The Australian banks are set to see a deteriorating loan book and loss of earnings is visible because of COVID-19 induced recession on the horizon, since banks are incurring substantial credit impairment charges to account potential losses.

Investors must consider structural changes that can arise for the banks in future rather than only looking at the daily share price movements.

When the world has gone online to work from home amid lockdowns, the popularity of neobanks that use digital services and world-class technology is rising ahead. With neobanks coming into the picture, a shift can be seen away from the Big 4 to a more decentralised banking system, however, Big 4 banks have substantial digital abilities.

The bank shares on ASX are still in a good position, churning out profits. However, risks of bad debt are looming amid the slowing economy.

Here is a look at two of the Australian banks and their financial position-

National Australia Bank Limited

As per its latest update, National Australia Bank Limited (ASX: NAB) has slashed its interim dividend and has endorsed a capital raising of $3.5 billion indicating the disastrous effect of COVID-19 on the bank. It further notified that it concluded a $3 billion Placement. As per the Placement, the bank would be issuing ~212 Placement shares at a price of $14.5/Placement Share.

NAB reduced its interim dividend to 30 cents per share, along with bolstering capital through new funding to provide the bank with sufficient capacity to operate amid a weak economy.

Coronavirus has affected its first half-year results for this year, for the period ending 31 March, materially with the cash earnings falling by 24.6% excluding large notable items compared to 1H19 due to high impairment charges and loss on liquidity (announced on 27 April). The bank entered into the crisis period in a robust position with substantial capital, liquidity and funding, and it has taken proactive steps to strengthen its balance sheet.

Bank officials, including the Chairman, have taken a 20% pay cut in their fees. Ross McEwan NAB’s CEO has himself taken a 20% cut on the fixed remuneration for the 2nd half of 2020. The group’s CEO and leadership team also opted on foregoing all short-term rewards for FY20.

NAB has approved about 6-month loan deferrals on 70,000 home loans with balances worth $26.5 billion. All small and medium businesses, to which NAB is the largest lender, are noticing their incomes drying up.

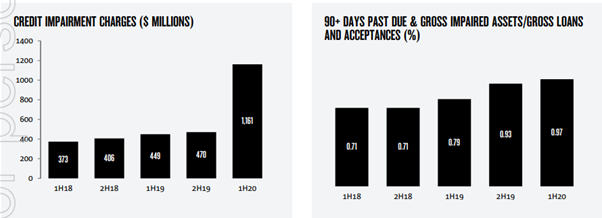

The bank’s revenue decreased 3.4% compared to 1H19 due to losses in liquidity portfolio in the markets and Treasury. Though, the credit impairment charges have soared up by158.6% to $1.16 billion that are indicative of 38bps as a percentage of gross loans and acceptances as compared to 23 bps in the previous period. The increase in charges was due to additional collective provision of $828 million forward-looking adjustments to reflect COVID-19 influence.

Source: NAB’s 2020 half-year report

The ratio of 90+ days past due and gross impaired assets to gross loans and acceptance rose 18bps to 0.97% due to increased delinquencies across Australian mortgage portfolio.

ALSO READ: ACCC Unveils- Big Four Banks Did not Fully Pass Lower Rates to Mortgage Customers

NAB has stated that given the current economic fallout arising from COVID-19, the underlying asset quality stays sound, but the stance is ambiguous. Hence, there is an extra forward-looking economic adjustment of $807 million among collective provisions for the COVID-19 impact in 1H20.

Also, the bank has been the first to declare dividend since APRA’s guidance on dividend suspension until COVID-19. It is augmenting its capital through lower interim dividend and significant new funding which are also good indicators of what can come from other banks.

Further on 30 April, NAB notified that one of its directors Ann Caroline Sherry, has changed her interest effective 29 April. The director acquired 3.5k ordinary shares at a value of $56.594.98.

On 30 April 2020, NAB last traded at $16.960, up by 4.113% from its previous close.

Australia and New Zealand Banking Group Limited

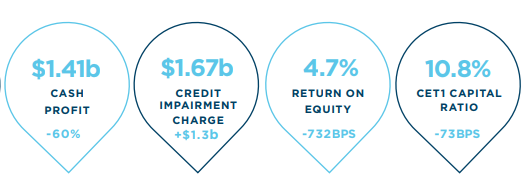

Australia and New Zealand Banking Group Limited (ASX: ANZ) declared its half-year results for 2020 on 30 April for the period closed 31 March this year. The bank reported a statutory profit of $1.5 billion down by 51% compared to last year driven by credit impairment charges of $1.6 billion, which included extra credit reserves of $1 billion for coronavirus related loan issues.

The bank has also been hit by $815 million loss to the valuation of investments in Asian associates who are affected by COVID-19 impact.

Below are some of the results for the bank-

Source: ANZ’s half-year report 2020, ASX

The bank has also deferred its interim dividend for 2020 with earnings per share down by 20 cents until there is clarity on the economic impact of COVID-19. The bank considered high uncertainty in the economic outlook and guidance from APRA for dividend suspension until a clear vision in assessing options.

As per Shayne Elliot, ANZ CEO, “The bank has assisted 1,80,000 customers with deferral on loan payments with a $16 billion additional funding to its long-term institutional-grade customers amid COVID-19. Given the prevailing tough conditions, ANZ gave a reasonable half-year result for 2020. COVID-19 has impacted ANZ’s performance, but it remains prepared to help its customers.”

The total provision charges for the half-year stood at $1.7 billion compared to $402 million in the previous half-year. The increase has been due to deterioration in economic forecasts due to COVID-19. The bank also plans on reductions in variable remuneration with a focus on maintaining productivity.

Overall, the bank remains well-positioned to manage the crisis and remains committed to its $8 billion cost ambition. On 30 April 2020, ANZ last traded at $16.90, up by 1.441%.

The outlook for 2020 still remains uncertain. However, as economic activities begin to recover, the banks are likely to recover as well. Investors may need to take a long-term view while investing in ASX bank shares.