Fortescue Metals Group Limited (ASX:FMG) shares are under pressure on 28 January 2020, and down by over 7% on ASX. The shares are hammered over the fears of coronavirus in China.

However, up until now, the FMG shares were on strong bull run shattering multi-year records over demand rush for iron ore in China. The stock is trading around its decade high and is within a few percentage points from its previous peak value of $13.150 (high in June 2008).

The surge in the company share prices placed Andrew Forrest on track to gain the title of Australia’s richest man, combined with other investments his net worth totals close to $15.9 billion neck and neck with the cardboard behemoth- Anthony Pratt, albeit todays negative price action could rejigger this ranking.

The towering iron ore price is now placing Andrew Forrest, who stood at the number seven spot in Forbes Australia rich in 2019 sharing podium with the mining mogul Gina Rinehart of Hancock Prospecting.

The competition ahead would be tough as the surge in iron ore price would just not make Andrew Forrest rich, it would also push the net worth of Gina Rinehart further.

Iron ore prices have witnessed a spark from the December 2015 low of USD 39.00 per tonne to USD 120.02 per tonne in July 2019, which underpins a price appreciation of ~ 208 per cent. The current demand and supply situation in iron ore market across the globe is keeping the iron ore rally alive and kicking, and at present, the commodity is changing hands above USD 90.0 a tonne on the Chicago Mercantile Exchange (or CME).

To Know More, Do Read: Iron Ore Gushes as Tropical Cyclone-Blake Raises Supply Concern

The gush in iron ore prices is not just pulling Fortescue, other iron ore mining companies on ASX such as Rio Tinto Limited (ASX:RIO), and BHP Limited (ASX:BHP) are managing to surpass multi-year highs with ease.

Rio Tinto rallied from its recent low of $82.420 (low in August 2019) to the present high of $107.790 (intraday high on 22 January 2020), which underpinned a price appreciation of ~30.78 per cent. The recent rally in iron ore prices had brought the stock near to its May 2005 peak price of $124.186.

Likewise, BHP is under rally from its recent low of $34.420 (low in August 2019) to the present high of $41.470 (intraday high on 22 January 2020), which marked a price gain of ~20.48 per cent.

While top iron ore gunners are inking new highs on ASX, many junior miners are also gaining momentum from the rise in iron ore prices.

For example, Mount Gibson Limited (ASX:MGX) a small cap iron ore miner recovered from its recent low of $0.640 (low in September 2019) to the present high of $1.025 (intraday high on 21 January 2020), a gain of ~60.15 per cent.

However, while hopes of riches are high with their respective holdings and from iron ore, many independent forecasters anticipate the iron ore to average low in the coming years as the supply restores.

To Know More, Do Read: Mid-Year Budget Lowers Iron Ore Price Forecast; Emerging High-Yielding Dividend Opportunity?

DIIS’ Forecast on Iron ore

The Department of Industry, Innovation and Science (or DIIS) estimates the average price in 2019 to be USD 80 tonne on Free-on-Board (or FOB) basis, which is further anticipated to average USD 60 a tonne by 2021.

The projected export earnings of $84 billion in 2019-20 are also estimated to decline to stand at $66 billion in 2020-21 over the decline in iron ore price.

However, the DIIS also estimates the export volume to grow substantially from 834 million tonnes in 2019 to 878 million tonnes in 2021, which would mark a rise of ~ 5.27 per cent.

While the majority of the decline in iron ore prices are estimated on account of the revival in supply, Australian mining could still be in profit and support the purses of top riches, subject to the demand and global economic scenario.

Demand for Iron Ore

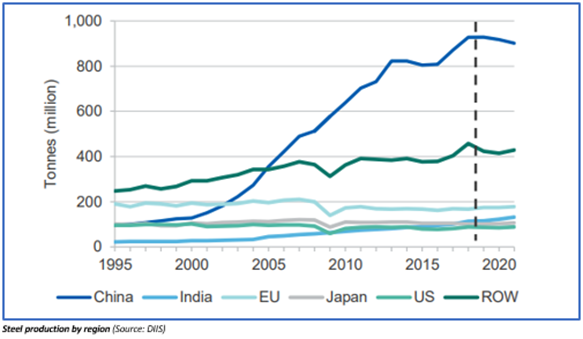

Iron ore is the basic material for steel production, and China is the top producer, which in turn, makes China, the primary consumer of the Australian iron ore supply. This explains today’s bearish trade set up for the ASX listed mining companies, with the index -S&P/ASX 300 Metals and Mining down 3 per cent as against -1.36 per cent marked by the benchmark index S&P/ASX 200.

Steel production from China and across the globe is projected by DIIS to grow substantially in 2021 before cooling-off slightly in 2022.

China is also supporting the steel demand through its development push related to infrastructure such as of power grid, and while the bilateral dispute of the red dragons with the United States has waned slightly, China is further expected to again push for the infrastructure development.

The impact of the bilateral trade deal between the United States and China makes it a potential risk, as well as, a decisive factor in deriving the iron ore price ahead.

Steel demand is highly correlated with the demand, which further moves in tandem with the global economic conditions. The global economic conditions are recovering so far tentatively; however, the recent forecast by the International Monetary Fund (or IMF) is not very encouraging for 2020, which is another risk factor for Andrew Forrest in reaching the number one spot of the Australian top rich list.

We must closely watch how the coronavirus situation pans out in China and how efficiently the Chinese authorities are able to thaw the epidemic threat.

To Know More, Do Read: IMF Downgrades Global Growth Forecast to 3.3 per cent for 2020