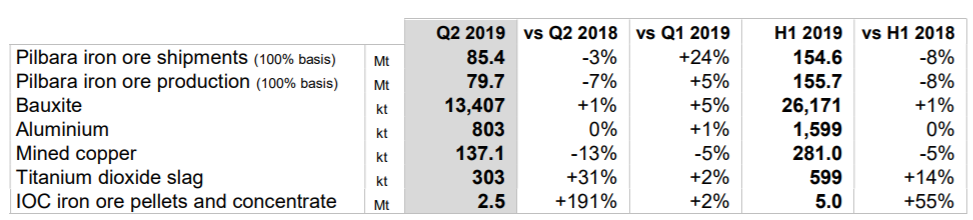

A leading global mining group, Rio Tinto Limited (ASX: RIO) witnessed challenging operational performance across its portfolio in the first half of 2019. In 2019 June quarter, the company reported Pilbara iron ore shipments of 85.4 million tonnes, which was 3% lower than the pcp. Impacted by the lower mine production and damage to the port facilities caused by the cyclone, the sales in the first half was around 154.6 million tonnes, which was 8% lower than the pcp.

Rio Tinto Second Quarter Production Results (Source: Company Reports)

In the June quarter, the company reported bauxite production of 13.4 million tonnes, which was 1% higher than the pcp. Alumina production in Q2 2019 was 6% lower than the pcp, mainly due to major maintenance activities at non-managed QAL and the lower bauxite supply from MRN.

Rio Tinto share of Production (Source: Company Reports)

In 2019, the companyâs Pilbara shipments are expected to be in the range of 320 million and 330 million tonnes. The company has confirmed that its Pilbara unit cost guidance in 2019 has been revised to $14 to $15 per tonne. In this guidance, the additional waste movement in the mines from the second half and the overall reduction in shipments is incorporated. With regards to the bauxite production, the company anticipates bauxite production for 2019 to be in the range of 56 million to 59 million tonnes. In 2019, the company expects its Aluminium production to be in the range of 3.2 mt to 3.4 mt and alumina production is expected to be between 8.1 mt to 8.4 mt.

The company currently has a strong portfolio of projects with operations in 18 countries across eight commodities.

On 16th July 2019, the company provided an update on the schedule and cost of the Oyu Tolgoi underground project, which is rapidly progressing on its path to become one of the largest copper mines in the world.

Till now, the company has completed the construction of ground infrastructure, including the control room facility and the jaw crusher system. The company is now progressing the construction of shafts 3 and 4 while the commissioning of shaft 2 remains on track for October 2019.

The company is in the process of determining the final design of the first panel of mining and expects to deliver the definitive estimate in the second half of 2020, reflecting a preferred mine design approach.

The preliminary information is suggesting that the first sustainable production could be achieved between May 2022 and June 2023 and the preliminary estimates for development capital spend for the project is now $6.5 billion to $7.2 billion, an increase of $1.2 billion to $1.9 billion from the $5.3 billion previously disclosed.

Currently, the company is focused on reducing the impact to project schedule and cost and is reviewing the carrying value of its investment in the project. The company is working closely with the Government of Mongolia and TRQ to complete the underground project.

In another announcement made on 16th July 2019, the company announced that it has completed the sale of entire interest in the Rössing Uranium Mine in Namibia to China National Uranium Corporation Limited (CNUC) for an initial cash payment of $6.5 million plus a contingent payment of up to $100 million, bringing the total divestment proceeds received since 2017 to $11.2 billion. To-date, the company has returned $9.7 billion of the total divestment proceeds to its shareholders. As per the companyâs Chief Executive, J-S Jacques, this transaction is demonstrating Rio Tintoâs commitment to further simplifying and strengthening its portfolio.

On the stock performance front, in the last six months, the companyâs shares have provided a return of 35.15% as on 12th July 2019. At market close on 16th July 2019, the companyâs stock was trading at a price of $103.250, down 0.635%, with a market capitalisation of circa $38.44 billion. Its 52 weeks high price is set at $107.990 and its 52 weeks low price stands at $66.978, with an average volume of 1,703,725.

Peer Analysis

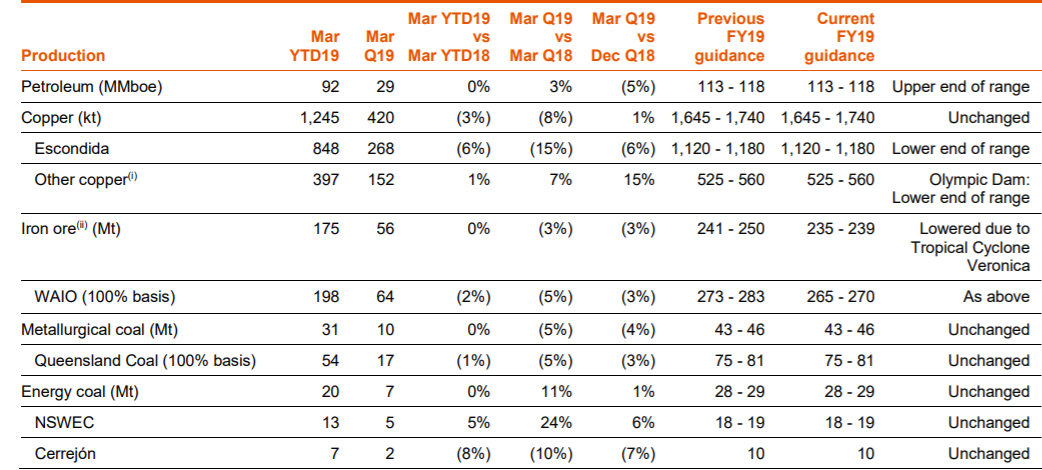

One of the major competitors of Rio Tinto is BHP Group Limited (ASX:BHP), a multinational mining, metals and petroleum company. BHP has not yet revealed its June quarter results, however, in the March quarter, it witnessed strong operational performance.

Summary of BHPâs Production and Guidance (Source: Company Reports)

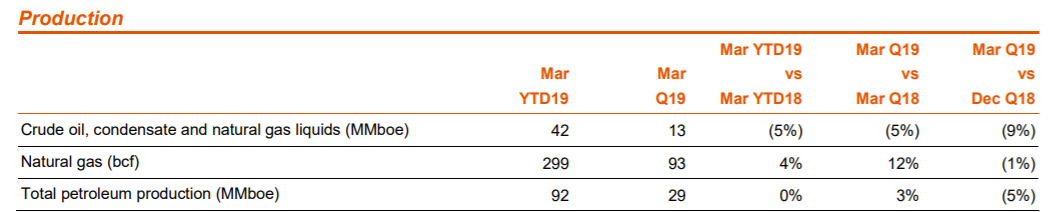

During the March quarter, the total petroleum production was flat at 92 MMboe while the crude oil, condensate and natural gas liquids production decreased by 5% to 42 MMboe, as depicted in the figure below.

(Source: Company Reports)

For the nine months ended March 2019, the companyâs minerals exploration expenditure was US$122 million. During March 2019, BHP signed a non-binding letter of intent with Luminex for an earn-in and joint venture agreement on Luminexâs Tarqui 1 and 2 mining concessions in Ecuador. Negotiations to complete a binding agreement will be undertaken over the next two months.

On the stock performance front, in the last six months, the companyâs shares have provided a return of 25.25% as on 12th July 2019. At market close on 16th July 2019, the companyâs stock traded at a price of $41.160, up 0.39% during the dayâs trade, with a market capitalisation of circa $120.69 billion. Its 52 weeks high price is set at $42.330 and its 52 weeks low price stands at $29.062, with an average volume of ~6,011,966. The stock has a PE multiple of 28.030x and an annual dividend yield of 4.07%.

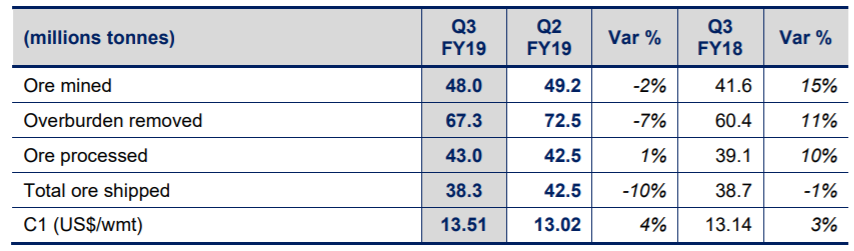

Rio Tintoâs another major competitor is Fortescue Metals Group Ltd (ASX: FMG), a world-class mining company. In the March quarter, FMG reported total shipments of 38.3 million tonnes (mt) and cash production costs (C1) of US$13.51 per wet metric tonne (WMT), as depicted in the table below.

Production Summary (Source: Company Reports)

The total ore mined during the 2019 March quarter was 48 million tonnes, which was 15% higher than the pcp but 2% lower than the previous quarter. During the quarter, the demand for Fortescueâs products was strong, reflecting continued moderation of steel mill margins, resulting in a significant reduction of Fortescue products at Chinese ports. As at 31st March 2019, the company had a cash balance of US$1.1 billion and gross debt of US$4.0 billion.

On the stock performance front, in the last six months, the companyâs shares have provided a return of 111.77% as on 12th July 2019. At market close on 16th July 2019, the companyâs stock was trading at a price of $8.990, up by 1.697% during the intraday trade, with a market capitalisation of circa $27.03 billion. Its 52 weeks high price is set at $9.550 and 52 weeks low price stands at $3.224, with an average volume of ~16,074,467. The stock has a PE ratio of 22.210x and an annual dividend yield of 3.53%.

It is to be noted that in the last six months, stocks of all three mining groups (BHP, FMG and RIO) have provided significant returns to their shareholders.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.