The health care system in Australia is comprehensive and comprises two parts: public health care and private health care. The system offers inexpensive and secure health care to its citizens.

The federal government, state government, and the local government run the health care system together. The system allows its residents to choose the system of their choice and also select their own doctor/specialist and health insurance provider.

The public health care system includes public hospitals, health organizations (owned by state and territory government) and community-based services. Under the Medicare system, a component of the public system, the Australian government offers health care services to all of its citizens and permanent residents. Through Medicare, the public can get access to proper health care at a reasonable price or even free of cost in some instances. Medicare’s expenses are funded by the tax collected by the government.

The private health care system comprises privately-owned health care services providers, including private hospitals, pharmacies, and specialist medical health. Private health care services are supported by both the government and private entities.

In this article, we will throw some light on the private health care system in Australia.

Why is private health care important?

While the public health system is for the citizens and permanent residents, the Australian government urges the public to buy private health insurance as well. The primary reason behind this is the fact that the public health system does not cover all the aspects of the services.

The patients using public health services might have to join a waiting list before getting the necessary treatment, may not have the option of selecting the doctor and/or the hospital of his/her choice. Also, the public health system does not cover vision, long-term, and dental care. It also excludes private patient hospital costs, ambulance services and medical costs incurred abroad.

Though private health insurance is not mandatory, it helps lessen the burden on the public health system and at present, ~50% of the public purchases private health insurance.

How does the private health care insurance function?

The insurance cover has three parts: hospital cover, general treatment cover and ambulance cover. Unlike typical insurance, private health insurance cover is not ‘risk-rated’ but is ‘community-rated’. This means that the private health insurers must insure an individual who approaches them, and they will have to charge the same premium for the same cover irrespective of the individual’s risk profile.

Hospital Cover: An individual can opt for a doctor of his/her choice through hospital cover and has the option of choosing whether to get treated in a private or a public hospital. While an individual in a private hospital can avail more facilities, an individual in a public hospital will still have to GO through the waiting list, if any.

In general, the medical services covered under Medicare and that fall under the Medicare Benefits Schedule (MBS) can be covered by the private hospital insurance as well. Cosmetic or laser eye surgery does not fall under MBS coverage but can be covered, to a limited extent, by the private hospital insurance.

Different insurers provide different policies with the more expensive ones providing a broader range of services compared to the less expensive ones.

General Treatment Cover: Also known as ancillary cover or extras cover, the general treatment cover offers insurance, either partial or full, against treatment by ancillary health service providers. The services include home nursing, dental treatment, physiotherapy, contact lenses/glasses, and prostheses, among others.

Ambulance Cover: An individual who purchases private insurance can get cover for ambulance service in the form of hospital cover, general treatment cover or any other kind of cover.

Broader Health Cover: A broad array of clinically suitable substitutes to hospital treatment can also be covered by private health insurers. Treatment provided in ones’ home or chronic disease prevention programs form a part of such services. Health insurers are not obligated to provide such services which include wound care, diabetes management, and intravenous therapy, among others.

Current scenario in the Australian private health care system

In a report published recently, it has been predicted that unless the reforms are made, the Australian population covered by private health insurance will be lower than 40%.

It is believed that deregulating premiums so that insurers can charge older people higher than younger people for the same coverage level can help keep the private insurance attractive.

Due to the same premium being charged for a coverage or plan, it has been observed that several younger people have been moving away from the private health care system.

Some specialists indicate that the system faces a death spiral where the young and healthy population is exiting the system due to high premiums leading the insurers to raise the premiums to negate the loss of losing customers. This, in turn, leads to more people moving out of the system.

Some have suggested that one way to tackle the current situation is to transmit the private hospital insurance rebate in the direction of older patients. Another suggestion is that instead of increasing the rebate, it should be removed from low-coverage policies. Dental care should be funded by some of the proceeds while the rest should help keep the premiums for older people at a reasonable level.

According to the Australian Prudential Regulation Authority (APRA), insurers need to toughen up and build strong strategies to deal with the challenges of an ageing population.

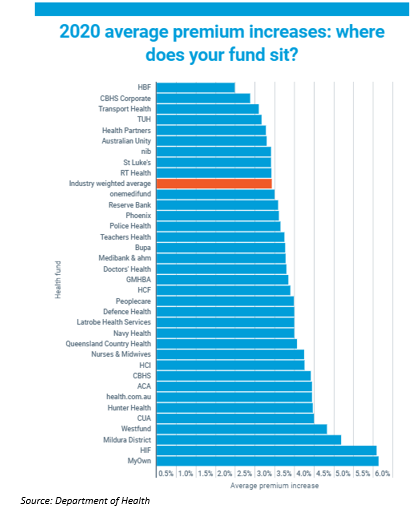

In addition to the challenges mentioned above, Australia’s health minister Mr Greg Hunt recently announced that effective 1 April 2020, private health insurance premiums would increase, on an average, by 2.92%. While this is the lowest increment since 2001, it is significantly higher than the rate of inflation.

Even though the premium increase compared to inflation in the health care sector, is on the lower side, the increase in price will likely be higher than inflation rate by 72%. Looking at the scenario, some have suggested that the government needs to run an enquiry with respect to private health care insurance and take preventive actions.

While the health care sector in Australia is said to be one of the best systems in the world, it is coping up with its own internal challenges. With growing uncertainty around the private health care insurance system, there’s a lot to be done to make the system in favour of people and insurers.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.