_06_04_2026_05_16_02_212823.jpg)

Highlights:

- Snowflake projected that its annual product sales growth would slow down compared to its previous triple-digit percentage growth.

- In Q4 2022, the product revenue of Snowflake increased 102 per cent year-over-year (YoY) to US$ 359.6 million.

- Snowflake is a cloud-based company and earns revenue when its customers store data and ask questions on its platform.

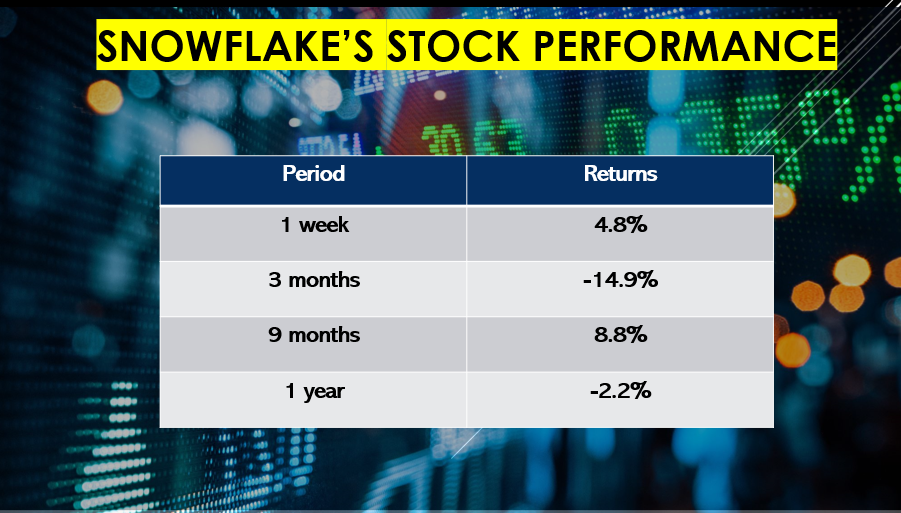

Stocks of Snowflake Inc. (NYSE:SNOW) nose-dived after the company provided financial guidance for 2023 along with its financial results for the fourth quarter and fiscal year 2022.

Snowflake projected that its annual product sales growth would slow down compared to its previous triple-digit percentage growth.

At the time of writing, the SNOW stock was down 22.1 per during pre-market trading hours and priced at US$ 207.5 per share. Meanwhile, at market close on Wednesday, March 2, the Snow stock closed at US$ 264.69 apiece.

A look at Snowflake's earnings

It is estimated that the company's data storage and analysis products will generate lesser revenue in the short term as customers would get the same results despite spending less.

Frank Slootman, the chief executive officer (CEO) at Snowflake, said that the full-year impact is significant; however, the company expects to get more clients in future as they would get the same results at lesser prices.

©2022 Kalkine Media®

©2022 Kalkine Media®

In Q4 2022, the product revenue increased 102 per cent year-over-year (YoY) to US$ 359.6 million. Meanwhile, Snowflake's net revenue retention rate was 178 per cent.

The operating loss of Snowflake was US$ 152 million in Q4 2022, whereas, for the full year, the operating loss was US$ 715 million.

For fiscal 2023, the company expects to clock maximum product revenue of US$ 1.9 billion after a YoY growth of 67 per cent. The forecast represents a decline as Snowflake's revenue growth doubled YoY in every of the last six quarters.

Also Read: What's next for investors as Vroom (NASDAQ:VRM) stock declines 46.5%?

Snowflake is a cloud-based company and earns revenue when its customers store data and ask questions on its platform. Therefore, unlike other cloud-based software vendors who charge a monthly subscription fee, it has a different business model.

Bottom line

Salesforce.com Inc (NYSE:CRM) provides enterprise cloud computing solutions, and on March 1, the company posted stellar fourth quarter and full-year results for fiscal 2022.

In Q4 2022, the revenue was US$ 7.33 billion, representing an increase of 26 per cent YoY. Meanwhile, the total revenue in 2022 was US$ 26.49 billion, up 25 per cent YoY.

The cash generated from operations in fiscal 2022 was US$ 6 billion, significant growth of 25 per cent from Q4 2021.

For the first quarter of Q1 2023, Salesforce has increased its revenue guidance and estimates it to be between US$ 7.37 billion to US$ 7.38 billion, up about 24 per cent YoY.

At the end of the trading session on March 2, CRM stock was up about one per cent and priced at US$ 210.39 apiece.

Also Read: 5 stocks to buy in March as Russia-Ukraine war impacts commodities

Please note, the above content constitutes a very preliminary observation or view based on market and is of limited scope without any in-depth fundamental valuation or technical analysis. Any interest in stocks or sectors should be thoroughly evaluated taking into consideration the associated risks.