_07_12_2023_11_05_52_936360.jpg)

Summary

- Housing values in September were down marginally, largely due to declines in property market movers, Melbourne and Sydney. Low mortgage rates and tight supply have helped the housing market during the pandemic.

- Regional Australia has experienced strength compared to capital cities, primarily owing to affordability and remote working environment.

- Fiscal policies have also supported housing markets. There would be more clarity on government policies after the budget, while overhaul of responsible lending norms would improve credit flow.

Real estate industry, like several other sectors, experienced adverse impacts, owing to the COVID-19 pandemic. The Australian real estate sector also witnessed subdued demand, with major impacts seen in capital cities.

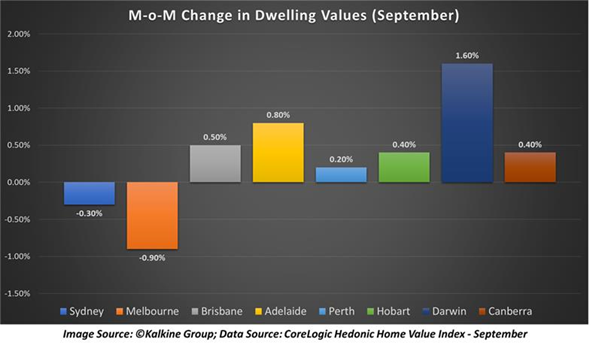

Housing values in September gained in most of the capital cities, barring Sydney and Melbourne, down 0.3% and 0.9%, respectively, according to CoreLogic. The national home price index fell by 0.1% over the previous month.

Sydney and Melbourne have more exposure to overseas migrants. Also, there has been job and income loss along with affordability constraints in the two capital cities. Sydney and Melbourne account for over half of the housing values in Australia.

But consumer sentiment is picking up in housing in overall terms with rising new listings and auction clearance rates. With lower interest rates, lenders have also passed on the rate cuts on mortgages, while further rate cut expectations have gained momentum recently.

Regional Australia relatively better than Capital cities

Since May, when housing values started falling, the 0.1% fall in national value is the smallest downward change. Melbourne values fell by 0.9% over the previous month, marking weakest outcome across capital cities.

CoreLogic believes that housing values in Melbourne would catch up as restrictions are eased. Housing values in the city are down 5.5% since the March peak. While all other capital cities have returned to positive, the rate of decline in Sydney is softening since July.

People have been remotely working since the pandemic, and there has been a trend towards regional areas. With cheaper rent in regional areas, it is perhaps the case that the working class is preferring regional areas.

Regional markets have also outperformed capital cities. Combined regional values index is down 0.8% since March against 2.6% fall in the values of capital cities. In September, regional market values in every state were up, except Western Australia.

Housing market strength and lower interest rates

CoreLogic highlighted that regional housing values have been affordable compared to capital cities, and regional markets also lagged pre-COVID gains in the housing market. They have observed that regional areas adjacent to capital cities are gaining demand because of connectivity.

Also, remote working culture has driven the regional market along with a preference for low-density housing options. They also noted that the housing market also remains susceptible to reduced fiscal support and weak labour markets.

But housing markets would be supported by other factors like low mortgage rates, expectation of interest-rate cuts, government incentives, and lower inventory levels. It was noted that the favourable environment seems to outweigh negative economic shocks due to the pandemic.

Additionally, lower housing advertisements continue to support housing markets, and new listing numbers are 22% lower than the previous year across Australia. In contrast, advertised stock levels are down 14% compared to the previous year and 17% down over the past five-year average.

A tight supply, along with recovering demand, is creating urgency in the market. CoreLogic estimated that housing sales were 2.8% higher compared to the same period last year. Moreover, such supply and demand fundamentals helped housing values to hold ground during the pandemic.

It was observed that the addition of new listings remains lower than the absorbing rate. They will monitor this trend over the coming months as financial support to households subsides, and households return to repayment after deferrals.

The auction markets have also shown strength, but Melbourne auctions were extremely lower, and auction clearance rate in capital cities is around 60% compared to 10-year average of 64%.

Rental markets

In rental markets, the performance has been in favour of house rents against unit rents; house rents were up by 0.4%, and unit rents were down 3.3% between March and September. In Melbourne and Sydney, house rents have fallen relatively lesser than unit rents.

Rents in regional markets have risen over the past six months for houses as well as units. In combined capital cities, gross rental yield is tracking at a record low of 3.85% compared to 4.23% a year ago. Sydney and Melbourne have the lowest gross rental yield, and gross yield for units remain higher than houses across every city.

The expected amendments to lending laws would enhance credit flow in the economy. CoreLogic noted that credit availability and housing markets have close relationship historically.