Bank of Queensland (ASX: BOQ) is one of the leading regional banks in Australia, operating several brands engaged in offering a diverse range of products and services, catered towards individual and business customers.

The bank is operating in a low growth part of the cycle with increased regulatory and compliance costs, growing investment requirements, accelerating industry disruption and competition, declining margins and increased community expectations.

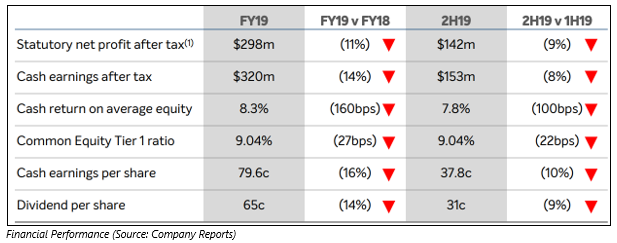

Its performance during the financial year 2019 ended 31 August 2019 were below expectations and reflected the difficult operating environment.

Disappointing Results in FY19

The FY19 statutory net profit after tax of the bank decreased by 11% from FY18 to $298 million, and cash earnings after tax declined by 14% to $320 million. During the reported period, cash return on equity also registered a decline to 8.3%, while common equity tier one lowered at 9.04% and cash earnings per share stood at 79.6 cents, which represented a drop of 16% from the year-ago period. The bank attributed these reductions to factors including a large jump in loan impairment expense, lower income, and higher operating expenses.

The dividends declared were in line with the reduction in cash earnings per share. The bank declared second half dividend of 31 cents, resulting in a full year dividend per share at 65 cents, which represented a reduction of 14% when compared with the same period a year ago.

The disappointing financial performance of Bank of Queensland shows the deterioration across all these metrics in the second half relative to the first half. This, combined with the decision to reduce the dividend, highlights the challenging environment mainly in the past six months.

On the positive side, total lending went up by $937 million, or 2%, with the first half slightly stronger, primarily driven by the Business Bank, with mortgages underperforming. The net interest margins of the bank went down by five basis points when compared with the prior corresponding period, with most of the reduction evident in the first six months of FY19. The total income posted a decline of 2% and operating expenses grew by 4%, with cost to income ratio increasing to 50.5% for the year and higher in the last six months.

Loan impairment expense increased by $33 million to $74 million, or 16 basis points of gross loans, which includes several one-off impacts. Although, the underlying asset quality remains sound with arrears at low levels.

Measures Bank is Taking to Improve its Current Position

The management of the bank recognises that the results were disappointing and therefore they have a clear mandate to take decisive action and improve its performance for customers and shareholders. Some of the major challenges the bank is facing are:

- Turning around the retail bankâs performance;

- Fixing its onerous lending processes;

- Addressing its rising costs, given the revenue challenges in the current environment;

- Closing the digital gap between BOQ and its peers.

The bank has five strategies in focus to improve its current position.

First: There would be a conversion period required to return to profitable and sustainable growth. The bank needs to improve revenue and margin and restore its lending processes. The improvement in revenue and margin would increase its distribution performance and help the bank to advantageously grow the customer base in a very targeted way.

Second: The bankâs capacity to develop its purpose-led customer culture would take great leadership that is inclusive. This would lead to better business outcomes and better customer outcomes.

Third: In order to make its business easier, address costs and improve productivity, the bank is performing a structural productivity and operating model review. The bankâs objective is to increase its cost-to-income ratio and to do that, the bank would simplify and reduce the number of products it offers. A simplified business would also make it slightly easier for the bank to steer the rising investment and regulatory costs the bank faces.

Fourth: By removing the data and digital gap that has arisen with the bankâs peers is important to its success. The bank would also make sure that its Virgin Money Australia digital bank targets are achieved.

Fifth: While doing all the above-mentioned things, the bank is committed to continue strengthening itself, via compliance standards and robust risk and keeping a strong balance sheet. That is why, the bank raised $275 million in capital, to strengthen its position, which would support its calculated transformation, aimed at delivering productivity gains, simplifying the business and achieving cost efficiencies. The additional capital would take CET1 ratio to a proforma position of 9.85%.

The bank plans to return with a detailed strategy update in February 2020. Moreover, BOQ would be clear about its transformation while providing clear milestones that can be used to examine its progress.

Actions the Bank Has Already Taken

- The bank appointed new CEO and CFO/COO to run its makeover change agenda;

- The bank is conducting a productivity review to lessen its cost to income ratio and convert BOQ to a more responsive, effective and simplified business model;

- A strategic review to refocus on niche customer segments across both business and retail banks, targeting above system revenue growth in its target markets;

- Investment in improving end to end customer experience and embedding customer led purpose and culture in the organisation;

- Investment in modernising its technology infrastructure and closing the digital and data gap;

- Continuing to strengthen the bank through its recent capital raising, strong governance, compliance and prudent risk management.

Outlook for FY20

FY20 would be a difficult year for BOQ.

- The bank is expecting a lower year-on-year cash earnings in the financial year, with revenue and impairment outcomes in line with FY19; however, subject to market conditions;

- MOQ also expects higher post-Hayne regulatory and compliance costs and increased operating expenses related to its investment in technology.

Many challenges remain for the bank such as regulatory changes, customer and technology behaviour and the broader economic challenges that the sector is facing. However, according to Bank of Queensland, based on a clear and focused strategy, there are good opportunities for the bank that would enable in capitalising on and again returning to profit.

Bankâs Stock Price Performance

The stock of BOQ was trading at $7.345 per share on 13th December 2019 (AEST 12:56 PM), up by 3.305% from its previous closing price. The bank has a market capitalisation of $3.14 billion as on 13th December 2019 with an annual dividend yield of 9.14%. The total outstanding shares of the bank stood at 442 million, and its 52-week low and high is $7.110 and $10.770, respectively. The stock has given a total return of -26.70% and -25.08% in the time period of 3 months and 6 months, respectively.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.