Summary

- SIG Plc had forecasted its full-year revenue to drop by 13% to around £1.87 billion during FY20.

- The like for like revenue for Q4 FY20 went up by 4% compared to the prior year.

- The Company forecasted it would start delivering underlying operating profit from H2 FY21.

- The Company had a closing cash balance of £233 million as of 31 December 2020.

SIG Plc (LON:SHI) is the FTSE All-Share listed construction stock. The Company is the leading supplier of specialist building solutions to customers across Europe and is a specialist merchant of roofing materials to medium-sized business. Based on its 1-year performance, shares of SHI have generated a return of about negative 61.84%.

Business Model

The Company is the supplier of specialist products to the construction industry and related markets. The Company operates through two geographic segments –

- UK & Ireland

- Mainland Europe

The key activities of the Company are focused on three product division –

- Insulation & Interiors

- Roofing

- Exteriors

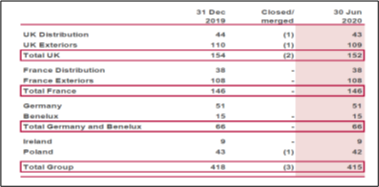

The Company had a total of 415 trading sites, 152 sites in the UK, 146 sites in France and 66 trading sites in Germany and Benelux as of 30 June 2020.

(Source: Company presentation)

Growth Plan

(Source: Company presentation)

Pre Closing FY20 Trading Update (as on 11 January 2021)

- The Company had witnessed a robust recovery during the second half of the year.

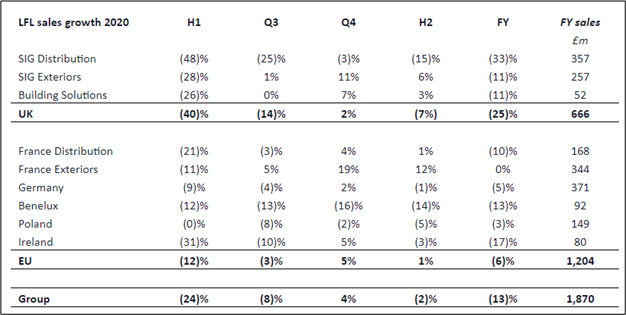

- The like for like revenue for Q4 FY20 went up by 4% compared to the prior year driven by strong demand across repair, maintenance and improvement (RMI) business segment.

(Source: Company update)

- The Company had forecasted that it would start generating underlying profit yet again from the second half of 2021.

- The Company had forecasted its full-year revenue to drop by 13% to around £1.87 billion, including its building solutions segment. The Company had forecasted its underlying operating loss in the range from negative £57 million to negative £61 million.

- The Company had highlighted that H2 FY20 LFL sales were declined by 2% compared to H2 FY19 LFL sales.

- All trading sites of the Company became operational as of 11 January 2021.

- The UK Exterior business had shown strong financial performance during H2 FY20 driven by the rising demand in the RMI segment. The UK distribution segment had shown encouraging signs due to the business performance in the last few weeks of 2020.

- The Company had delivered a decent performance in the EU courtesy of a reasonable increase during Q4 FY20. France had performed as per the Company’s expectations and had shown decent growth during H2 FY20 driven by the strong RMI demand in the exterior business.

- Regarding its financial position, the Company had a closing cash balance of £233 million as of 31 December 2020. The Company had reported a net debt of £5 million at the end of the period.

Recent News

On 16 December 2020, the Company had updated regarding the appointment of Alan Lovell as an independent non-executive director of Mitie Group Plc effective from 01 January 2021.

On 16 December 2020, the Company had updated regarding the appointment of Kath Durrant as a Non-Executive Director and Chair of the Remuneration Committee with effect from 01 January 2021. Kath would replace Kate Allum, who would no longer be associated with the Company effective 31 December 2020.

H1 FY20 results (ended 30 June 2020) as reported on 24 September 2020

(Source: Company result)

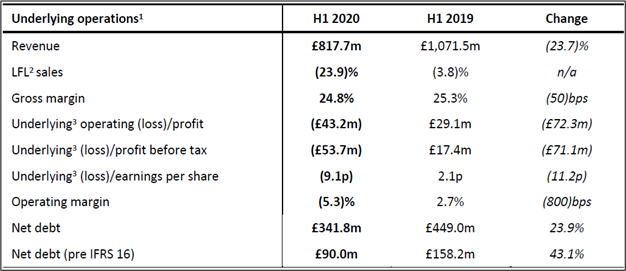

- The underlying revenue of the Company had reduced by 23.7% to £817.7 million during H1 FY20 ended on 30 June 2020 from £1,071.5 million achieved during H1 FY19.

- The underlying gross margin went down by 50 basis points to 24.8% during H1 FY20.

- The Company had reported an underlying operating loss of negative £43.2 million during H1 FY20, while it had reported an underlying operating profit in the amount of £29.1 million during H1 FY19.

- Similarly, the underlying loss before tax was negative £53.7 million during H1 FY20.

- Regarding its financial position, the Company had managed to reduce its net debt from £449 million during H1 FY19 to £341.8 million during H1 FY20.

- The Company had a net cash position of £29 million as of 31 August 2020.

- The Company had completed capital raise of £165 million in July 2020 consisting of £83 million equity investment by Clayton, Dubilier & Rice LLC.

- The Company had decided not to pay any final dividend of FY19 in order to preserve the liquidity and cancelled interim dividend for H1 FY20 as well.

- The Company had a significant liquidity headroom of £250 million as of 31 August 2020.

Share Price Performance Analysis of SIG Plc

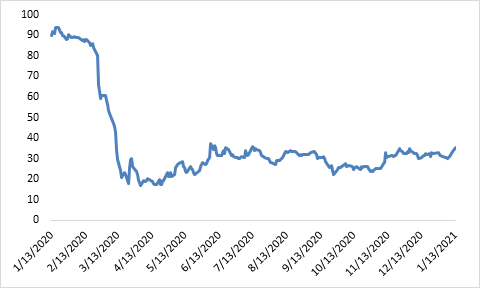

(Source: EODHD/Others, chart created by Kalkine group)

Shares of SIG Plc were trading at GBX 35.40 and were down by close to 0.55% against the previous closing price as on 13 January 2021, (before the market close at 09:00 AM GMT). SHI's 52-week High and Low were GBX 95.28 and GBX 14.38, respectively. SIG Plc had a market capitalization of around £420.63 million.

Business Outlook

The Company had demonstrated strong recovery across all geographic segments and products and delivered encouraging financial performance during the second half of 2020. The Company had highlighted the Covid-19 pandemic uncertainty may persist for short-term. However, the Company is well-equipped to tackle all the challenges. The Company believed that results of the management actions taken in 2020 would be reflected in the financial performance of 2021 and the Company is all set to show organic revenue growth in 2021 with subject to no further material disruption. The Company had established confidence regarding its profitability and highlighted it would return to underlying operating profitability during the second half of FY21. The medium-term targets set by the Company are shown below -

(Source: Company presentation)