Summary

- The national electricity market, which has been observing an increase in the system cost, is presently being targeted by the energy operator to make the electricity more affordable.

- To reduce the system cost and enhance the overall consumer experience across all NEM regions, AEMO plans to integrate the renewable energy into the national grid system; however, it possesses certain challenges, which the energy operator has identified and would address ahead.

- The major challenge over the integration of renewable energy or the Distributed Solar PVs (or DPVs) is the passive use and large penetration across NEM regions.

- The wind and solar generation capacity in the NEM would witness an upsurge of ~ 58.82 per cent in 2025 to stand at 27 gigawatts against 17 gigawatts in 2019, and such a large generation with a plan of integration into the national gird would not be without certain challenges and relevant opportunities

Renewable energy sector is the emerging poster boy within the energy sector with increasing integration into the national grid, resulting in reducing the average electricity cost to consumer. In the recent past, the national electricity market (NEM) has come under pressure thanks to higher penetration of solar PVs across the continent and falling gas prices.

To Know More, Do Read: NEM Prices Average At Multi-year Low As Demand Dazes And Gas Price Declines in Q12020

The government plans to integrate renewable energy into NEM through a multi-year plan, which would support the higher penetration of renewable energy into the national grid. Australia is already experiencing some of the highest levels of wind and solar generation in the world, with many projects getting the Morrison government backing.

Also Read: Tasmania Purposes to Increase 2022 Renewable Output by Twofold- Hydro a Supporting Pillar

Under its Draft 2020 Integrated System Plan, the Australian Energy Market Regulator (or AEMO) had proposed that under all scenarios, the least-cost future of NEM would witness continuing increase in renewable generation and its integration into the national grid, which has been consistently running on higher system cost so far.

To Know More, Do Read: No Respite in Electricity Prices; ACCC’s DMO- A Successful Measure?

Recently, AEMO released the Stage 1 of the Renewable Integration Study and based upon the analysis on the year 2025 of the Central scenario generation previously proposed by the energy regulator it estimates that the wind and solar generation capacity in the NEM would witness an upsurge of ~ 58.82 per cent in 2025 to stand at 27 gigawatts against 17 gigawatts in 2019.

For Getting Familiar With The Background, Do Read: The Future of Energy Generation in Australia; Solar to Increase Three-Fold By 2024

Integration of Distributed Solar PVs (DPVs)

The DPV generation is surging across the continent over the last decade and is further anticipated to grow; however, majority of DPV systems are being operated in a passive manner and are not subject to the performance standards set for the large-scale sources. Distribution network service providers (DNSPs) or the energy operator does not control it, even under emergency, which poses some technical challenges for DNSPs, mainly in the face of passive usage and large penetration.

As per the AEMO assessment, DPV generation, which already exceeds the largest scheduled generator in across the NEM, would surge by 3 gigawatts by 2025 to stand at 12 gigawatts under the Central scenario and 19 gigawatts in the Step Change scenario.

However, the main challenge related to the DPVs is its passive use at the household level, which could be addressed by better integration, improved performance standards, and minimum levels of curtail ability.

AEMO’s RIS identifies a trajectory of system limits as the share of passive DPV surges ahead with limitations first arising within the distribution network at the regional level.

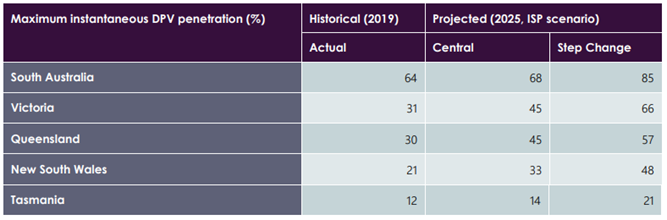

The comparison of NEW regions at present with future related to the DPV penetration is as below:

Source: AEMO

While the passive DPV generation is expected to increase over time, it presents challenges to the distribution network across NEM.

As per the AEMO survey and DNSPs planning documents, all DNSPs have started to experience voltage management challenges across their low voltage (LV) network, while the extent of DPV integration challenges remain location specific.

At present, South Australia and Queensland are experiencing the most significant challenges due to their high DPV penetration levels, and DNSPs are implementing a range of measures to improve DPV hosting capacity within their networks, including network strategies, behind-the-meter strategies.

Passive DPVs Penetration Impact on the Bulk System and Integration

The higher passive penetration of DPV generation is now impacting the energy operator’s ability to operate the South Australian power system along with many other NEM regions.

Actions to Fast Track DPVs Integration into The Grid

The aggregate performance of the DPV fleet is becoming increasingly critical as penetrations increase and without action, the largest regional and NEM contingency sizes will increase due to DPV disconnection in response to major system disturbances.

To address the same challenge, the energy operator would fast-track requirement for short duration voltage disturbance ride-through for all new DPV inverters in South Australia and would also encourage other NEM regions to do the same while investigating the need for updating existing DPV fleet to comply with fast-tracked short duration voltage disturbance ride-through requirement.

The energy operator would further join hand with the industry via the Standards Australia committee to update the national standard for DPV inverters.

Key Takeaways

In a nutshell, RIS represents the first stage of a multi-year plan to maintain system security across the national electricity market through the integration of renewable energy. The previous ISP (or the Integrated System Plan) along with RIS aims to reduce the average energy cost across NEM regions and maximise consumer benefits while reducing the system cost.

AEMO anticipates that the wind and solar generation capacity in the NEM would witness an upsurge of ~ 58.82 per cent in 2025 to stand at 27 gigawatts against 17 gigawatts in 2019.

However, while the renewable energy generation is estimated to witness another decade of growth ahead, one problem, which AEMO identified is the increasing passive use of DPVs.

DPVs generation is further projected to surge by 3 gigawatts by 2025 to stand at 12 gigawatts under the Central scenario and 19 gigawatts in the Step Change scenario, which possess some technical challenges for DNSPs.

AEMO identifies that the current technical challenges concerning the integration of solar PVs though DPVs could be addressed by better integration, improved performance standards, and minimum levels of curtail ability.