National Australia Bank Limited (ASX:NAB)

NAB has revealed half-year results for the period ended 31 March 2020. It has taken numerous actions to manage the risk of COVID-19. The banks had announced significant measures to provide relief to customers.

COVID-19 has materially impacted the first-half 20 results of the bank. Excluding large notable items, the bank’s cash earnings fell by 24.6% compared to 1H19 – this was due to higher impairment changes, mark-to-market losses on high quality liquids portfolio within Markets & Treasury.

It was reported that collective provisions now include $2.13 billion, and capital is being bolstered through a capital raise and reduced interim dividend. The bank has declared an interim dividend of 30 cents per share payable on 3 July 2020 to shareholders in records on 4 May 2020.

The bank has approved over 70k home loan and 34k business loan requests to defer repayments. Its business support scheme is providing $250k unsecured lending for 3 years.

Chairman and other directors of the bank have taken a 20% cut on their base fees. NAB CEO Ross McEwan has also taken 20% cut on fixed remuneration for the second half. Mr McEwan and his executive leadership team have decided to forego short-term variable rewards for FY20.

Operating performance

The bank’s revenues were down 3.4% against 1H19, and this was majorly due to the losses on its liquid portfolio in Markets & Treasury. Net interest margin was down 1 basis to 1.78% as against 1H19. A lower NIM was due to low interest rates which was offset by repricing in home lending portfolio.

Net interest income of the group was $6.88 billion and other operating income was $1.68 billion. Operating expenses for the period were $5.35 billion. Net profit attributable to owners of NAB was $1.31 billion compared to $2.69 billion in the previous corresponding period.

It was noted that the expenses for the period increased by 28.1% due to large notable items, higher investment spending, restructuring related costs – all these were offset by lower performance based compensation and productivity improvements.

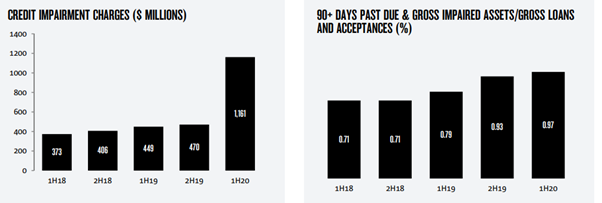

NAB credit impairment increased by 158.6% to $1.16 billion, which represents 38bps as a percentage of gross loans compared to 23bps in the previous corresponding period; this was primarily due to forward looking adjustments to reflect potential impact of COVID-19.

Source: NAB HY Results

It also witnessed an increase in delinquencies in the domestic mortgage portfolio, resulting in impaired assets to loans and acceptances ratio reaching 0.97% (gross 90 days past).

At the end of the period, the group’s CET1 ratio was 10.39%, up by 1bps from the September 2019. It includes 18 bps positive impact from the conversion of NAB capital notes into ordinary shares in March and 17 bps positive impact from the 2H19 dividend reinvestment plan.

NAB CET1 capital ratio was reduced by 21bps due to FX movement and losses on high quality liquids portfolio, and a 19 bps negative impact due to potential losses to COVID-19. Its leverage ratio for the period was 5.2%, liquidity coverage ratio was 136% (quarterly average), and net stable funding ratio of 116%.

Divisional Performance

This excludes large notable items and forward looking adjustments to account for the potential risks of COVID-19.

In Business & Private Banking, the bank generated an earnings of $1.37 billion down by 5.7% compared to 1H19. Although there was benefit with productivity gains, the earnings were impacted by lower returns on deposit and capital along higher investments.

In Consumer Banking, the division generated earnings of $699 million, showing an increase of 26.4% against 1H19. A higher revenue due to repricing with lower funding costs, and this was offset by competitive pressures. This segment also saw a lower credit impairment charges as a results of house price movements.

In Corporate & Institutional Banking, the earnings for the period were $701 million, down by 10.2% compared to 1H19. Lower income from the segment reflect subdued income from Markets, lower returns on deposits and capital and deteriorate lending margins. However, a higher lending volume and lower credit impairment provided some benefit.

In NZ Banking, the earnings were $562 million, up by 5.6% from 1H19. Although lower interest rates impacted the earnings, the segment saw lending growth and lower operating expenses.

Economic Outlook

It was said that that measures to curb the spread of virus resulted in an immediate negative impact to the economic activity. Policy measures would lower the impact on output and employment to some extent. Measures would also provide support when recovery is initiated, but when recovery would be sparks remains uncertain.

The bank expects GDP to be lower by over more than 8% by 3Q 2020 against 4Q 2019, and it expects recovery by early 2022. It anticipates unemployment to peak in mid-2020 at 11.2% and recovering to 7.3% by December 2021.

Capital Raising

NAB has launched capital raising seeking to raise $3.5 billion, comprising of an institutional placement of $3 billion (fully underwritten) and a share purchase plan of $500 million (non-underwritten).

The bank has taken proactive steps to build capital through capital raising and a reduction in interim dividend due to COVID-19 pandemic.

Capital preserving efforts of the bank would enable to continue delivering the services to the customers and navigating through a range of scenarios, including a prolonged economic downturn.

Post completion, the CET1 ratio of the bank would be 11.2% compared to 10.39% at the end of 31 March 2020. Placement is being undertaken at $14.15 per share, resulting in an issue of around 212 million new shares.

Under the Share Purchase Plan, Eligible shareholders who were on the book of the NAB on 24 April 2020 could apply for new shares up to $30k. It seeks to raise $500 million, and new shares under the plan will not be eligible to receive interim dividend of 30 cents per share.

On 28 April, NAB notified the market that institutional placement of $3 billion was completed under Placement. The bank has taken proactive steps to build capital through capital raising and a reduction in interim dividend due to COVID-19 pandemic.

Chairman & CEO letter

Philip Chronican, Chairman of the bank and Mr McEwan also wrote a letter to shareholders. They noted the immediate and deep impact on the economy and health of community, which they have not seen before.

They are working collectively with the government and regulators. In response to the pandemic, the bank had launched support for its customer by introducing a range of measures.

It was said that capital preserving resulted in lower dividends, but it is intended to strengthen the bank. They have developed a plan to take the bank in the next five to ten years.

On 28 April 2020, NAB was trading at $15.450, down by 1.967% (at AEST 1:40 PM).