Australian iron ore miners are experiencing twin shock from the steel industry. First, the steel prices are losing momentum in the international market and second the high iron ore prices are pulling a halt on the steel mills demand for the raw material amid slower growth in the steel industry.

Steel Scenario:

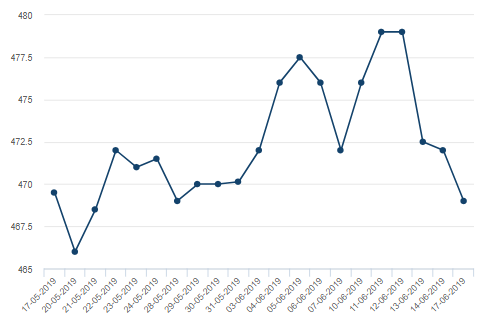

The steel prices on the London Metal Exchange lost significant value from the top of US$488.50 (Dayâs high on 1st April 2019) to the level of US$459.50 (Dayâs low on 8th May 2019), which marked a decline of approx. 6 per cent in around 11 weeks.

Post declining to the level of US$459.50; the steel rebar prices took a U-turn to the level of US$479 (Dayâs high on 12th June 2019). However, the prices on LME again lost the momentum and dropped to the level of US$469.00 (Dayâs low on 17th June).

LME Steel Prices (Source: LME)

Not just on the London Metal Exchange, the steel lost the momentum in the Chinese market as well, after ending the dayâs session at RMB 3755, down by 0.98 per cent on the Shanghai Future Exchange (as on 14th June 2019), the steel rebar future (October Contract) dipped further to the level of RMB 3700.00 (Dayâs low on 17th June 2019). The prices are currently trading at RMB 3718 (as on 18th June 4:22 PM AEST).

Steel Industry Outlook:

The prices of steel were mainly hit by slower growth in the steel sector in China as compared to the previous year. As per the data, the production of crude steel grew by 10 per cent in May from a year ago, as compared to the growth of 12.7 per cent in April 2019.

The total production for April 2019 stood at 85.03 million metric tonnes and the output in the first four months of the year 2019 stood at 314.96 million metric tonnes.

The production in May stood at 89.09 million metric tonnes, up by approx. 4.78 per cent as compared to the previous month and the output over the first five months of the year 2019 stood at 405 million metric tonnes.

On the demand side, the recent U.S-China trade war is putting a curb on the steel demand, and the high production of steel coupled with less demand in stopping Chinese domestic mills from procuring iron ore on such high prices.

Despite the weak growth, low demand of steel in the Chinese domestic market build-up the weekly steel inventory in China, which rose by 0.38 million tonnes or 3.04 per cent to stand at 12.79 million tonnes for the week ended 14th June 2019.

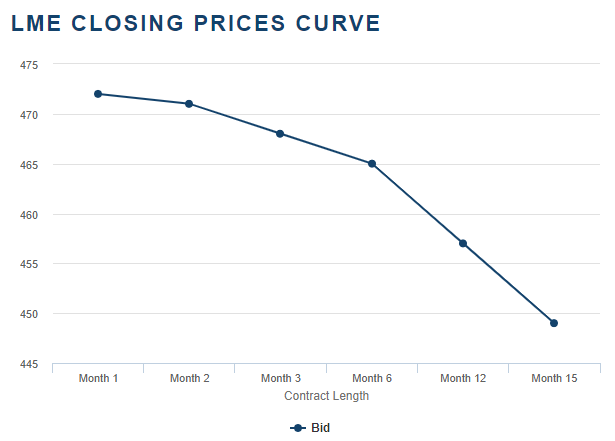

The weak demand and a slower growth exerted pressure on steel prices and turned the steel future curve on LME downwards, which in turn, dragged the steelmaking raw material prices as well.

Steel Future Curve up to 15 months contract (Source: LME)

Steel Plunge:

The iron ore recovery somewhat supported the ASX-listed iron ore miners; however, the weak steel demand and low prices exerted pressure on BlueScope Steel Limited (ASX: BSL), a steel manufacturer on ASX, and the share prices of the company dropped by 19.57% in the past three months.

BlueScope Steel Limited (ASX: BSL)

Latest Update:

In an announcement made public by the company on 18th June 2019, BSL mentioned that it expects the FY2019 underlying EBIT to approach $1,350 million, which in turn, mark an increase of 6 per cent from the previous corresponding period.

As per the company, the EBIT for the second half of the financial year 2019 is approaching $500 million. BSL also notified about the key changes in prior guidance provided by the company in February 2019.

The benchmark steel spreads of North Star prospect is now expected to decline by US$150 per tonne against its previous expectation of US$130 per tonne, which is lower than 1HFY2019; however, the company stated that the sales volume and operating performance of North Star remains strong.

BSLâs Building Products Asia and North America prospect is progressing well and reduced the manufacturing cost along with improvement program; however, the company highlighted that the market conditions have been softer than the estimation, particularly in ASEAN and North America.

BSLâs Building North America prospect is noticing general market conditions and order intake to be positive; however, despatch volumes and margins of the prospect is still getting impacted by longer customer lead times, as compared to the previous expectation.

BlueScope notified that other businesses of the company are performing in line with the February guidance, and the company is currently evaluating an opportunity to add a further 800,000 to 900,000 tonnes per annum of production capacity to its North Star mini-mill in the United States.

Buy-Back Extension:

BSL notified that amid a strong cash flow, the company would further extend the previous $250 million on market buyback program by another $250 million, as part of its 1HFY2020 capital management program.

The on-market buyback culmination date is further extended from the current 30th June 2019 to 31st December 2019.

The share price of the company nosedived over the increased price spread amid low steel prices, and ended the dayâs session at A$11.010, down by 1.167 per cent as compared to its previous close. The prices previously dropped from the level of A$11.840 (Dayâs high on 17th June 2019) to the level of A$11.120, a plunge of more than 6 per cent in a single trading day.

Iron ore Past and Present Scenario:

Iron ore prices are enjoying the leverage of shortfall in supply and the prices again made a new 52-week high on 14th June 2019. The inventory across 35 significant Chinese ports fell for the tenth consecutive week on 14th June. As per the data, the iron ore inventory across the Chinese ports declined by 2.89 million metric tonnes to stand at 109.55 million metric tonnes, down by 2.57 per cent as compared to the previous corresponding period.

The iron ore price climbed the level of RMB 797.50 (Dayâs high on 14th June 2019) before ending the session at RMB 787.50 on the Dalian Commodity Exchange.

After such a steep rise, the iron ore prices felt the pressure of weak demand from the steel industry, and the prices dropped significantly on 17th June 2019 at the Dalian Commodity Exchange (DCE). The prices of most active September contract (Iron Ore Futures), started the dayâs session at RMB 776.5, down by approx. 1.40 per cent.

Post starting the day below the previous close; the prices further plunged to register a low of RMB 760.5, down by more than 2 per cent in an intraday session, as compared to the opening price.

The substantial downfall in iron ore prices from its multi-year high pulled the ASX-listed iron ore miners down, and miners like Fortescue Metals (ASX: FMG), and BHP Billiton (ASX:BHP) started the dayâs session down by nearly 2.40 per cent and roughly 1 per cent respectively on 17th June 2019.

FMG and BHP further plunged during the dayâs session on 17th June to mark a low of A$8.400 and A$39.550, respectively.

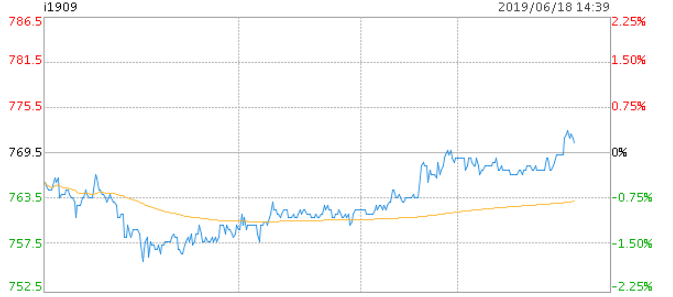

However, the shortfall in iron ore inventory again supported its price, and the commodity rose today on DCE. The iron ore futures on DCE started the dayâs session (18 June 2019) at RMB 766.5, down by approx. 0.39 per cent. Post starting the session below the previous closing the prices backed by short supply inched to mark a high of 773.0, up by 0.84 per cent from its opening.

Intraday Chart of DCIOU9 (Source: DCE)

ASX Jumpers:

Post seeing a pressure of correcting iron ore prices, the Aussie iron ore miners took the support from recovering iron ore prices and coupled with other factors traded either flat or surged on ASX today (18 June 2019).

After starting the session at A$8.350, down by more than 1.41 per cent, the shares of Fortescue Metals recovered sharply to the level of A$8.530 (Dayâs high on 18th June), and closed the trading day on a positive note at A$8.520, up by 0.49 per cent as compared to its positive close and up by more than 2.40 per cent as compared to its dayâs low of A$8.320.

The same recovery was shown by other iron ore miners such as Rio Tinto (ASX: RIO), and BHP (ASX:BHP) as well.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.