In this article, we would discuss two large companies from the Energy sector in Australia. Accordingly, Caltex Australia & WorleyParsons Limited are the constituents of the Australian benchmark index S&P/ASX 200, which by the closure of the trading session, was at 6724.6, up by 36.4 points from the previous close (as on 23 July 2019). Concurrently, the S&P/ASX 200 Energy (Sector) was at 10,834.90, up by 144.80 points from the previous close.

Caltex Australia (ASX: CTX)

Caltex Australia (ASX: CTX) is a large-cap energy sector related company based in Australia. The stock of the company is a constituent of S&P/ASX 50, S&P/ASX 100, S&P/ASX 200, S&P/ASX Dividend Opportunities Index, S&P/ASX 200 Energy (Sector) and a few more indices.

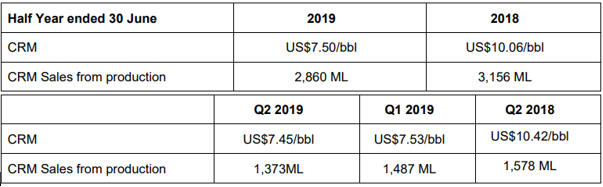

On 23 July 2019, Caltex Australia reported a Caltex Refiner Margin (CRM) update for the period ended three months to June 2019 (Q2 2019). Accordingly, CRM depicts the variation between the cost of importing Caltexâs products to eastern Australia and the cost of importing crude oil needed to manufacture Caltexâs products. Also, CRM is converted to AUD terms using the prevailing FX rates, and it is one of the components to the EBIT earnings of the Lytton refinery â fuel & infrastructure division (as notified on 20 June 2019).

The current announcement suggests that the Q2 2019 CRM was of US$7.45/bbl, which is down from the preceding quarter CRM of US$7.53/bbl in Q1 2019, and below the prior corresponding period CRM of US$10.42/bbl in Q2 2018. In addition, the average CRM was US$7.50/bbl, while CRM sales from the production were reported at 2,860 ML.

CRM & Sales (Source: Companyâs Announcement)

Credit Rating

In an announcement dated 25 June 2019, Caltex reported that the global rating agency S&P Global Ratings had reaffirmed BBB+ long term issuer rating for Caltex following the lowered profit guidance. Also, the outlook of the company has been revised from stable to negative; this is due to the challenging industry conditions, particularly the convenience retail business. Recently, the company has asserted to place a strong emphasis on cost reduction, optimising returns and capital efficiency, including the convenience retail business. Besides, it believes that achieving these priorities would ensure a strong balance sheet position.

Half-Year Profit Guidance

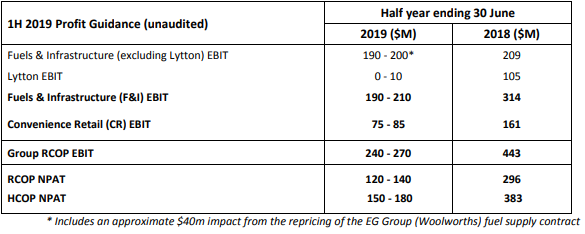

Previously, Caltex Australia had released half-year profit guidance (unaudited) for the period ended 30 June 2019 on 20 June 2019.

Market Conditions

The announcement suggested that the first half of the year presented escalated domestic challenges in the industry. Also, these challenges were driven by weak domestic activity in areas including transport, agriculture, and construction sectors. Besides, the sales volumes and margins were impacted by the combination of high crude price and lower external refiner margin.

Fuels & Infrastructure (F&I)

Reportedly, the company had expected the EBIT in between $190 to $210 million for the first-half 2019 down from $314 million in the previous corresponding period. Also, it expects an EBIT in between $190 to $200 million, excluding the Lytton.

Admittedly, EBIT from Lytton refinery is anticipated to be in the range of zero to $10 million in the first half of 2019, which would be down from $105 million in first-half 2018. Besides, this has been impacted by the CRMs, while the first-half 2019 sales from production were expected of 2.9BL, and the guidance on the full-year outlook remains unchanged at around 5.8BL.

Unaudited Profit Guidance (Source: Companyâs Announcement)

Sales Volume

As per the release, the total fuel sales volumes are expected to be around 9.7BL in the first half of 2019, which is about 5% lower from 10.2BL in the previous corresponding period. Also, the domestic sales volume in Australia are expected to reach 8.2BL in the 1H 2019, approximately 2% below from the 8.4BL in the previous corresponding period. Besides, the international volumes are anticipated at ~1.5BL in first-half 2019, ~15% down than the 1.8BL in first-half 2018.

Convenience Retail (CR)

Reportedly, the division is anticipated to deliver an EBIT in the range of $75 to $85 million in first-half 2019, which was down by about 50% from $161 million in the previous corresponding period. Also, the total volume sales in the division are expected to be ~2.4 BL in first-half 2018, which would be 1-2% down from the volume in the previous corresponding period.

Other Items

Caltex has anticipated corporate costs to be at $25 million for first half of 2019 down from $31 million in the previous corresponding period. Admittedly, the net debt of the company as on 30 June 2019 would be around $1,200 million; this depicts an increase from $955 million as on 31 December 2018 due to an off market buy back (OMBB) of $260 million. Besides, the company is expecting interest payments to be of about $65 million in first-half 2019, which would be up from $27 million in the first-half 2018; this represents the inclusion of $30 million of lease interest expense post incorporating AASB16.

On 23 July 2019, CTX stock last traded at A$25.97, up by 0.232% from the previous close. The stock over the past one-year has given a negative return of 15.68%. Besides, the stock has returned +7.47% over the past one month.

WorleyParsons Limited (ASX: WOR)

WorleyParsons Limited (ASX:WOR) is engaged in the business of professional project and asset services in the energy, resource and chemical sector. Besides, the stock of the company is a constituent of S&P/ASX 100, S&P/ASX 200, S&P/ASX MIDCAP 50, S&P/ASX 200 Energy (Sector) and few more indices.

On 25 June 2019, WOR reported the change of interests in a regulatory filing to the exchange. It was notified that Jacobs Engineering Group Inc., a substantial holder of the company, effective 24 June 2019, had reduced its interests in WOR to 9.90% from 11.20% in terms of earlier voting power.

On 5 June 2019, the company released its Investor Day Presentation for 2019. The presentation contained the following details:

Companyâs Focus

Accordingly, the companyâs focus remains in integrating the operations while delivering the cost, revenue synergies consistent with existing strategic priorities; therefore, the cost synergy target was increased from AUD130 million to AUD150 million. Besides, the company intends to develop a new transformational strategy that would improve the leadership position in chemicals & petrochemicals, capture the opportunities presented by the global energy transition and change the way WorleyParsons work through leveraging automation as well as the use of digital products.

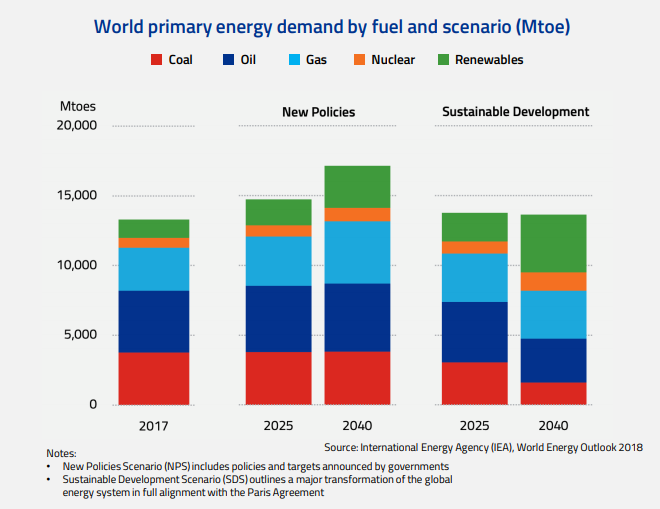

Global Energy Transition

Reportedly, the company anticipates the changes in the global energy mix, but it is also uncertain regarding the pace of change in the energy mix and believes changes in energy mix would be idiosyncratic to different countries. Also, the oil and gas are expected to increase annual sanctioned investments through to 2025. Besides, WorleyParsons anticipates the opportunities would underpin the energy transition across all of the four sectors it operates.

Global Energy Demand (Source: Companyâs Investor Day 2019 presentation, June 2019)

Energy Transition: Downstream & chemicals

Reportedly, the major changes in the composition of oil product demand are presenting challenges for refiners including fall in demand for gasoline and diesel, demand for lighter feedstock supply, the increased proportion for chemical feedstock, decreased yields for residues and adhering to IMO 2020 regulations. Besides, WorleyParsons believes that it is well positioned with the customers, geographic diversity and leading desulphurization technologies.

According to GlobalData Oil and Gas (May 2019), the changes are driving investment in upgrades and brownfield projects with CAPEX investment expecting 5.5% CAGR to 2022.

On 23 July 2019, WORâs stock last traded at A$15.09, up by 1.891% from the previous close. Over the past one-year, the return of the stock has been -11.77%. Besides, the year-to-date return of the stock has been +30.60%.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.