Summary

- Credit rating is a measure of the creditworthiness of a bank, a financial institution, or an individual borrower.

- Credit rating agencies search through the credit history of the borrowers and their financial accounts to rate them.

- The CAMEL model is one of the models used by agencies to arrive at these ratings, other models being CAMELS and rating scale.

Financial experts often give high weightage to credit ratings and use it as a threshold to measure the strength of an operating firm. Credit rating refers to the assessment of an institution or an individual based on how well-managed their liabilities are. Simply put, credit rating is a measure of the creditworthiness of a borrower or a potential borrower.

A good credit rating depicts that the borrower has a satisfactory track record of loan repayments. It is also indicative of a borrower being in a financially sound state. Thus, businesses with a high credit rating are generally termed as profitable and are more likely to receive loan approvals than those businesses with a lower credit rating.

Credit rating is given by rating agencies that do a thorough analysis of the borrower’s history and their financial accounts. In many cases, credit rating serves other roles than just being the yardstick around which creditworthiness is measured. It depicts the strength of a business or an institution.

The rating agencies

Credit rating agencies evaluate the credit ratings of borrowers based on their financial history. Both quantitative and qualitative aspects are analysed before a rating is given. These aspects include audited financial statements, annual reports and other external information like analyst reports, media articles, industry performance and forecasts for the future.

Investors and financial experts rely on the ratings given by these agencies as they are deemed to be unbiased, independent third-party organisations. Thus, these entities provide an impartial analysis of the credit risk taken up by an organisation seeking credit through loans or bond issuance.

The top three rating agencies that are most prominent include Moody’s Investor Services, Standard and Poor’s (S&P), and Fitch Group. These agencies have different rating methods and generally rate banks and other financial institutions. However, they may give similar results at times.

The types of ratings

Credit rating agencies have different techniques used to adopt credit ratings. These ratings can be divided into two types:

- Investment Grade: This is used to indicate that the investment is considered solid by the credit rating agency. These investments are less competitively priced than speculative grade investments.

- Speculative Grade: These investments are deemed as high risk and offer high interest rates to reflect the quality of the investment.

The meaning of a rating

The credit rating generally offers a rank-based analysis used to compare different types of institutions and investment tools. This rating is not a recommendation to buy, hold or sell an investment. Rather is a measure of financial soundness of the risk being undertaken.

The rating represents the willingness and ability of the issuer to repay his/her debt in a timely manner. There are readymade models available to these agencies that help the arrive at a rating.

Credit rating agencies originated in the United States in the early 1900s. The first credit reporting service was started by Lewis Tappan in New York in 1941.

The CAMEL model

The CAMEL model is a rating methodology used to arrive at a credit rating. It is one of the many methodologies used by agencies including rating scale and CAMELS. CAMEL stands for Capital, Assets, Management, Earnings and Liquidity. These can eb explained as follows:

- Capital: Capital structure includes the retained earnings and external funds, fixed dividend for preferred stockholders and fluctuating dividend for common stockholders and adequacy of long-term debts.

- Assets: This represents the revenue earning capacity of the assets which are in use or to be used.

- Management: It is the degree to which management personnel is involved and the level of decision-making used in an institution.

- Earnings: This depicts the stability and the trends in the money inflow of an organisation as well as how readily it adapts to cyclical fluctuations as well as discharges debts.

- Liquidity: This includes the stock-related policies and the policies applied for creditors apart from the effectiveness of working capital management.

The meaning of credit ratings

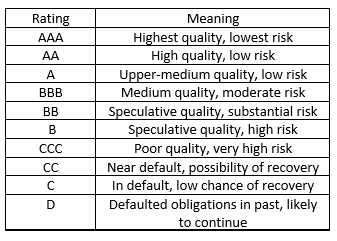

Not all agencies have the same system of rating. The following table depicts the ratings given by S&P to banks and financial institutions:

The ratings given by Moody’s and Fitch are somewhat like these with slight difference in the rating scales. Each category represents the same level of risk among the three agencies.

A lower rating may not always signify that an institution is in distress. A lower rating can be worked upon and can be improved by timely payments. However, customers and investors must be wary of investments with a junk rating. A junk rating is a direct signal to stay away from the institution or investment tool in question. For instance, junk bonds should be avoided as they have very low ratings associated with them.