Summary

- Earnings at the banking sector have taken a hit with stalling business activities leading to the mounting of bad debt and customers and directors availing moratoriums leading to decreased earnings

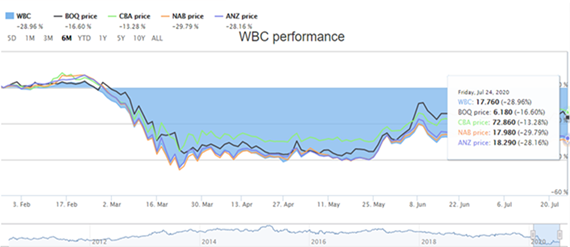

- In an uncertain future, Major banks are trading significantly below with share prices down by almost 30% within a year

- To deal with bad debt, Bank of Queensland has increased its provisions for bad loans to $71 million from $10 million

- Many banks such as CBA and NAB have issued subordinated notes to strengthen their liquidity position

The COVID-19 has baffled the banking sector as economies crippled down worldwide. Since the beginning of the pandemic, banking shares were plummeting as stalling business activities led to the mounting of high debt and customers and directors availing moratoriums leading to decreased earnings. According to ABS, in June 2020, the business sector was worst hit with 73% of businesses working under modified conditions, of which almost 72% are small businesses. Mortgage defaulting has also led to decreased earnings through interests and accumulation of bad debt. To combat bad debt, many banks have increased their provisions for bad loans.

Bets of Banking

Nonetheless, since the March bear marker, ASX has bounced with banking sector witnessing a price rally. Easing of restrictions, government stimulus programs for household and businesses supported the price rally significantly. Still, the banks are trading much lower compared to the year before.

Bank of Queensland Limited (ASX:BOQ) increased its provisions for bad loans

To combat bad debt, Bank of Queensland (ASX:BOQ) has expanded its provisions for bad loans to $71 million from $10 million. According to Australian Prudential Regulation Authority’s (APRA) Basel III Pillar 3 report released by BOQ for the period ending 31 May 2020, the bank has witnessed an increase of $112 million in +90 days past due loans. According to the management, $58 million of $112 million have availed for relief packages, and their application is under process. In contrast, the remaining amount is accounted for customers who did not avail moratoriums or relief measures or had been ineligible to avail any scheme.

According to the bank, it will continue to monitor its business with respect to impacts from COVID?19 and will update its collective provision before finalising its year-end position, which is due in October. According to CEO George Frazis, bank has deferred loans for 21,000 customers, and every four out of five customers of BOQ are yet to commence loan repayment following the three-month check-in offered by the bank. The bank also announced its common equity tier 1 (CET1) ratio to drop to 9.8% from 9.9% over the quarter to May 31.

Commonwealth Bank of Australia (ASX:CBA) closed at $72.86 on 24 July and is trading below 11.52% than a year before. However, Commonwealth Bank has recently reported an uptick in spending by CommBank credit and debit card by almost 5% higher over the previous year. CBA also issued subordinated notes of $210 million under its Euro Medium Term Note Programme of worth US$70 billion.

Westpac Banking Corporation (ASX:WBC) closed at $17.76 on 24 July. The share price of WBC dropped by 37.44% in a year. Westpac had been strengthening its management team during the COVID-19 outbreak and recently appointed Mr Anthony Miller as Chief Executive officer for Westpac Institutional Bank (WIB) to ramp up business in the institutional banking category. Mr Miller has been appointed on the new role for his 20 years’ experience in corporate and institutional banking and international exposure which is expected to bring considerable value to the Westpac bank with respect to risk management and increased customers. The company also appointed Mr Michael Rowland recently as the new Chief Financial Officer (CFO) of the group in July.

The share price of National Australia Bank Limited (ASX:NAB) has dropped by 36.53% in twelve months and closed at $17.98 on 24 July. The bank has announced various subordinated notes transactions to strengthen its liquidity position, latest being the issuance of $100 million subordinated notes due 24 July 2040. On 17 July, NAB also issued another $600 million floating rate capital notes.

Recently, the bank also highlighted $0.8914 per share distribution, fully franked, at a rate of 3.5367% per annum for NAB Capital Notes 2 set for payment on 7 October 2020 for the period 7 July 2020 to 6 October 2020.

Also Read: An Uncertain Road to ASX Banks’ Dividends

Australia and New Zealand Banking Group Ltd (ASX:ANZ) recorded a drop of 33.85% within a year. As on 24 July, ANZ share price closed at $18.29. On 25 June, Distribution Amount of $0.6815 per share was announced by ANZ for ANZPH -3-BBSW+3.80% PERP NON-CUM RED T-03-25 to be paid on September 21, 2020.

A subtle observation and future outlook

We can see from the above facts that despite a grim economic situation, the banks are preparing themselves well to battle out the impacts of COVID-19 by securing liquidity through debt and capital notes. With the resurgence of cases, the business activities that had picked up in recent times are again struggling. However, with the news of vaccines coming on board making rounds, the not so near future shows a recovering economy, leaving signs of growth across sectors.

Please Note: All financials mentioned above are in AUD, unless otherwise specified.