_06_17_2026_00_06_46_079093.jpg)

On 24 July 2019, the prudential regulator of the Australian financial services industry, APRA has notified three Australian banks to tighten their intra-group funding arrangements, criticising them over breaching of the prudential liquidity standard. These banks include Macquarie Bank, Rabobank and HSBC. APRA intends to ensure that these sound banks can stand against financial stress scenario.

Besides, APRA expects these banks to restate their previous liquidity and funding ratios where these had been reported inaccurately.

Stronger requirements on remuneration

APRA has recently proposed a creation of new prudential standard (CPS 511) aimed at strengthening and clarifying remuneration requirements in the entities it regulates. The proposed reform forms a part of measures intended by APRA in response to the misconduct identified in the financial services industry by the banking royal commission.

APRA has proposed some key amendments for the Australian financial sector that will place the country in line with better international remuneration practice. The regulator released a discussion paper on Tuesday that suggested the following reforms to the remuneration framework:

Minimum Deferral Period for Bonuses

The regulator has proposed to introduce minimum deferral periods for variable remuneration of senior executives of up to seven years, while giving the company boards the power to recover remuneration for up to four years after they were paid out in cases where misconduct became apparent. This means that the bank executives in Australia might have to wait for up to seven years to get their bonuses.

Cap on Executive Bonuses

APRA has also suggested a cap on the proportion of executive bonuses in its proposed reforms. To put greater focus on the non-financial risks, the regulator has advised that the financial performance measures must not contain over 50% of the performance criteria for setting bonuses. According to the APRAâs Deputy Chair, Mr John Lonsdale, limiting the influence of financial performance measures in deciding bonuses will encourage the executives to put greater emphasis on culture and governance and other non-financial risks.

Enhance Accountability in the Financial Sector

The regulator intends to improve accountability in the financial sector by imposing stringent conditions on executive pay policies. To ensure individual and collective accountability, APRA wants the boards of Australian banks and other big financial institutions to actively oversee and approve the remuneration policies, regularly confirming that the policies are actually applied.

Mr Lonsdale mentioned in the discussion paper that the regulator has observed a lack of accountability and an over-emphasis on short-term financial performance at the time of failures, and this has undermined trust in the financial industry. He believed that CPS 511 will reduce the likelihood of misconduct and lift the industry standards of accountability by supporting the Banking Executive Accountability Regime.

Mr Lonsdale informed that the regulator will wait for the response from the impacted stakeholders to assess whether the APRAâs proposed approach is properly calibrated to attain its planned outcomes. A 3-month consultation period has been decided that will end on 23rd October and APRA intends to announce the final prudential standard prior to end of the current year.

APRAâs Capability Review

The Australian government published a capability review of the APRA after the regulator was criticised by commissioner Kenneth Hayne in a special inquiry into financial sector misconduct. The report highlighted that the regulator was reluctant to change, slow to act and lacked the âenforcement appetiteâ that was required to take on big companies.

The review made 24 recommendations that demanded a change in the APRAâs organisational structure and more transparency in its policies. The report criticised APRA for not acknowledging the disparities in the superannuation industry adequately and called for an alternative approach to supervision.

APRA has welcomed 19 recommendations out of 24 that were directed at it. According to the regulator, it is already working on many of these recommendations as a part of its current Corporate Plan.

APRA ensured that it will keep focussing on maintaining the financial system stability besides growing capability in other areas. The report acknowledged the steps already taken by APRA but emphasises the requirement to accelerate change if the regulator wants to retain its position as a successful prudential supervisor.

APRA Modifies Capital Requirements

Recently, the prudential regulator raised the capital requirements for big four banks of Australia, lifting the loss-absorbing capacity of the banks. The regulator declared that it wants the major banks to lift their capital requirements by 3 % points of risk-weighted assets (RWA) by 1st January 2024. However, APRA kept its overall long-term target of extra 4-5 percentage points of loss absorbing capacity as intact. The regulator also informed that it will consider the most viable alternative over the next four years for sourcing the remaining 1 to 2 percentage points. APRAâs move was focussed on minimising the risks of taxpayers and depositors in case Australia experiences a bank failure.

Impact of APRAâs move on Big Four Banks

The big four Australian banks responded to the APRAâs move and informed about the possible impacts on their businesses. The additional three percentage points represented an incremental increase of:

- $13 billion of total capital for Commonwealth Bank of Australia (ASX: CBA)

- $12.1 billion of total capital for National Australia Bank Limited (ASX: NAB)

- $13 billion of additional capital for Westpac Banking Corporation (ASX: WBC)

- $12 billion of total capital for Australia and New Zealand Banking Group Limited (ASX: ANZ), along with an equivalent fall in other senior funding.

APRA Imposes Additional Capital Requirements on Three Banks

Post announcing the amendments in the capital requirements for big four banks, the regulator asked three out of the big four banks â ANZ, Westpac and NAB â to increase their minimum capital requirements by $500 million each. The regulator forced the banks to keep aside the additional capital until they reimburse customers for wrongly charged fees and strengthen risk management. The order was given in response to the self-assessments conducted by the banks with regards to the management of non-financial risks.

The three Australian banks have provided information on the impact of APRAâs move through the Australian Stock Exchange recently:

National Australia Bank Limited: The bank stated that the additional $500 million of operational risk capital will be equal to an effect of 16 basis points on Common Equity Tier 1 in accordance with the bankâs 31st March 2019 capital position. NABâs risk weighted assets amounted to $403 billion as at 31 March 2019. Prior to APRAâs decision, the S&P Global Ratings revised its outlook for NAB from Negative to Stable.

Westpac Banking Corporation: Westpac reported that the $500m requirement will be implemented through a rise in RWA (risk weighted assets) and will be applied from 30 September 2019. The additional capital will reduce the bankâs Level 2 common equity tier 1 capital ratio (which was 10.64 per cent as at 31 March 2019) by around 16 basis points.

Australia and New Zealand Banking Group Limited: The $500 million of additional capital requirement will be equal to an effect of 18 basis points on ANZâs Common Equity Tier 1 capital ratio. ANZâs risk weighted assets amounted to $396 billion as at 31 March 2019. The bank reported that the increased capital requirement will be effective from 30 September 2019.

Fitch Ratings has revised the outlook for WBC and ANZâs Long-Term Issuer Default Rating from Stable to Negative post the APRAâs decision to apply additional operational-risk capital requirement on the banks.

The self-assessments of the three banks have reflected higher operational risk and demonstrated that they have fallen short in a number of areas. According to APRAâs Chair, Mr Wayne Byres, the major banks of Australia are financially sound and well-capitalised. However, there is a need to manage the non-financial risks by focusing on the root causes of the issues like unclear accountabilities, weak cultures, complexity, etc.

In May last year, APRA also applied a $1 billion additional capital requirement to Commonwealth Bank of Australia post identifying an inadequate oversight, an ineffective board and a complacent culture dismissive of regulators in the bank.

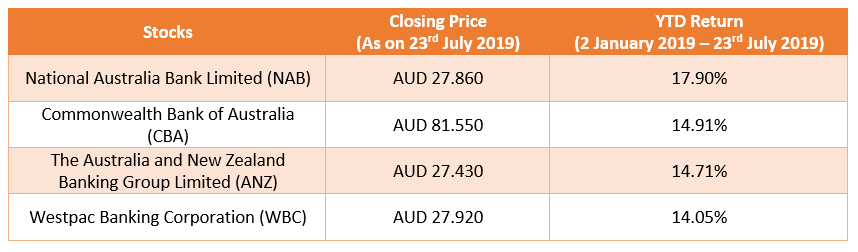

Let us now have a look at the big four Australian banksâ stock performance on a YTD basis:

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.