Two different stocks, from two different sectors; is there a commonality among them? Letâs find out. The change in stock performances and updates influence businesses. Companies undergo micro and macro level changes daily, and it is essential for investors to be wary about any such changes as it could impact their interests and returns from the stocks of the company.

In this piece of writing, we would be looking at the two stocks from the opposite sectors- Consumer discretionary player Tabcorp Holdings Limited (ASX:TAH) and Consumer staple company GrainCorp Limited (ASX:GNC).

Let us understand the fresh takeaways from the two companies:

Tabcorp Holdings Limited

Racing Queensland alleges Tabcorpâs subsidiary UBET on underpayment ground

On 24 July 2019, as per the order of the Supreme Court of Queensland, the Claim made by Racing Queensland against Tabcorp Holdings Limited (ASX:TAH) and its subsidiary UBET QLD Limited, were made public.

The Claim was filed in the court on 28 June 2019 and is related to the degree to which the point of consumption tax, was levied on UBET, accepted by it or Racing Queensland; influencing the estimation of fees falling within contractual arrangements which comprised of- Queensland Product and Program Deed between Racing Queensland or QPP and UBET along with the fees payable by UBET to Racing Queensland and the Deed of Understanding between Tabcorp and Racing Queensland or DOU, which laid down the least monetary commitments to Racing Queensland concerning the business of UBET, along with offering the yearly top up compensations for CY18 - CY20, if UBET fails to fulfil those least commitments.

Further, UBET thinks that it has right to decrease/offset fees paid to Racing Queensland by a rise of 100 per cent in wagering tax waged by UBET, as per the point under QPP. Racing Queensland agrees to the same, but for a smaller amount. Given the difference, the view on calculation of tax, Racing Queensland is paying heed to the increase attributable to the change in relevant specified percentages, from 14 per cent to 15 per cent for totalisator wagering and 10 per cent to 15 per cent for fixed odds wagering.

Racing Queenslandâs position based on the Claim is that UBET should not receive any reduction or offset to reflect the increase in tax on sports wagering revenue and post calculation of increase in tax, UBET can offset/reduce the fees paid to Racing Queensland by 39 per cent. Moreover, Racing Queensland stated that UBET has underpaid it by an amount of approximately $11 million for October to December 2018, the impact extended across the term of the QPP until 2044.

If Racing Queensland is proved right, UBET would stand the complete wagering tax rise for CY18-20 and trusts that the DOU has no requirement for any such repayment.

TAH would defend its case and is in process of its formal preparation.

Company Profile and Stock Performance: TAH is a renowned Australian provider of gambling and other entertainment services. Apart from this, it also deals with wagering and media, gaming services, and Keno (its brand) operations.

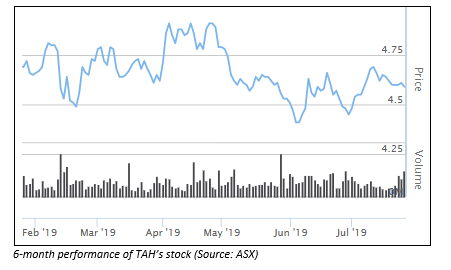

Post the ASX trading hours on 25 July 2019, TAHâs stock, with a market capitalisation of A$9.27 billion, was valued at A$4.52, down by 1.525 per cent, relative to its last trade. The YTD return of the stock has been 8.25 per cent.

GrainCorp Limited

ACCC considering GrainCorpâs proposed sale of its Australian Bulk Liquid Terminals

On 25 July 2019, Global Agri-business GrainCorp Limited (ASX:GNC) informed that the ACCC (Australian Competition and Consumer Commission) was underway in considering the companyâs plea to sell its Australian Bulk Liquid Terminal s to ANZ Terminals Pty Limited. The proposal was announced this year on 4 March and the preliminary view in the form of a Statement of Issues or statement by ACCC was delivered to the company.

According to the Statement, ACCC expressed its view on removal of a prominent competitor in the NSW, Victoria, and South Australia region apart from Queensland, being tapped by the involved parties and is a concentrated industry. ACCC feels that the acquisition would lead to ANZ Terminals, at a few places being the sole storage provider for some liquid products, rising the prices and lowering services, given the absence of any other party. Moreover, there is scarce availability of land for storage, debarring the probability of new players.

The statement by ACCC denotes a procedural step in the informal merger review process, and GNC is keen on aiding ACCC with all the details needed while it considers the transaction.

The final decision by ACCC is expected to arrive on 17 October 2019, also the transaction would be subject to FIRB approval and other conditions precedent. The company awaits the same and as of now, the GrainCorp and ANZ Terminals are working towards gratifying these conditions.

Besides, on 24 June 2019, GNC provided an update regarding the demerger of its Malt business. The demerger would proceed as per a SOA subject to its Board, shareholder and regulatory approvals, which would be rolled out post the companyâs FY19 results.

With regard to the same, the company would appoint Graham Bradley AM as Chairman of the Malt business, if the demerger were to proceed. Further, on 24 June 2019, Peter Richards was welcomed as Deputy Chairman of the company. He would take up the role of Chairman of GNC in case of the Demerger being proceeded further.

Besides these appointments, the company was hunting for a successor to Mark Palmquist as Managing Director and CEO, worldwide, as he would be the future Managing Director and CEO of MaltCo post the demergerâs implementation. Chief Operating Officer, Klaus Pamminger would continue in his post and tap opportunities recognized via the integration of Grains and Oils.

Company Profile and Stock Performance: GNC is an expert in the agrifood processing business and is one of Australiaâs leading grain exporters. It is the owner of Eastern Australia's chief integrated grain transport and storage network and its expertise and products are sought by more than 30 nations.

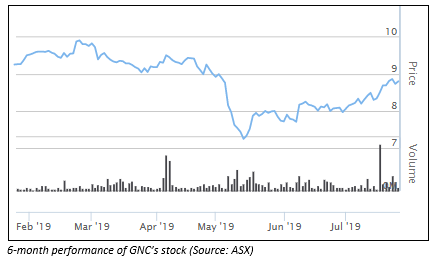

Post the ASX trading hours on 25 July 2019, GNCâs stock, with a market capitalisation of A$2.01 billion, was valued at A$8.63, down by 1.932 per cent, relative to its last trade. The YTD return of the stock has been of -2.55 per cent.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.