_02_06_2025_07_05_23_538703.jpg)

Summary

- Halma Plc had reported a decline of 5.0% in its revenue during H1 FY21.

- The Company had sold Fiberguide Industries to Molex for total cash consideration of £28.1 million.

- The Return on sales of the Company remained flat at 19.7% for H1 FY21.

- The Company had declared an interim dividend of 6.87 pence per share to be paid on 05 February 2021.

Halma Plc (LON:HLMA) is the FTSE 100 listed industrial stock. The Company is a well-established electronic equipment player. Based on its 1-year performance, shares of HLMA have generated a return of about 13.48%. Shares of HLMA were down by close to 0.70% from the last closing price (as on 22 December 2020, before the market close at 08:15 AM GMT).

The Company has four reportable business segments - Process Safety, Infrastructure Safety, Environmental & Analysis and Medical.

Business Model

The Company is currently operating in 20 countries with the majority of its operations present in the UK, Europe, Asia and the US. The Company is bifurcated into four sectors briefed below -

Process Safety – It includes products targeting assets and employees present in the workplace. The key products are corrosion monitoring products, specialized interlocks and explosion protection instrument.

Infrastructure Safety – It encapsulates a range of products detecting hazard to protect people and assets in public places, transportation and commercial buildings through its wide variety of products like fire detection, suppression systems and fire & smoke detectors.

Environmental & Analysis – The Environmental & Analysis deals with products and technologies used in safety, environmental markets and life sciences.

Medical – It focuses on bringing the quality of products and services used by patients and healthcare providers.

Recent News

On 21 December 2020, the Company had updated that it had acquired Static Systems Holdings Limited for £37 million, on a cash and debt-free basis.

On 18 December 2020, the Company had updated regarding the details of the transaction involving the sale of Fiberguide Industries. The Company had sold Fiberguide Industries to Molex for a total cash consideration of £28.1 million on a cash and debt-free basis. The Company had acquired Fiberguide in 2008. This transaction involving divestment was falling in line with the Company’s strategy with an objective of generating strong growth and return in the long term.

On 04 December 2020, the Company had updated that Paul Walker will be appointed as the Chair of RELX Plc with effect from 01 March 2021. He will step down from the Chair of Halma Plc by the end of July 2021 as announced on 23 September 2020.

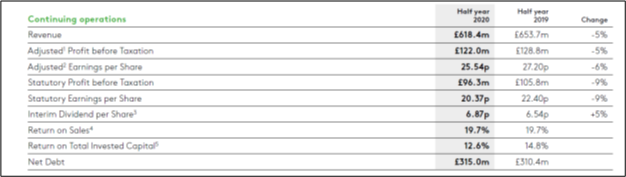

H1 FY21 results (ended 30 September 2020) as reported on 19 November 2020.

(Source: Company result)

- The revenue of the Company had reduced by 5% to £618.4 million during H1 FY21 ended on 30 September 2020 from £653.7 million achieved in H1 FY20. The Company had witnessed an improvement of 11% in Q2 FY21 revenue from the levels achieved in Q1 FY21.

- Similarly, the adjusted profit before tax also went down by 5% from £128.8 million during H1 FY20 to £122.0 million for H1 FY21.

- The adjusted earning per share also dropped to 25.54 pence per share during H1 FY21.

- With regards to its financial position, the net debt of the Company had increased to £315.0 million during H1 FY21.

- The Return on sales of the Company remained flat at 19.7% for H1 FY21 due to discretionary cost reduction of over £20 million during Q1 FY21 in comparison to Q4 FY20.

- The Company had declared an interim dividend of 6.87 pence per share to be paid on 05 February 2021, while it was 6.54 pence per share during H1 FY20.

- The R&D expenditure of the Company was £34.4 million, which accounted for 5.6% of total revenue during H1 FY21, while it represented around 5.3% of revenue during H1 FY20.

- The USA was the largest contributor to sales in H1 FY21, as it had achieved around 41% of the total revenue.

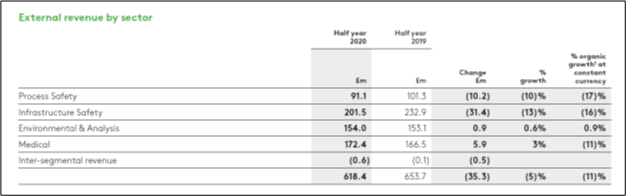

Operational Segments review

(Source: Company result)

Process Safety – The revenue across process safety business segment had registered a decline of 10% despite a significant positive contribution of 7% from the acquisition of Sensit Technologies in the prior year. The profitability went down by 33% during H1 FY21 from the equivalent period of the prior year due to the reduction of high-margin USA onshore oil & gas revenue.

Infrastructure Safety – The Company had delivered a 13% decline in revenues to £201.5 million due to weak performance in Fire, Security and Elevator safety, partially offset by positive contributions from the acquisitions of Ampac and FireMate. The profit was 12% lower than that of its prior year to £46.0 million during H1 FY21.

Environmental & Analysis – The revenue across this business segment was increased by 1% due to a strong growth of 10% witnessed in Photonics, representing around 50% of the sector’s revenues. The Company had seen exceptional growth of 22% in its profit to £38.3 million during H1 FY21.

Medical – The Company had achieved a 3% increase in revenue from £166.5 million during H1 FY20 to £172.4 million during H1 FY21 due to a significant rise in demand for products regarding the treatment of Covid-19. However, the profitability went down by 3% due to an increase in R&D expenditure.

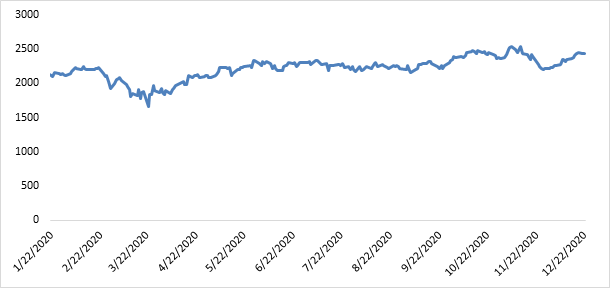

Share Price Performance Analysis of Halma Plc

(Source: EODHD/Others, chart created by Kalkine group)

Shares of Halma Plc were trading at GBX 2,416 and were down by close to 0.70% against the previous closing price as on 22 December 2020, (before the market close at 08:15 AM GMT). HLMA's 52-week High and Low were GBX 2,609 and GBX 1,660, respectively. Halma Plc had a market capitalization of around £9.24 billion.

Business Outlook

The Company had kickstarted its second half of the year on a good note having its order intake more than that of revenue and an increase from the equivalent period of the last year. The resilient trading performance and good cash position are enabling the Company to take a critical strategic decision towards making several lucrative investments during H2 FY21. The Company is expecting its adjusted profit before tax to be around 5% lower in FY21 than that of FY20. The Company is expecting its capital expenditure to be estimated approximately £30.0 million and net finance expense of about £10.8 million during FY21.