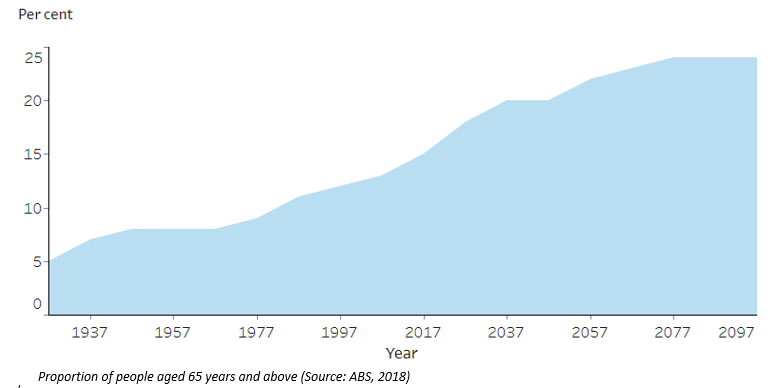

Evidence exists to show that proportion of older Australians is growing in the country with a growing demand for retirement safety and financial needs. As per official stats by Australian Institute of Health and Welfare, over 1 in 7 people or 15% of the total population of 3.8 million Australians were aged 65 and above in the country in 2017, which is further expected to grow steadily over coming decades. Increasing life expectancy can be partly attributed to the growing proportion of the Australian ageing population.

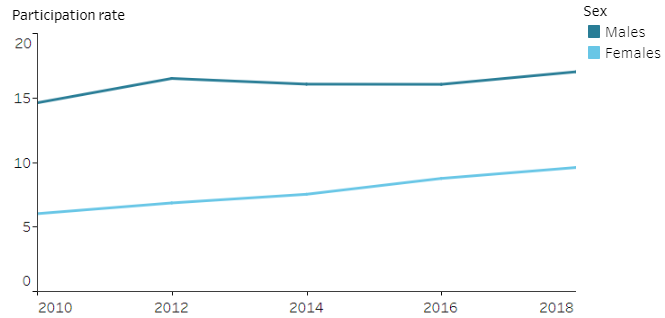

According to the government, 1 in 8 older Australians were employed in 2016. Further, data suggests that as on January 2018, people aged 65 years and above accounted for 13% of the countryâs total workforce. Besides, 17% and 10% workforce participation were reported for men and women, respectively.

Older Australianâs workforce participation (Source: ABS)

In Australia, retirees face savings challenges, as the market does not have many products that can offer them guaranteed income. Thus, annuities can be considered as the only guaranteed income product available to Australian retirees. Let us have a broader look at annuities.

Understanding Annuity:

An annuity is an insurance contract or policy, offered by financial institutions including investment companies and life insurance companies (regulated by APRA). Specifically designed for retirement, annuities guarantee a steady cash flow for retirees, in exchange of a lump sum payment or a series of regular payments made by the investor.

Annuities provider in Australia

Examples of some of the companies offering annuities in Australia include:

- Challenger Limited (ASX:CGF) is the largest annuity provider in Australia, offering a wide range of products such as lifetime and term annuities, superannuation products and several other aged care solutions. Challenger Life, regulated by APRA, offers guarantee to CGFâs annuities offerings.

- BT Financial Group, acquired by Westpac Banking Corporation (ASX:WBC), manages and offers managed investments, superannuation and retirement products, among other products.

Different types of annuity:

Fixed Annuity: Under a fixed annuity, a guaranteed amount including principal investment and earnings is paid for a fixed term period.

Lifetime Annuity: Unlike fixed annuity, Lifetime annuity has no fixed term, offering payments for the entire life. Some exceptional annuities offer access to the capital early, if required.

Immediate Annuity: This type of annuity is purchased with a lump sum payment and is ideal for a person approaching his/her retirement age, as there is no accumulation phase and the investor starts receiving payments immediately after the initial investment.

Variable Annuity: Unlike Fixed Annuity, the pay-out under this type of annuity varies, as it depends on the investment made and rate of return on the investment.

Deferred Annuity: In this type of annuity, payments are made after a certain period.

Why people opt for annuities?

Annuities are preferred by the people, who consider these as their primary income source after retirement. They can be compared with other retirement income strategies like pension products, bank deposits or other investment strategies resulting in a fixed income. People prefer annuities, as they:

- Give a secured guaranteed return (in case of fixed annuities) for very long term, regardless of financial market fluctuations.

- Offer higher earning rates than other alternatives to fixed income like government bonds and bank deposits.

- Give income to the beneficiary, in case the person who purchased annuity dies, thus serving the future financial needs of the loved ones.

- Has both taxable and tax-free components. In Australia, income received under annuities is tax-free, if the buyer purchases it with superannuation money and meets the minimum income payment requirements. Moreover, the buyer needs to be 60 years old or over. Annuities purchased by a buyer less than 60 years old will be subject to the marginal tax rate, with a 15% offset. For annuities purchased with non-super money, only the income component is subject to taxation.

- Removes the worry of out-living savings, in case of a lifetime annuity.

- Do not carry product fees, as the fees are incorporated into the annuity rates offered.

Disadvantages of annuities:

Major disadvantages of investing in annuities have been listed below:

- The money is locked, that means a limited or no access to lump sum money for a long period of time. Some annuities offer access to money subject to conditions.

- People have no right over where the fund goes. The fund manager decides where to invest the money.

- Number of companies offering lifetime annuities is low in Australia, perhaps reflecting lesser competition in terms of price and features.

- Issues in transferring annuity money to another pension product.

- Annuities may give lower returns than a market-linked investment, in long term.

Impact on Age Pension entitlement:

In Australia, nearly 65% of elderly people depend on a government pension or allowance as their source income after retiring. Thus, Age Pension is an important income source for retirees in the country. An income test and an assets test determine the Age Pension in Australia. Any person opting for annuities can check with the Department of Human Services' Financial Information Service (FIS) regarding its impact on the Age Pension entitlement.

What an investor needs to know before opting for annuities?

- Investors need to ensure that the annuity provider is well-rated and regulated, as annuitants have credit risk on the insurer. The Australian Prudential Regulation Authority regulates life insurers in the country. The agency is responsible for ensuring that the insurers are well capitalised and have enough liquid assets to meet expected annuity and death benefit pay-outs.

- Investor should have a clear idea about what type of returns he/she expects with an annuity, and accordingly undertake the appropriate choice regarding the type of annuity to invest in.

- Income payments can be received on a monthly, quarterly, half-yearly or yearly basis.

- In case the investor dies, the nominated beneficiary is eligible to receive the income payments, however, the income received may be lower than what the investor had received.

- Inflation impact: inflation has an impact on every fixed income product. The investor can choose an inflation?adjusted annuity, if he/she is concerned regarding the inflation impact on the annuity income.

Superannuation aspects and changes expected from 1st July 2019

In Australia, superannuation is an arrangement, under which the government encourages people to place a minimum percentage of their income during their working life into a fund to ensure an income stream after their retirement. The superannuation fund invests money in shares, property and managed funds, etc. In 2016-17, nearly 65% of people aged 45 or above who had retired had made contributions to a superannuation scheme.

The Australian Institute of Superannuation Trustees (AIST) is the representative body for the profit-to-members superannuation sector worth A$1.3 trillion in Australia. The organisation plays a major role in policy development. AISTâs members include trustee directors, in addition to employees from industry, corporate and public-sector funds. AIST is the host of several industry conferences and events, along with the Conference of Major Superannuation Funds (CMSF).

In February 2019, reforms that were proposed in the budget for 2018 became law. The reforms are aimed at safeguarding the superannuation savings of Australians from erosion, owing to unsuitable fees and insurance premiums as well as cut unintended multiple low balance accounts, as it is a major issue for most of the Australians.

The reforms were introduced after a report found that approximately 10 million or one third of all superannuation accounts are unintended duplicate accounts and can erode member benefits by up to A$2.6 billion in unnecessary fees and insurance, annually.

The amendments will encourage the consolidation of multiple low-balance superannuation accounts. The reforms are estimated to proactively consolidate about 3 million accounts worth approximately A$6 billion, according to the organisation. The changes set to come into effect from 1st July 2019 are:

- Inactive super accounts for the last 16 months will be closed. Any account that has not received any contributions into the super account for more than 16 months is considered as inactive.

- The changes mean that inactive accounts with a balance less than A$6,000 will be cancelled. The Australian Tax Office will receive the balance amount, as the account will get transferred to the office, which will also close any other insurance attached with that member.

- Fund members will get a fee cap imposed on certain fees for account balances less than A$6,000.

- Fund members will not be required to pay exit fees for shifting money from a superannuation account.

In order to ensure proper implementation of the reforms, the organisation is working closely with the Australian Prudential Regulation Authority and the Australian Tax Office.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.