Boral Limited (ASX: BLD) gets knocked down on the rating card of a leading investment banker, Credit Suisse, given the impending cyclical downturn in the housing construction market.

The building material company now sits at âunderperform gradeâ in the rating card of the Bank, down from the previous rating marked at âneutralâ. Credit Suisse also downgraded its earnings expectation for Fiscal 2020 and cut down the target price, where it would not be a surprise if the market sees BLD trading below $4.50 a share.

The ratings change charged the bears in the morning session, taking the stock down over 2.42% to $5.24 on ASX; however, it has been recovered to $5.35 in a mid-day trade, down 1.381%, as at 3 June 2019 (1:07 PM AEST).

There still seems to be a skin in the game as the company expects its Fiscal 2019 EBITDA (before significant items) to be higher than Fiscal 2018 for continuing operations. It would be a good result if Boral meets its fiscal year guidance despite the weak residential activities in Australia and the US in the March quarter, stated market expert.

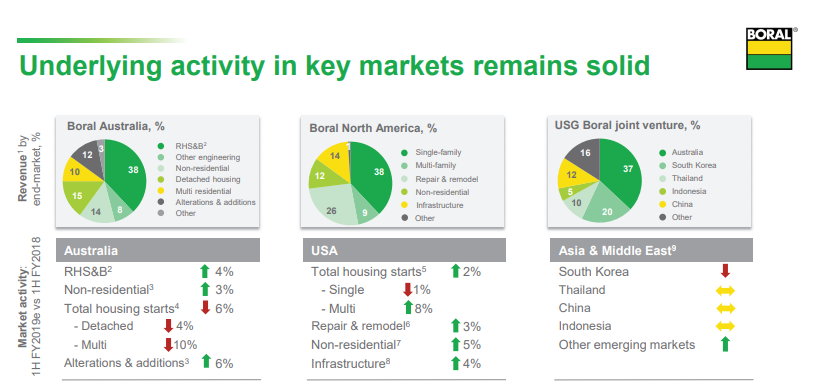

Boral market activities and revenue from its segments (Source: Companyâs Announcement)

Boral market activities and revenue from its segments (Source: Companyâs Announcement)

In the recently released investors day presentation, Boral reaffirmed its FY2019 guidance for its all three divisions- Boral Australia, Boral North America and USG Boral. The key highlights are as follows:

Boral Australia- FY2019 Earnings before interest, tax, depreciation and amortisation (EBITDA) is expected to be broadly similar to prior year excluding property earnings, which is projected to be around $30 million compared with $63 million in FY2018. The favourable performance of Boral Australia is monumental on 4% estimated industry growth in RHS&B and around 7% rise in non-residential demand, which together could offset moderating housing construction market.

Boral North America- This division is expected to flag FY2019 EBITDA growth of approximately 15% in US Dollars from continuing operations, underpinned by the synergies of ~US$25 million from Headwaters acquisition. Increase in fly ash volumes and price hike with moderate growth in underlying demand will reportedly be other few factors contributing to North Americaâs earnings growth.

USG Boral- The company expects slightly lower profits from USG Boral, reflecting a decline in residential construction activity in South Korea that includes the impact of Typhoon Soulik in the September quarter and intensifying competition. However, the company continues to eye strong result from Australia, which could consist of year-on-year improvement in earnings in 2H FY2019 not just in Australia but also Indonesia, Thailand and Vietnam.

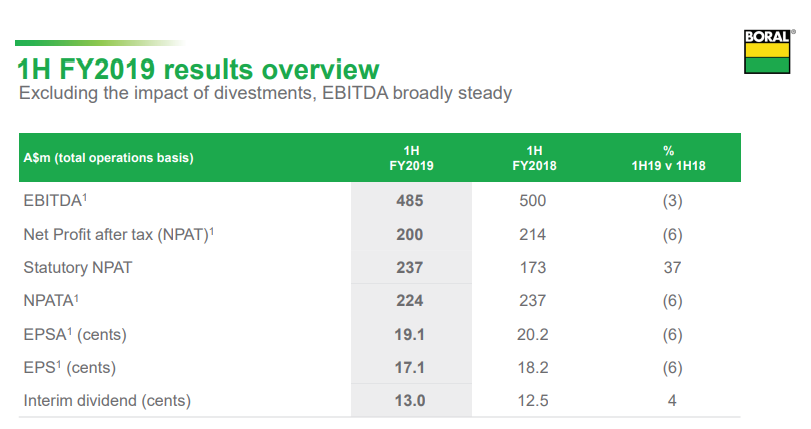

Boral 1H FY2019 Performance (Source: Companyâs Announcement)

Boral 1H FY2019 Performance (Source: Companyâs Announcement)

Boral has also been one of the most discussed companies among income investors for its consistent dividend payments. The company positioned as a good dividend payer has declared an interim dividend of 13 cents per share for 1H FY2019, compared to 12.5 cents in 1H FY2018. Its dividend policy has maintained a payout ratio of approximately 50-70% of earnings before significant items, subject to the companyâs financial position.

Now, it would be interesting to watch how this billion-dollar material company maps its future growth and gain back market expertsâ trust!

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.