US Markets: Wall Street indices advanced sharply on Wednesday, 1 December, bouncing back from the previous session’s drop with the three major averages gaining more than 1% each following the positive macroeconomic data with ISM Manufacturing PMI rising to 61.1 in the month of November 2021 from October’s reading of 60.8. With the back-to-back upswing in the manufacturing PMI, the manufacturing sector continues to expand for the 18th straight month after witnessing massive contraction in April of 2020, the first month of complete lockdown.

The upbeat manufacturing data clearly indicates the potential of industries as they progress ahead on the path of recovery, irrespective of the ongoing operative hurdles due to the elongated course of Covid-19 pandemic. Markets have managed to rebound from the multi-week lows, welcoming the terminal month as market participants absorb the hawkish remarks by the US Federal Reserve Chair Jerome Powell.

The uncertainty propelled by the Omicron Covid-19 variant and the cases linked to it continues to weigh on markets even as stock indices stage meaningful recovery. The vaccine makers are still skeptical about the prospective effectiveness of vaccines over the Omicron variant, at a time when healthcare authorities continue to analyse the potential extent of damage due to the new strain, its transmissibility and the variable response of humans towards it.

Global Markets bounce back | Omicron Fears Linger | Top Global News

Meanwhile, Fed Chair Powell has made it clear that the persistently high rate of inflation is no longer momentary, effectively indicating that the inflationary hurdles will take adequate time to resurrect to normal. He has further signalled about expediting the process of tapering $120 billion bond purchases every month and discussing the same in the upcoming Federal Open Market Committee policy meeting of the US Federal Reserve.

Dow Industrials briefly touched a level above 35,000 as market-wide buying pushed the index further in positive territory, Nasdaq Composite advanced more than 250 points, whereas the wider share barometer S&P 500 surpassed 4,650.

The Dow Jones Industrial Average rose 366.83 points, or 1.06% to 34,850.55, the tech leader Nasdaq Composite jumped 194.05 points, or 1.25% to 15,731.74 and the broader benchmark S&P 500 surged 62.88 points, 1.38% to 4,629.88.

US Market News: Shares of Salesforce.com cracked nearly 7% after the San Francisco-headquartered software corporation said that the present quarter profit is likely to remain lower from the previous estimates following the competitive environment in the industry.

Effectively counterbalancing the plunge and negative points provided by the Salesforce.com stock, the shares of Amgen, Travelers Companies, Chevron, American Express, Merck & Co, Cisco System, 3M, Apple, McDonald’s, Johnson & Johnson, Home Depot, UnitedHealth Group, P&G, JPMorgan Chase, Caterpillar, Goldman Sachs, Coca Cola, Intel, Walt Disney, Walgreens Boots Alliance, Honeywell International, Nike and IBM grew 1-4%.

The stock of Merck & Co rallied more than 2.5% after the United States Food and Drug Administration (US FDA) approved the antiviral drug for the treatment of Covid-19. Amid the Nasdaq Composite shares, the stocks of Vertex Pharmaceuticals, Applied Materials, Microchip Technology, NetEase, ASML, Micron Technology, NXP Semiconductors, Analog Devices, Lam Research, KLA-Tencor, Marvell Technology, Texas Instruments and JD.com gained between 3% and 8%.

While, on the other hand, the stock of Moderna extended the losses on Wednesday, effectively paring the gains realised in the previous two sessions. Shares of Moderna tumbled over 9% after the Massachusetts-based biotechnology and pharmaceutical giant lost appeal over drug delivery patents. Shares of MercadoLibre, Zoom Video Communications, Workday and Ross Stores dropped 1-4%, partly offsetting the index gains.

UK Markets: London equities gained strength on Wednesday with the domestic benchmark index FTSE 100 appreciating well above the psychological level of 7,100. During the day, the market index touched a session high of 7,182.01. Shares of BT Group topped the index with the stock advancing nearly 5%, while the equity components of Ocado Group and Croda International lost 3% each.

Among the heavyweight constituents of FTSE 100, shares of AstraZeneca, Diageo, HSBC Holdings, GlaxoSmithKline, Royal Dutch Shell, BP, British American Tobacco, Rio Tinto, Relx, Glencore, BHP Group, National Grid, Reckitt Benckiser, Anglo American, Prudential Lloyds Banking Group, London Stock Exchange Group and Experian gained up to 4%, while Unilever shares ended marginally lower.

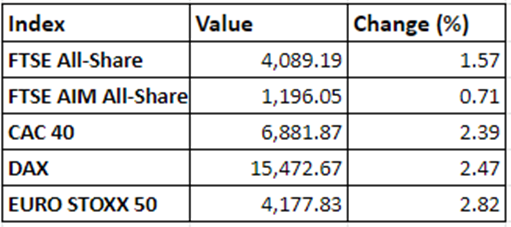

The equity benchmark FTSE 100 ended 109.23 points, or 1.55% higher at 7,168.68, while the mid-cap heavy FTSE 250 advanced 393.01 points, or 1.75% to finish at 22,912.73.

FTSE 100 (1 December)

Source: EODHD/Others

Market Snapshot

Top 3 volume leaders: Lloyds Banking Group, Vodafone and International Consolidated Airlines

Top 3 sectoral indices: Automotive, Finance Services and Health Care and Related Services

Bottom 3 sectoral indices: Industrial Chemicals, Gas and Water and Precious Metals

Crude oil prices: Brent crude up 1.94% at $70.57/barrel; US WTI crude up 1.77% at $67.35/barrel

Gold prices: An ounce of gold traded at $1,786.35, up 0.55%

Exchange rate: GBP vs USD - 1.3317, up 0.16% | GBP vs EUR - 1.1759, up 0.29%

Bond yields: US 10-Year Treasury yield - 1.465% | UK 10-Year Government Bond yield - 0.8165%

Markets @ 16:35 GMT