Highlights

- Parents can invest in different sub-categories like RRSPs and large-cap stocks

- RRSPs share some features with the 401 (k) retirement plans available in the US

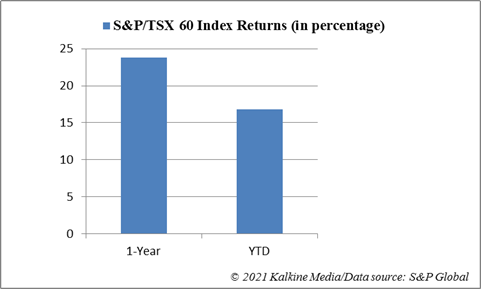

- The S&P/TSX 60 Index’s one-year return is 23.8 per cent and YTD is 16.8 per cent

Every member of the family is different when it comes to earnings and expenses. Some members manage their own expenses while others are entirely dependent on others. Kids fall in the latter category.

Invest in risky assets or large caps?

Families have to first identify a basic fact that the entry of a child will increase expenses but not earnings. Earlier, if a large chunk of this disposable income went into purchase of assets with depreciating value or riskier assets such as stocks with weak fundamentals or cryptocurrencies, the shift can now be made towards income-driven assets such a promising tech driven companies and/or blue-chip dividend paying stocks. The latter may appear less lucrative but produce steady income in the form of dividends.

Also read: Can Bitcoin be termed as the ‘asset of the century’?

S&P/TSX 60 Index

The S&P/TSX 60 Index is not the benchmark index of the Toronto Stock Exchange (TSX) but it is a very closely watched index.

The index is comprised of 60 leading companies listed on the TSX. These stocks are also the leaders in the industry they operate in. The large market cap of these stocks makes them less vulnerable to shocks and short-term hiccups. Shopify Inc. and the Royal Bank of Canada are the two leading stocks here. The market cap of these is nearly C$216 billion and C$180 billion respectively.

TSX 60 Index’s return is promising on one-year basis. At the time of writing, the one-year return was 23.8 per cent. The year-to-date (YTD) return of the index was 16.8 per cent.

Invest a little in RRSPs, a little in growth stocks

Quite often, families save without having any sub-category under this head. Sub-categories like saving for the child's higher studies or saving for own retirement can be beneficial and financially rewarding, for example, savings in Registered Retirement Savings Plan (RRSP). In RRSPs, savings grow without levy of any tax. The withdrawal is however taxed.

At the same time, the duration of savings in sub-categories can be different. Stocks of new companies in emerging technology like electric vehicles and with promising fundamentals can be good for long-term retirement savings.

Also read: 7 Canadian stocks combating climate change

Teach the child the importance of money

Educating the child about finances can be done using simple, real-world examples, like storytelling about successful entrepreneurs that manifested financial prudence and great investment skills from a very young age. Explaining the child how unsustainable debt can deal a severe blow to financial health is important.

Also read: 5 Canadian copper stocks to buy as electric vehicles demand surges

Bottom line

Savings is an art that parents must know to preserve the financial health of the household at all times. A little money can be invested in Registered Retirement Savings Plans, a little in large-cap stocks listed on the TSX, and a little in TSX emerging technology stocks.

The stock market of Canada has created wealth for investors even during the subdued pandemic phase. In this light, considering investment in stocks seems rewarding.