In our report from the 100 years of the Australian Share Market and based on the extensive research report laid down by the Reserve Bank of Australia, major banks account for a large share of the Aussie economyâs output and employment. Banks in Australia have undergone mergers and grown over time. Even though the banking stocks underperformed for a few decades post the Great Depression (from 1929 to 1939), it is an interesting find that the financial corporations, and banks, in particular have accounted for over half of the Australian market in terms of market capitalisation. Whatâs interesting is the fact that this statement has remained intact and true for a century.

Banking Sector and its Impact:

The section of a countryâs economy, which focusses on the financial assets to contribute towards creation of wealth, while undertaking regulatory activities in sync with the government, is the banking sector.

In simple terminology, banking is described as a process and full-fledged business activity, wherein money owned by other individuals and entities is not only accepted and protected, but eventually lent for the purpose of earning a profit. With evolving times, the banking business has expanded with a hoard of products and services on the offer. Cards, lockers, ATM services and virtual banking have been a part of the evolution of banking.

Banking is amongst the most vital factors driving an economy and contributing towards its growth, as it encourages the flow of money in the direction of productive use and investments. Banking aids businesses, entrepreneurs and individuals to facilitate their financial transactions and forms an everyday part of their lives, without which the economy would cease to function effectively and efficiently. The impact of banking deepens as it is one of the catalysts that drives international trade relations between the economies.

Around the world, the popular players in the banking space include of; Wells Fargo, JP Morgan Chase and HSBC Holdings.

Banking Sector in Australia:

Australia has a contemporary, competitive and profitable financial structure with a strong regulatory system governing the banking space. The banking sector is a large part of the Australian market. Some of the biggest names in the Australian Banking space include-Commonwealth Bank of Australia (ASX: CBA), Westpac Banking Corporation (ASX: WBC), National Australia Bank Limited (ASX: NAB), and Australia and New Zealand Banking Group Limited (ASX: ANZ).

In the recent times, the Aussie banking space has been in the limelight due to the Banking Royal Commission, RBA interest rate cuts and the housing bubble bursting. With the Banking Royal Commission in action, market experts believe that there would be positive systematic change in the countryâs banking landscape.

Bank Fees in Australia:

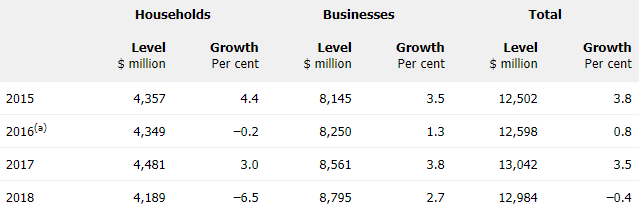

Based on a survey undertaken by the RBA, banksâ overall income from fees was tweaked a bit in 2018. A number of banks removed the ATM withdrawal fees, reducing the total fees charged to households, which accounts for approximately one-third of the banksâ fee income. The remainder, which is the fee income from small businesses continued to rise, depicting a significant increase in the transactions done via credit card and debit card.

Banks' Fee Income (Source: RBA)

Elaborating the tweak, reflecting a submissive growth in lending assets and deposits, the ratios of fees to assets and deposits remained flat in 2018. After depicting a growth profile in the recent years, the bank fees charged to households decreased by 7 per cent in 2018, driven by the significant decrease in fee income from household deposits and the decline of the housing loans.

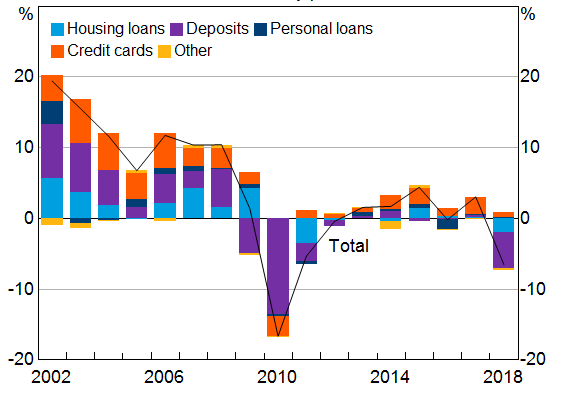

Growth in Household Fee Income (Source: RBA)

The Fee income from credit cards grew at a comparatively slower pace. Coming to the Fee income from deposit accounts, these slumped by 20 per cent, driven by the abolishment of ATM withdrawal fees. It should be noted here that of late, consumers in Australia have been inclined towards the usage of electronic payment modes and payment cards. Income from exception fees on transaction deposit also deteriorated.

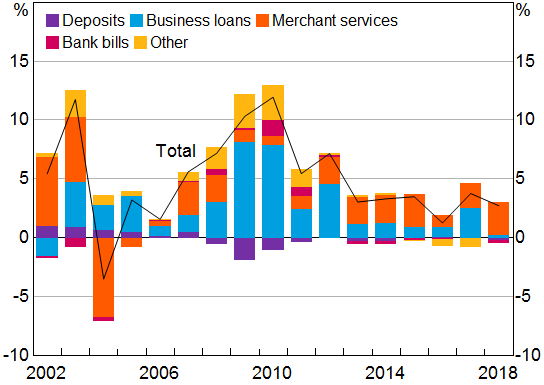

From the small business perspective, the Total fee income from businesses increased by 3 per cent in 2018, with a growth in income from merchant service fees on card transactions. The fees charged on the business loans also witnessed a fair increment though the fees from deposit services and bank bills went down. Merchant service fee income continued to grow at a sturdy pace.

Growth in Business fee income, by product (Source: RBA)

In the backdrop of this context, let us look at a rousing update and the performance of the top four banking stocks of the Aussie land, on the Australian Securities Exchange:

Recent Fitch Ratings placed WBC and ANZ in the âNegativeâ zone:

Regarded amongst one of the âBig Three credit rating agenciesâ along with the Standard & Poor and Moodyâs, Fitch Ratings Inc. is a renowned credit rating agency, headquartered in New York. On 17 July 2019, the agency created a buzz in the Australian banking space, when it revised its ratings of two major Aussie banks, who are looked upon as peers in the country- Westpac and Australia and New Zealand Banking Group. The revised rating moved the standing of these two banks from âstableâ to ânegativeâ with ratings at âAA- â.

This depicts Fitchâs increased focus on compliance measures and taking charge of operational concerns. It should be noted here that last year, other two major banks- NAB and CBA had been placed on the negative rating side, on the same account of a negative outlook.

This was announced post APRAâs order to three major Aussie banks to each set aside a further A$500 million as a requisite capital, until the risk management was made robust and the reimbursement took place for the wrongly charged fees to customers.

It can be stated that moves like this showcase a strictness in the economy towards any complexity, lack of accountability and bureaucracy.

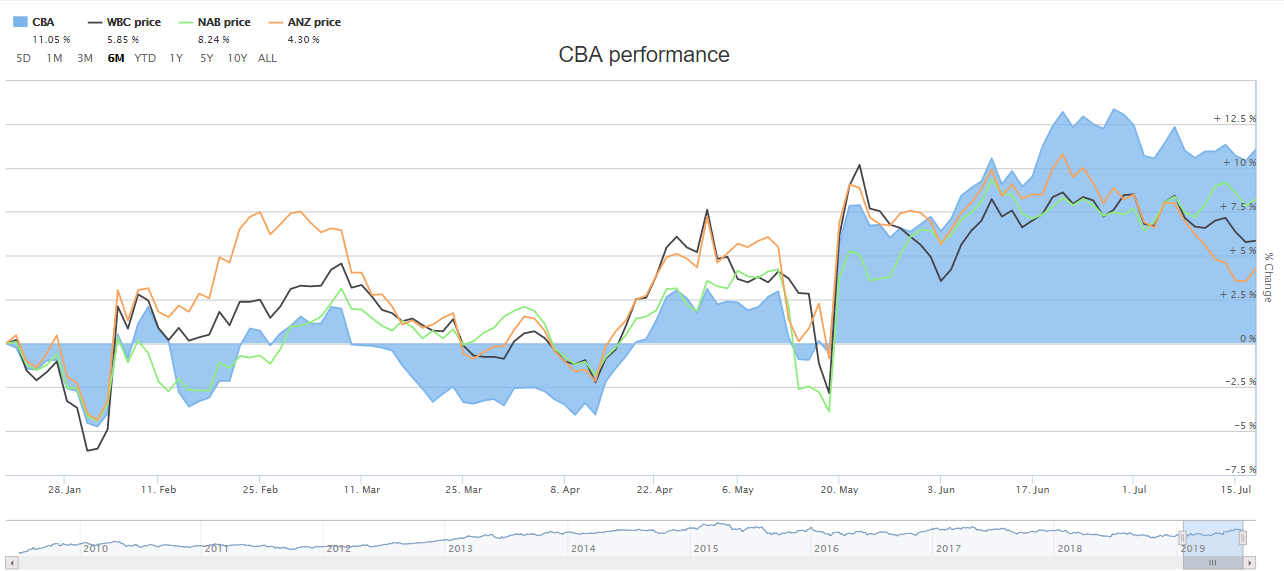

On the trading side, below is the performance of these big banks on the ASX:

The below graph depicts the 6-month returns that CBA, WBC, NAB and ANZ have generated, as on 18 July 2019. Surprisingly and interestingly, it can be noticed that all these major players have shown a similar trend while generating their respective returns and have risen and nose-dived almost simultaneously.

Commonwealth Bank of Australia (ASX: CBA):

Post the close of business on 18 July 2019, the stock of CBA was valued at A$81.380, marginally up by 0.074 per cent relative to its last trade, with approximately 1.77 billion outstanding shares. The company has a market capitalisation of A$143.96 billion and an annual dividend yield of 5.3 per cent. In the last one, three and six months, the stock has generated returns of 1.41 per cent, 10.96 per cent and 11.75 per cent, respectively, with a YTD return of 14.58 per cent.

Westpac Banking Corporation (ASX: WBC)

On 18 July 2019, the stock of WBC closed at A$27.580, down by 0.361 per cent, relative to its last trade, with ~3.49 billion shares and with a market capitalisation of A$96.6 billion. The companyâs annual dividend yield is 6.79 per cent and in the last three and six months, WBCâs stock has generated returns of 3.25 per cent and 6.18 per cent, respectively, with a YTD return of 13.07 per cent.

National Australia Bank Limited (ASX: NAB)

The stock of NAB was at a price of A$26.920, down by 0.07 per cent with ~2.88 billion outstanding shares and with a market cap of A$77.67 billion on 18 July 2019. The annual dividend yield of the stock is 6.76 per cent and in the last one and six months, it has delivered returns of 1.05 per cent and 8.59 per cent, respectively. The YTD return of the stock is 14.01 per cent.

Australia and New Zealand Banking Group Limited (ASX: ANZ)

Another major bank of the Aussie land, ANZâs stock closed at A$A$27.120, down by 0.257 per cent on 18 July 2018. The market cap of the company is A$77.07 billion and it had ~2.83 outstanding shares. The stock has an annual dividend yield of 5.88 per cent and has generated a YTD return of 13.96 per cent.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.