Highlights

- A primary reason behind the sluggish growth of one’s savings is the bad habit of occasionally dipping into it when the money is tight.

- Keeping your regular and occasional expenses in check can ensure the safety of your savings.

- Apart from limiting your spending, having a budget can also help you stay prepared for unforeseen expenditures.

Quite often, people find their savings growing poorly despite all efforts. A primary reason behind this sluggish growth is the bad habit of occasionally dipping into one’s savings when the money is tight.

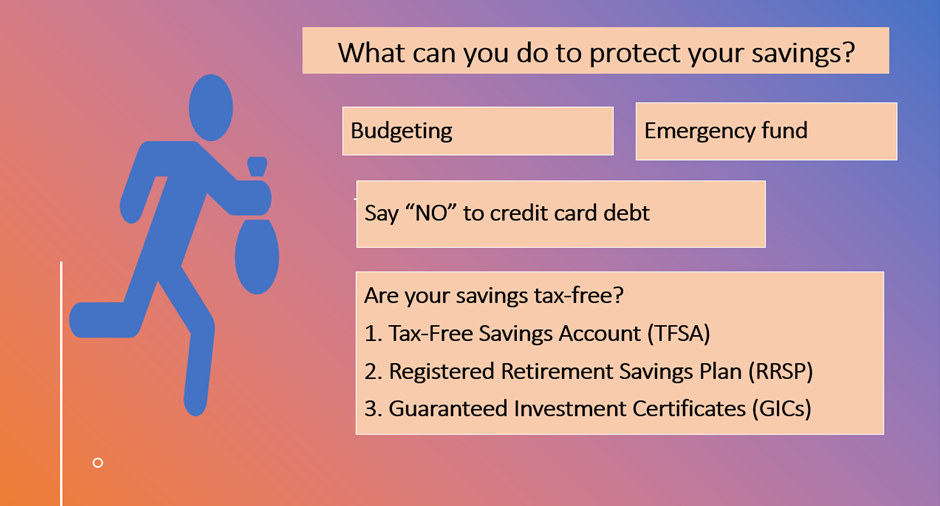

But financial difficulties cannot always be controlled or foreseen. So, how does one protect their savings from going up in the air?

Here are a few tips to follow:

1. Budgeting

Apart from limiting your spending, having a budget can also help you stay prepared for unforeseen expenditures.

Planning for your regular expenses can be a good habit. By doing so, you will be able to manage your daily and monthly bills better, which can help you in controlling the urge to dip into your savings.

Also read: The trick to save extra 20 dollars every week

2. Build an emergency fund

While you cannot stop surprises, you can always prepare for them.

An emergency fund is mainly built for unexpected and unplanned expenses, be it funding a sudden trip or a medical emergency.

3. Say ‘No’ to credit card debt

If you are in debt, bear in mind that the cost of debt is way higher than returns on savings. Additionally, penalties attached with debt, including that of a credit card, is heavy in case of default.

Hence, it is best to ensure that the money you are saving is not suffering the ill-effects of debt.

Image source: © 2021 Kalkine Media

4. Are your savings tax-free?

Considering that you have rightly set a budget and have been maintaining an emergency fund to ensure you do not exploit your savings. There is still one other essential factor that could continue to affect savings i.e., taxation.

Savings accounts rarely offer any tax benefits. To ensure that your savings are intact and free from tax, you can explore the following options:

- Tax-Free Savings Account (TFSA)

As the name suggests, a TFSA is a tax-free account for any gains and savings earned from financial assets like stocks, exchange-traded funds (ETFs), bonds, yields, etc.

These accounts allow you to withdraw money without a penalty, although they are subject to few government-mandated rules.

- Registered Retirement Savings Plan (RRSP)

This is a retirement plan backed by the government to provide tax breaks. Any money deposited in the RRSP during a given year is exempted from taxation and will only be taxed when you withdraw money.

The RRSP can be a way to save money for the future and minimize your tax bill for the year.

- Guaranteed Investment Certificates (GICs)

The GIC technically functions like a savings account. While investing in these certificates, you give your money or savings to the respective financial institution for investment purpose.

Also read: How retirees can cushion themselves against ill-effects of inflation

GICs are generally considered a safe way to protect and enhance savings. One can easily withdraw money from GICs at any point of time. Be it for a short term or long term, these certificates are known to generally offer guaranteed returns irrespective of market downturns, economic shocks, or slowdowns.

GICs also include currency options that can secure your funds from currency fluctuations.

Bottom line

Having a basic understanding of these factors can help safeguard your savings, as setting aside a fixed amount of money over a period of time is only the first step towards building a robust savings account for the future.