FCA highlights that it could lead the consumers into cycles of debt.

Summary

- Amid the scenario of many people undergoing financial distress during the coronavirus-led economic crisis, the ESAS has gained increased popularity.

- Despite presented as lucrative and beneficial option, the ESAS has attracted strong criticism in recent times.

The outbreak of the coronavirus pandemic has brought several worries for salaried people. The lockdown to curb the spread of the deadly infections were brought into effect without any prior notice to make any necessary arrangements regarding the need of cash for day-to-day needs. Besides the need to work from home as an overnight necessity for many, came the suspicions regarding future security and need for finances. Given the distressed situation, the Employer Salary Advance Schemes (ESAS) served as a solution for many who were cash-strapped.

Despite looking like a lucrative and beneficial option, the ESAS has off late attracted strong criticism citing the facts that it could lead the consumers into cycles of debt. The critics viewed that the operators target to rake the place of the payday lenders and suggested strict regulatory measures.

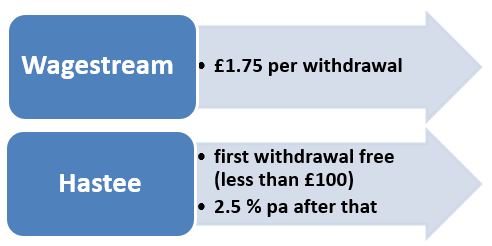

Having an arrangement with the employers, these companies usually function as a mediator between the payroll operations of the businesses and the bank accounts of their staff. Operating mostly as an unregulated business, some of these specialist scheme operators have created an app-based platform to the employees. As a standard, the withdrawals are constrained to wages already earned by the employee as per the number of shifts or hours worked to date. The businesses subtract the amount of advance availed apart from any fees or charges as applicable by the service providers from the staff’s wages on payday. Two of the popular salary advance firms in the segment are Hastee and Wagestream, through which employees can access up to 50 per cent of their salary before the pay day.

Charges by salary advance providing firms

The blow for the salary advance industry was especially noticed in July 2020 when the Financial Conduct Authority (FCA) raised its concerns over the lack of regulation. The FCA feared that the lack of clarity around costs and the temptations of repeated withdrawals would in a great probability make the workers become dependent on the services to meet their requirements. The Financial Conduct Authority is the conduct regulator for 59,000 financial services firms and financial markets in the UK, besides being a prudential supervisor for 49,000 firms and setting specific standards for 19,000 firms.

Also read: Three Unique Investment Tips to Build Recession-Proof Portfolio in COVID-19 Crisis

Also read: A Complete Guide for Securing Business Loans in the UK

Also read: Global Loans Unmanageable; High British Debt Could Trigger Another Financial Crisis

Also read: What Next For The Ailing UK Economy?

A quick look at the ESAS industry scenario

With the rising popularity of the salary advance schemes, especially when several people are under an increased financial constraints due to the coronavirus-led crisis, several ESAS operators have noticed an upward trend of users opting for the scheme. Besides, many companies have recorded a rise in people signing up on their platforms to avail the benefits of the scheme during mid-March 2020. Players registered a spike in withdrawals during the lockdown months of March and April 2020. There are an increased number of users aged around 27 with earnings of £28,000 annually and generally taking an advance four times a month on an average. Other companies informed that there was a significant rise in its users from hospitality, retail, and restaurant sectors, since the government started to ease the restrictions.

How the experts view the situation?

Many experts agreed that the ESAS operators work on the basic principles of providing the required cashflow to the employees when they need it, bringing people out of the debt cycle by removing the need for debt altogether. On the other hand, some felt that the ESAS in itself could potentially engulf people into a debt trap as people would need to borrow early the next month as the salary that they would receive at month-end would not be complete and might not service all their monthly obligations. Some industry observers described the ESAS as similar to the payday loans with a lower rate of interest and called for regulations similar to payday loans.

Exclaiming that the ESAS industry has gained a privileged status with its cheaper fees, the Consumer Finance Association, which represents short-term lenders, commented that the ESAS are cost-effective because there is zero risk of them not being repaid. It needs to be understood that in addition to having less protection, the employees bear all the risk. The association agreed with the FCA’s concerns regarding lack of or nonexistent affordability checks, besides the fact that regulated lenders would be unaware of the proofs of the wage advance while scrutinising the person’s credit files.

The concerns raised by the FCA

Presenting its views on the risks and benefits of ESAS and what employers and employees should consider when using them, the FCA observed that though the scheme has been popularised as an alternative to high cost credit, it still has similar implications. It is to be noted that the FCA’s regulations do not umbrella the ESAS as it does not comply with the definition of credit under legislation. Nonetheless, use of similarities with some credit products, the FCA considered that its observations could benefit all the relevant stakeholders, including the employers, the employees, and the scheme providers to make informed decisions.

Key concerns raised by the FCA for employees

The FCA cautioned that several scheme operators define the ESAS as a component of the wellbeing package, while further describing it as safer than the payday loans. Giving details, it stated that in case employees withdraw a portion of their salaries before the payday, they are expected to fall short before the upcoming date of salary payment.

There is a high probability that it might result in a cycle of repeat advances and surmounting fees. It could be possible that the employees may find the fees charged as modest, but still it is considered risky as they might not be able to understand the real cost. The FCA explained that in comparison with the price limitations for payday loans and other high-cost short-term credit products, the charges for ESAS could be more. The Financial Ombudsman Service would not be in a position to register any complaints. It is to be noted that the charges are generally applied based on the amount sought for the advance apart from the time of the payday cycle. Since the ESAS usually operate outside of credit regulation, the employees do not get the benefits of the regulatory and statutory rights and protections provided by the consumer credit agreements.

The FCA further added that the employees may find it difficult to compare it with the interest rate or the annual percentage rate (APR) on a standard loan. Drawing attention towards an employee seeking the advances repeatedly, the FCA observed that it could become more expensive. The employees must understand that the advanced amount and the fees would be debited from their next pay cheque. This called for a greater emphasis on being confident that the employees could meet their usual obligations and extra expenses that might come up. In the absence of such surety, the salary advances could lead to a long-term financial problem.

As a solution for cash-crunched employees, the FCA highlighted that it would be better to get proper debt advice. Some of the useful institutions that could be of help are the Money Advice and Pensions Service. In addition, the employees facing the challenges of not being able to meet their existing mortgage or credit commitments, should consult with their creditors, who may provide options like easy repayment plans.

Crucial things for the employers to consider

Highlighting the importance of accumulation of charges if an employee repeatedly opts for ESAS, the FCA advised the businesses partnering with the scheme operators to take into account various factors, including the advantages and possible risks, before offering ESAS to their employees. The FCA reiterated its fears the scheme has a high probability of making the employees dependent on it and they would choose to withdraw the salary advance as and when the financial need arises. As a responsible employer, businesses should guide the employees to seek debt related advices. Besides scanning the limitations of ESAS, employers need to understand that the short-term help provided by ESAS would not be useful to assist their employee’s larger financial problems.

Crucial things to know about the ESAS

By using the services of the companies providing ESAS products and services, workers could access up to 50 per cent of their total wages, usually for a defined fee charged by the operators, before their regular payday. Being a recent phenomenon, there are specialized companies or operators who coordinate with both public and private sector employers to provide the scheme. The FCA observed that if used in a correct way, it could be helpful in tackling unforeseen expenses and occasional short-term cash flow. Many a times, they are advertised against other high-cost credits, including the payday loans.

Conclusion

A salary advance could definitely help those who face cash shortages during a month before receiving the salary cheque. Though, it is an easy, quick, and simple way of accessing immediate cash to meet one’s needs, many experts have raised their concerns regarding the wider implications that needs to be understood before opting for the salary advance withdrawal. Given the situation of increased financial distress that many people are going through during the coronavirus-led crisis, it is important to alleviate public awareness on debt guidance, alternative avenues for credit, apart from ways to better manage one’s available finances. These crisis times call for innovators and other businesses with unique ideas that could provide substitutes for existing high-cost credit to benefit people.