1.22% nickel by using JORC Code 2012.

- Nickel Industries produced its first batch of nickel pig iron in Central Sulawesi, within the Indonesia Morowali Industrial Park.

Data source: ASX as of 29 November 2022

Data source: ASX as of 29 November 2022

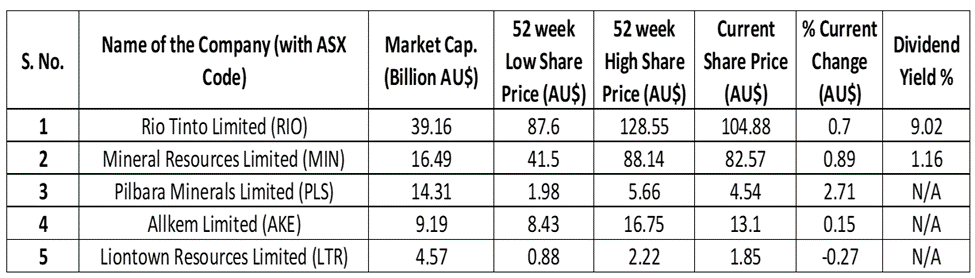

Lithium stocks

Rio Tinto Limited (ASX:RIO)

- Rio Tinto completed the VTEM Survey and identified new conductors on the Tete Nord Ni-Cu Project in August 2022.

- Rio Tinto shares outperformed the ASX200 by more than 3% in September 2022 after announcing the production of spodumene concentrate in Rio Tinto Iron and Titanium (RTIT) Quebec operations.

Mineral Resources Limited (ASX:MIN)

- The company in June 2022 announced that the Mt. Marion Ore Reserve has probable reserves of 16.4 million dry tonnes of 1.57% lithium oxide. It is a spodumene concentrate-producing mine and has been operating since 2016.

Pilbara Minerals Limited (ASX:PLS)

- The company announced the increase in production of spodumene concentrate at its Pilgangoora Project by 16% over the September quarter.

- In November 2022, Pilbara Minerals received AU$250 million long-term debt facility from the Australian Government to further expand its Pilgangoora operations.

Allkem Limited (ASX:AKE)

- Allkem Limited announced in October 2022 that its project at Sal de Vida, Argentina, had received finance of US$200 million from the International Finance Corporation. Stage 1 of the project is expected to produce 15 ktpa of battery-grade lithium carbonate.

Liontown Resources Limited (ASX:LTR)

Liontown Resources Limited was pleased to declare the approval of mining proposal and works by the Western Australia Government for its Kathleen Valley Lithium Project in October 2022. The initial project had the capacity to produce 2.5 Mtpa of spodumene concentrate. It is now planned to expand to 4 Mtpa production of spodumene concentrate in next six years.

Data source: ASX as of 29 November 2022