Retirement, a major life decision, is wonderful if you have two essential things, much to live on and much to live for. And as it is popularly said, one should Retire from Work, But Not from Life.

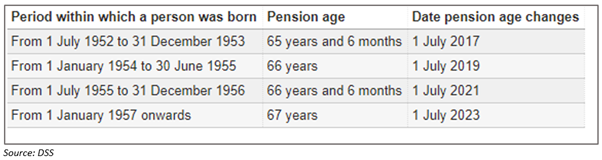

In a developed country, an individual may expect to live for another 20 years or more after his/her retirement in say, 60s. The Pension age in Australia is gradually being changed from 65 to 67 years, increasing slowly by 6 months every 2 years until 1 July 2023 (referring to the table below).

With increasing longevity, Retirement Planning has become an important financial goal. For spending those golden years doing whatever one wants to as a retiree, it is highly recommended to start with retirement planning as soon as one can in the active years of working so as to build up maximum funds for a beautiful post-retirement life.

Different kinds of support services and guidelines are provided by the Australian Government and related bodies such as the Department of Human Services, Department of Social Services (DSS), Australian Securities and Investments Commission’s (ASIC) MoneySmart and others. Besides, there are various investment schemes for individuals offered by private companies that provide retirement benefits.

Different income sources can be combined to make your money lasts as long as you do. While most retirees get income from a couple of sources, the most conventional of these are Super Funds and the Age Pension.

- Superannuation Funds

In Australia, the point of investing in Superannuation Funds (Super Funds) is to put a fraction of your income in a variety of assets and the income derived from superannuation investments is taxed concessionally, acting as a substitute or a supplement to the Age Pension. As an individual continues to work and make regular payments to his/her super, the investment grows until the retirement.

Some Basic Types of Superannuation Funds in Australia include-

- Corporate Funds

- MySuper

- Retail Super Funds

- Public Sector Funds

- Industry Super Funds

- Self-Managed Super Funds (SMSFs)

A couple planning for a comfortable retirement life may need $ 60,457 per year on an average, states the Association of Superannuation Funds of Australia’s (ASFA) Retirement Standard. There is also a Superannuation Guarantee (SG), which is the mandatory superannuation contribution of 9.5%, calculated on ordinary time earnings, that an employer must pay into a superannuation fund for their employees (eligible to receive SG if they earn $ 450 or more in a month).

A key advantage of super is that most people pay less tax than any other investments while a small downside of dealing with super is that your money is locked away until you are old.

ASIC’s Take on Superannuation: According to ASIC, there are five fundamental forces being culture, customers, compliance, competition and change that are presently impacting the superannuation industry in Australia. ASIC is particularly focussed on understanding how these forces reflect in the behaviour of trustees on an everyday basis, particularly in dealing with members (in other words, conduct), especially after the Royal Commission’s enquiry into Misconduct in the Banking, Superannuation and Financial Services Industry.

Australia’s superannuation industry is valued at more than $ 2.8 trillion, with approximately 15.6 million Australians currently saving for their retirement, according to ASIC. For Australian citizens, superannuation is a critical financial asset. In fact, for some of them, it is the only major saving planned for their retirement.

ASIC, as the conduct and disclosure regulator for superannuation and APRA (Australian Prudential Regulation Authority), as the prudential regulator responsible for system and fund performance, are both striving, in collaboration, to upgrade the working of the superannuation system for ensuring better outcomes for the members.

In line with maintaining a fair and efficient financial system, ASIC has laid out its key priorities concerning the superannuation industry such as high-deterrence enforcement action; prioritisation of the recommendations/referrals given by the Financial Services Royal Commission; delivering improvements in governance and accountability; protecting vulnerable consumers as well as addressing harms in insurance and the poor financial advice outcomes; and others.

To translate these organisation wide priorities into action focused on the superannuation industry, ASIC plans to primarily focus on-

- Advice in superannuation;

- Insurance in superannuation;

- Fees and cost disclosure;

- Taking action against misconduct by super trustees.

- Age Pension

As per Department of Social Sciences in Australia, the purpose of the Age Pension scheme is to provide financial cushion to aged residents who require it, while also urging pensioners to optimise their overall incomes. In order to qualify for receiving Age Pension, an individual must meet age and residency requirements, subject to a means test which includes an income test and an assets test.

Moreover, the pension rates are indexed twice a year, so as to keep up with the Australian price and wage hikes. Thus, how much income you receive through pensions depends on how much income you receive from other sources and what your assets are worth.

The Most Common Forms of Pension paid to retirees in Australia include-

- Age pensions

- Disability support

- Sickness and mobility allowances

- Bereavement allowances

- Wife pensions

- Widow B pensions

- Carer payments and allowances

As a last resort, if one does not qualify for the Age Pension, a concession card can be availed. Australia offers two main kinds of concession cards that provide a range of benefits, including Commonwealth Seniors Health Card and Pensioner Concession Card.

Good Read: Essentials Of Retirement Planning: Rationale, Timing, Investment Areas

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.