.jpg)

With increasingly complex and ever-changing nature of the financial world, the individuals are compelled to seek qualified and experienced guidance in anticipation to secure financial stability in the future successfully.

In this article, we will give you a general overview of the significance of Financial Adviser Services. We will also touch upon the key difference between General Advice and Personal Advice.

Need for Financial Advice?

An abundance of information on financial instruments, investing options and more are available either for free or just a click away. Numerous websites upload various investment plans regularly and help in calculating short term and long-term gains based on them. Do you think that it is humanly possible to scan all this available information and isn’t it difficult as a retail investor to understand where to invest and at times how to invest?

The highly volatile nature of the financial markets across the globe has triggered the desire to gain easier access to quality financial advice that can benefit from fulfilling the needs as well as the objectives of investors.

As financial advisers hold profound knowledge about the different financial market instruments, they help investors by addressing their investment needs and take wise decisions.

Broadly, there are two types of financial product advice, namely, general advice and personal advice.

It is important to note that there exists a distinction between general advice and personal advice before a financial adviser is selected.

For offering factual information about financial products, which does not intend to imply any opinion or recommendation about a financial product, an individual need not be licensed; however, an appropriate licence is required for offering general advice or personal advice.

Let’s dig deeper into understanding general advice and how is it different from personal advice.

What is General Advice?

General advice is a type of financial advice which can be offered by someone holding an Australian Financial Services (AFS) license for

- Making a statement which intends to influence the decision making of a person regarding a financial product or a class of financial products.

- And most importantly, financial advice to be general advice requires that no discussion be made about the client’s objectives, personal or financial situation in relation to a specific situation.

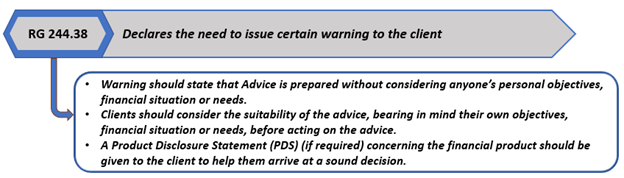

Disclosures required while giving General Advice

- Carrying a prescribed warning is a must in case of general advice and may include a qualitative assessment about, or an evaluation, analysis, or judgment of, certain or all the features of a financial product.

- Financial Services Guide - mentions the details about the entity providing the financial service and the services offered by the license holder.

Some examples of general advice can be as follows:

- Consultations with prospective clients discussing certain investments without gaining information about their personal circumstances, objectives, as well as current investment.

- Offering research information or education material like general information on superannuation can be used as a General Advice.

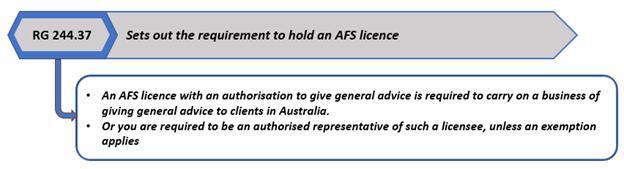

What does it require to give general advice under an AFS licence?

As per the Corporations Act 2001, Authorised representatives and advice providers who offer information and advice to retail clients in Australia concerning financial products are guided through ASIC’s Regulatory Guide (RG) 244.1, which sets out guidance for all Australian financial services (AFS) licensees.

General Advice is defined under section 766B(4) of the Corporations Act 2001 as financial product advice that is not personal advice.

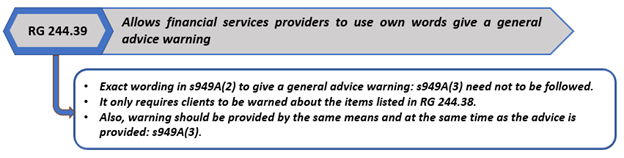

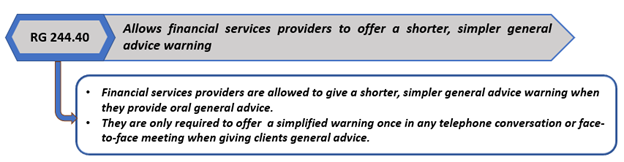

One of the requisites for giving general advice is to be authorised under an Australian financial services (AFS) licence to offer advice on financial products. Providing general advice under an AFS licence requires the following regulatory guidance to be followed:

Data Source: ASIC’s Regulatory Guide (RG) 244.1; Image source ©Kalkine Group 2020

Who are exempted from the licensing requirement?

Regulatory Guidance 244.41 of the ASIC’s Regulatory Guide 244 exempts financial product issuers from the compulsion of obtaining an AFS licence or authorisation to offer general advice regarding the products or the class of products they issue.

Few conditions regarding the above licensing exemption are set out in RG 244.42, which are as follows:

- Informing the client for not being licensed to offer general advice about their own product

- Recommending the person to obtain a Product Disclosure Statement, if suitable, and read through it before deciding

- Notifying the client about the availability or, if not, of a cooling-off regime that pertains to the purchase of the product, in case of offering advice about the offer, issue or sale of a financial product.

How is general advice different from personal advice?

As elaborated above, giving general advice does not take into consideration an investor’s personal goals or objectives, or the ways it may possibly affect an individual personally. A financial adviser can offer personal financial advice which is tailored to an investor’s financial situation and goals. Few examples of personal financial advice can include:

- Support to a retail investor by creating a financial plan to meet its financial goals through insurance, investments, retirement planning etc

- Regular monitoring of the investors’ personal and financial situation and changing the financial plan as and when required.

What is to be taken care of while giving personal advice?

Personal Advice is always presented in a way which is considered to have taken into account one or more of the investor’s objectives. There are specific best interests’ duty and related obligations imposed on the persons who provide personal advice.

Regulatory Guidance 244.50 sets out the following obligations on persons providing personal advice:

- Acting in the best interests of the client while offering personal advice.

- Providing the client with proper advice.

- Warning the client about the advice which is based on incomplete or inaccurate information.

- Prioritise the client’s interests.

Exceptions to personal advice?

Having personal information about a client does not always mean that the advice given to the client is personal advice. An adviser can make use of personal information of a client while giving more relevant general advice to a client. For example: A brochure mail sent out to all the members of a superannuation fund on retirement planning issues, highlighting it is general advice and most relevant to people above the age of 60.

Information given by the adviser may be factual and includes no proposal or declaration of opinion meant to influence the client.

In Australia – while providing personal advice to a retail investor, a “Statement of Advice” should also be given to the client.

Whereas, while giving general advice this statement is not needed.

In essence, it is important for the adviser to disclose to the client about the type of advice they are giving, regardless of obtaining his/her personal information.

Remember, a general advice does not consider your individual investment, financial situation, objectives, or needs. You should therefore analyse whether the advice is appropriate to your investment requirements before acting upon it. You may seek further advice from a stockbroker or other financial professional as necessary before acting on any such advice.