Summary

- The UK Treasury Chancellor to announce the schedule for public spending review and budget soon

- Speculations are doing rounds that taxes will be raised during the autumn budget

- Corporation tax, fuel duty, online retail tax, and pension tax relief rates could be tempered with

The British government is faced with the tough task of balancing its finances during the autumn budget, after giving away a lot of sops during the period of March to August 2020 to revive the country’s economy. This has already shot up the public sector net debt to an unsustainable level of £2,004.0 billion by the end of July 2020. In percentage terms, this value was more than 100 per cent of the UK GDP (gross domestic product), and close to 20 per cent higher than during the corresponding time last year in 2019.

Paul Johnson, director, Institute for Fiscal Studies, an independent research institute, has said that growth of the British economy could be slower than earlier expected, at least in the medium-term. Till the time this contracted economy comes back to its pre-corona size, public spending needs to be kept under control. If the expenditure continues to remain high, the government would need to support it by upping its revenue sources.

Public sector finances

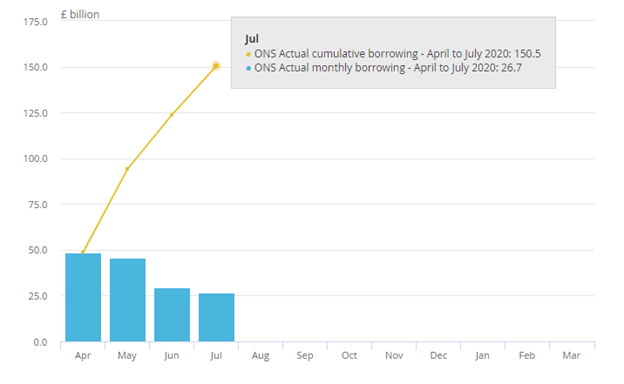

According to government estimates, the net public sector borrowings in the UK during the period of April to July 2020 totaled £150.5 billion. This was almost thrice the amount borrowed during the entire last year of FY 2020 (£56.6 billion), which explains that the government had to really blow its expenses out of proportion as a result of the coronavirus pandemic.

Public sector net borrowing (April to July 2020)

(Source: Office for National Statistics, UK)

Also Read: UK Quarterly Borrowings A Cause For Concern

For the month of July 2020, the British public sector borrowed a sum of £26.7 billion, which was £28.3 billion higher as compared to the public borrowings recorded during last year for July 2019. Generally, the borrowings for the month of July tend to be low, but for the year 2020, this high value has come around as a result of the ongoing government policies to fight the coronavirus pandemic.

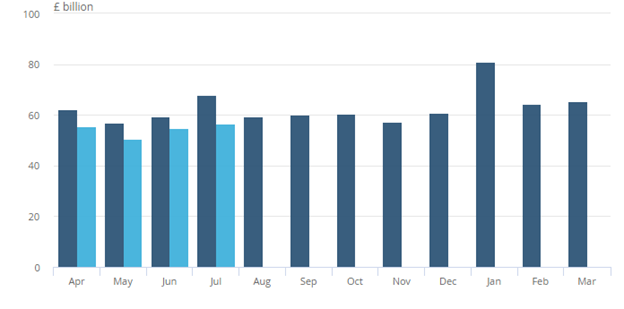

Central government receipts

(Source: Office for National Statistics, UK)

The central government receipts have been consistently falling short of their 2019 levels for all the months of the financial year 2020 till now (April to July). For instance, the July 2020 monthly current receipts were £56.6 billion, as against a higher collection value of £67.9 billion during the corresponding period in they previous year 2019.

UK’s tax levels lower than many other nations

According to the IMF (International Monetary Fund) statistics, the revenue for the UK government as a percentage of its GDP was 37 per cent for the year 2019. The corresponding value was much higher for many other European nations such as Norway (58), Denmark (55), Finland (54), France (51), Italy (46), Germany (45), and the Netherlands (45).

Therefore, from this stand-point at least, there is enough room to raise the total amount of government revenue and lower the UK government’s fiscal deficit.

Opinions differ on when to raise taxes

While there is no doubt that the government would have to raise taxes somewhere or the other to collect more revenue and lower its fiscal deficit, however, some economists differ on the timing of levying the higher tax rates.

For instance, Julian Jessop, fellow, Institute of Economic Affairs explained that raising taxes now could slow down the economic recovery process. With a lot of uncertainties prevailing around the eradication of the coronavirus led pandemic, the coming autumn might not be the best time to undertake fiscal tightening measures, he opined.

In fact, even with just a tax announcement coming in, people would plan their personal finances and companies their strategic decisions accordingly, which may or may not be line with the desired economic recovery being planned out by the government.

Even if one accepts that this many not be the right time to increase the taxes, as the economy continues to struggle to reach its pre-pandemic levels of output, however, the government can at least start a healthy debate around the best ways to raise taxes in Britain, which will be least detrimental to the economy’s growth. This should definitely prepare the ground for future tax shocks to come.

Which taxes could rise?

Media reports indicate that the corporation tax could be raised by 5 per cent which could provide additional £12 billion revenue to the British government exchequers.

The rates for income tax, national insurance, or VAT (value added tax) could also be tempered with, according to sources. These variables have the potential to raise the government revenue by as much as 2 per cent of the country’s economic output.

Reforms in the existing pension tax relief system to raise taxes could also be considered, and is under discussions.

Another move could be raising the capital gains tax and equating it with the prevailing income tax rates. A fuel duty rise could also be on the cards along with a tax on online retailers.

The British economy had contracted by almost one fifth of its pre-pandemic size during the first quarter of the year 2020 (April to June period) due to the devastating impact of the coronavirus led crisis. This led the government to push up spending and extend critically required support across various industries and to individuals through its popular furlough scheme which expires in October 2020.

Also Read: What Next For The Ailing UK Economy?

Also Read: British Economy To Rebound In Q3

It is pertinent to note that during April 2020, Rishi Sunak, Chancellor, UK Treasury had imposed a new digital services tax on foreign firms. However, this tax could be dropped in the forthcoming budget since not much money has been raised under this head till now. Further, this tax is seen to be hindering the progress of the ongoing UK-US trade negotiations. This tax was projected to garner close to £500 million per annum for the British government.

Government is also considering lowering its foreign aid to contain its expenses, according to media sources. The inheritance tax could also be revamped.

Also Read: Early Vaccine Hopes May Put A Life to The Dried Dividends for The UK Investors

Finally, despite conflicting expert views on the timing of tax hikes, Sunak has indicated in the past that some taxes might need to rise in the medium-term itself, considering the dire state of the British economy’s public finances. The public sector borrowings have crossed 100 per cent of the UK GDP and cannot continue to grow forever. Therefore, probably it is the need of the hour and the British citizens would have to bear the brunt of higher taxes. While there are speculations around various types of taxes, duties, or levies that the government might tinker with, but more clarity with come during the next few weeks when government decides to formally announce the same.