A global media and marketing company, Crowd Media Holdings Limited (ASX: CM8) works closely with its clients to design tailor-fit digital strategies to reach their business and marketing goals. The company specialises in Influencer Marketing, Performance Marketing and Creative Services.

Earlier, the company was known as Crowd Mobile Limited, however, in December 2018, it changed its name to âCrowd Media Holdings Limitedâ. The Rationale behind the name change was:

- Focus on its core strength in social media marketing

- Clear positioning in a high growth area

- Alignment across the group with Media, Subscription and Q&A.

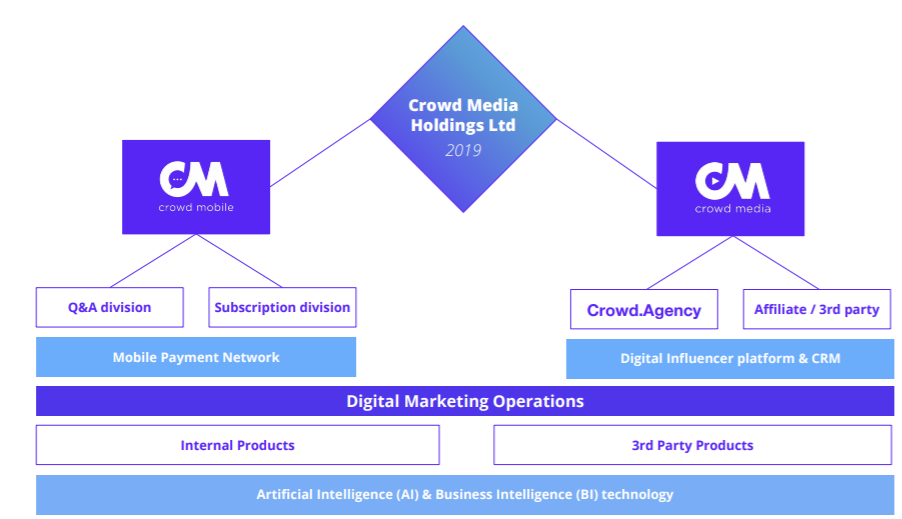

Crowd Media Holdings Limited has two divisions:

- Mobile division - Produces content including apps, music and games.

- Digital Marketing Division â Work hand-in-hand with brands and influencers to deliver branded content to the massive and fast-growing millennial and Generation Z markets.

Operating Structure of Crowd Media Holdings Limited (Source: Company Reports)

Review of operations:

In the financial year 2018, the company delivered positive financial results. CM8âs Q&A division ended the year with revenues of $24.7 million while the Subscription division achieved revenues of $13.3 million. The results from these divisions were important in assisting the companyâs continued debt repayment, which effectively reduced its net debt from $2.8 million at 30th June 2017 to $1.6 million at the end of September 2018.

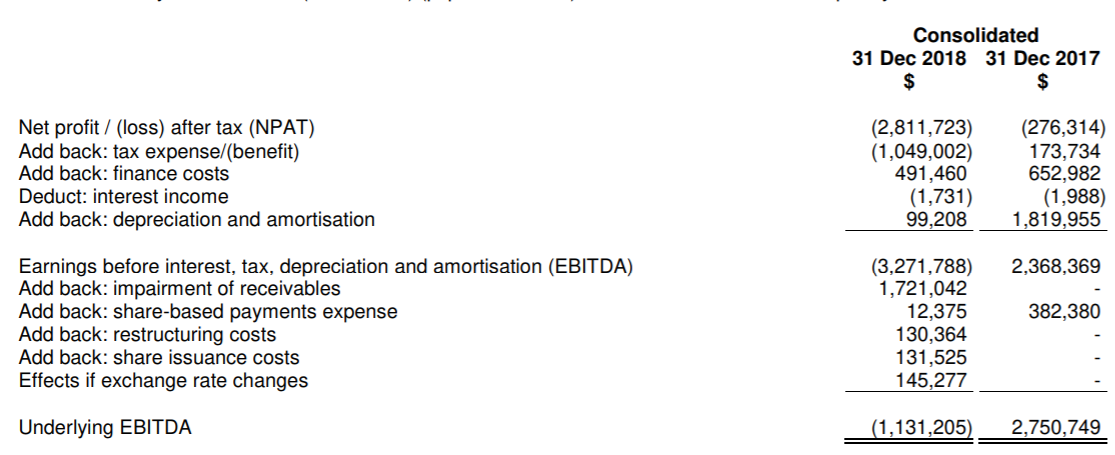

In the first half of FY19, the company reported revenues, interest and other income of $14,009,516 and net loss after tax of $2,811,723. It is to be noted that the companyâs EBITDA and net loss includes impairment of receivables of $1,721,042, a non-cash share-based payment charge of $12,375, restructuring costs of $130,364 and share issuance costs of $131,525. After adjusting these effects, the underlying EBITDA loss for the financial year amounted to $1,131,205, which is 141% less than the previous corresponding period.

(Source: Company Reports)

The half year revenues included $9,037,574 from Q&A, $3,688,171 from Subscription, and $1,283,771 from Media. The companyâs revenue is expected to stabilise in the second half of FY19, as a result of further growth of the Media business, continuous leverage of existing and new products into existing and new markets in both the Q&A, subscription businesses and reducing operating expenses.

In the financial year 2019, the company put a lot of emphasis on diversifying itself from the mature Mobile division to focus on the faster growing Media division. Letâs take a look at CM8âs Financial Plan for FY19.

Accelerate the Growth of the Media Division

- Invest in Media business and achieve breakeven within this division by Q4-FY19

- Grow revenues and margins in Media, leveraging the technology and people across the company

- Create a globally leading social media marketing organisation.

Stabilise Mobile division

- Mobile remains a strong cash generating division and hence will be managed carefully to ensure ongoing cash flow generation

- Continue to sustain the Mobile division, reducing costs, restructuring and finding new revenue niches, potential growth from new apps and products, and new geographies.

In FY2019, the company identified the need to reduce expenses across corporate and operational costs in order to move the company back to profitability. On 19th November 2018, the company advised the market that it undertook a review of expenses to streamline its future operations.

As part of its review, the company has assessed all employee and contractor costs, including those who are on a Permanent or Fixed employment agreement or a Contractor agreement. The company identified employees who had contracts, and those contracts that are expiring in the short term and not going to be renewed. It has reviewed and identified non-employee costs, which can be cut or reduced, and a number of these initiatives have already been executed.

The company has implemented redundancies that will result in an annualised cost savings of $3.5 million in FY19 and in order to fund these redundancies, the company has secured a Convertible Note to fund the employee exits and provide working capital to fund future initiatives. It is expected that Crowd Media division will again deliver improved results in FY19, with expected revenues of around $1.7 million in full year, up 240% on FY18.

Outlook for FY2020: In FY2020, through its Crowd Media division, the company will continue to deliver globally competitive social media and digital influencer campaigns to its clients and from its Crowd Mobile division, the company will focus on growing its revenues and profits again across the Subscription mobile and Q&A businesses. In the financial year 2020, the company will focus on reducing its debt and expects to achieve positive EBITDA and positive operating cashflow.

In its many releases, the company has communicated that it expects to be EBITDA positive and operationally cashflow positive from 1st July 2019 onwards.

Recent Updates:

- Executed new 3rd party agreements for digital marketing services including digital influencer marketing for multiple international brands

- Executed a pilot agreement with Moneyfarm, one of the largest digital wealth companies in Europe, reflecting the shifting focus of Crowd Media to the large and growing digital influencer and social media marketing sector.

- The company entered into a Convertible Securities Agreement with Obsidian Global Partners, LLC (Investor). The aggregate number of convertible notes issued to the Investor is 5,259 convertible notes, pursuant to which the company has raised $750,000.

At market close on 17th June 2019, CM8âs stock was trading at $0.022, with a market capitalization of $4.74 million and a daily volume of 4,711,729.

Disclaimer This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. The above article is sponsored but NOT a solicitation or recommendation to buy, sell or hold the stock of the company (or companies) under discussion. We are neither licensed nor qualified to provide investment advice through this platform.