US Markets: American equities opened largely flat on Wednesday, 27 October, with the Nasdaq Composite strengthening towards its record high, while Dow Industrials and S&P 500 oscillated in the negative region due to a mixed set of corporate results. The higher-than-anticipated performance in the July-September quarter by General Motors, McDonald’s and Coca-Cola impressed the investors, while the shares of Microsoft led the gains, emerging as the biggest positive point contributors to the Dow Jones Industrial Average.

Market participants have turned partly cautious due to the back-to-back macroeconomic releases with the data from the US Census Bureau indicating a month-on-month decline in the new orders for US durable goods in September 2021 as compared to the uptake in August. Subsequent to a downward revision, the new orders for durable goods in August of 2021 rose by 1.3%.

This has been the first drop in the five months as supply side challenges continue to hurt the businesses as they look to overcome the deep-rooted troubles. The supply chain and logistics problems could escalate the problem for businesses if the counter measures by the Washington administration fail to resurrect the level of supply.

Meanwhile, the goods trade deficit of the United States widening to $96.25 billion in September of 2021 also raised eyebrows as the country struggles to keep up the pace of exports. This has been the largest gap between the exports and imports since the series started in 1955, the advance estimates by the US Census Bureau showed.

What made Global Stocks give up three- day gains?

Driven by the contraction in export of industrial supplies, automotive vehicles, capital goods and foods, feeds & beverages, the net exports from the United States dropped by 4.7% in September, effectively stretching the trade deficit in the reporting month.

The part of caution is also due to the upcoming announcement and releases with the US Bureau of Economic Analysis readies to reveal the GDP growth rate for the United States in the July-September quarter on Friday, 28 October. Alongside this, the US Department of Labor is set to reveal the number of people seeking the unemployment benefits in the preceding week.

US Market News: The broader market index S&P 500 was largely unchanged at 4,575.64, up 0.2% from the previous closing of 4,574.79, the Dow Industrials slipped 88.39 points or, 0.25% to 35,668.49, from the last close of 35,756.88, while the tech heavy stock barometer Nasdaq Composite advanced 80.32 points, or 0.53% to 15,315.66, from the previous mark of 15,235.72.

Shares of Xilinx, Tesla, Alphabet, Microsoft, CrowdStrike Holdings and NetEase rose between 2-7%, effectively complementing the Dow Jones Industrial Average and the wider share index S&P 500. The rise in the aforementioned shares was partly counterbalanced by the drops in shares of Fiserv, Pinduoduo, Texas Instruments, Analog Devices, Moderna, Cognizant Technology, and Peloton Interactive.

Amidst the 30 components of Dow Industrials, the stock of Visa emerged as the biggest laggard, followed by the shares of Dow, JPMorgan Chase, Walgreens Boots Alliance and 3M. Among the major heavyweight corporations, Ford Motors and eBay are slated to announce their respective July-September earnings report cards after the closure of the market.

UK Markets: UK shares hovered in the negative region on Wednesday, 27 October, with the headline FTSE 100 snapping the three-day gain and the mid-cap reflector FTSE 250 struggling to hold marginal gain due to mixed earnings and market-wide subduedness due to the Autumn Budget 2021 presentation.

The Chancellor of the Exchequer Rishi Sunak unveiled the Autumn Budget today, announcing a wide range of protective measures for the ailing industries to augment the pace of recovery.

The global heaviness amidst the capital markets has been weighing on the London equities with the major round of earnings coming to an end. However, a set of blue-chip companies are yet to report the quarterly figures in the upcoming days as Royal Dutch Shell, British American Tobacco and Lloyds Banking Group prepare to release the financial results on Friday, 28 October.

In the next week, large-cap corporations including BP, BT, Standard Chartered, Flutter Entertainment, Croda International, Next, Smith & Nephew, J Sainsbury and IAG are slated to release the earnings report card. The benchmark FTSE 100 traded at 7,252.55, down 0.34% from the previous close of 7,277.62, the mid-cap index FTSE 250 surrendered the gains in the terminal trade to 23,181.25, up 0.08% from the last close of 23,161.27.

FTSE 100 (27 October)

Source: EODHD/Others

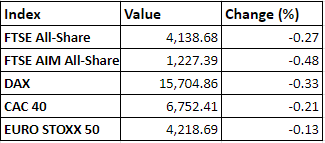

Market Snapshot

Top 3 volume leaders: Lloyds Banking Group, Glencore and Taylor Wimpey

Top 3 sectoral indices: Consumer Services, Electricity Generation and Distribution and Household Goods

Bottom 3 sectoral indices: Insurance, Industrial Metals and Personal Goods

Crude oil prices: Brent crude down 1.69% at $84.20/barrel; US WTI crude down 1.65% at $83.25/barrel

Gold prices: An ounce of gold traded at $11,794.25, up 0.05%

Exchange rate: GBP vs USD - 1.3728, down 0.28% | GBP vs EUR - 1.1841, down 0.24%

Bond yields: US 10-Year Treasury yield - 1.570% | UK 10-Year Government Bond yield - 0.9820%

Markets @ 16:30 BST